Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jacqueline Ricci

October 26, 2023

WE THOUGHT IT WAS GOING TO BE DIFFICULT……..

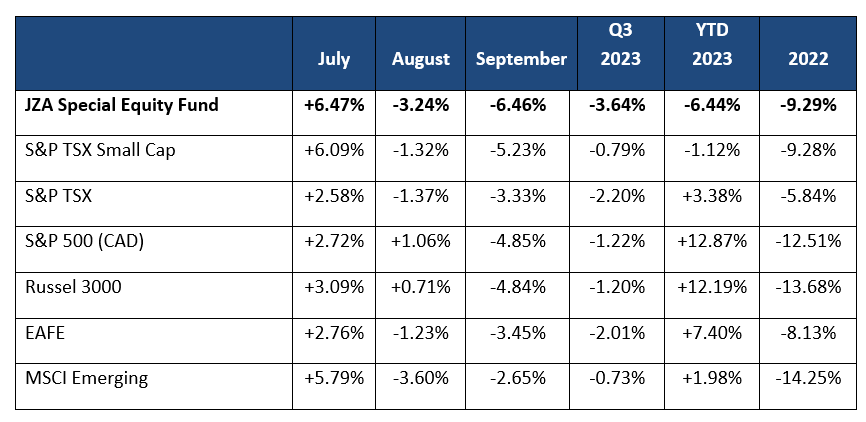

We spent some time in the last quarterly letter discussing the possibility of a weak fall for equities and unfortunately, we were correct. Returns in the quarter pushed Canadian indexes into negative territory and not surprisingly small caps bore the larger brunt of the decline. Below is a chart showing returns for global indexes as well as Canadian indexes.

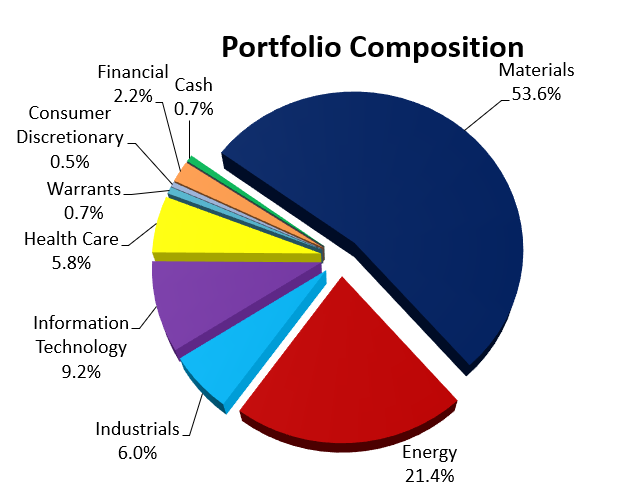

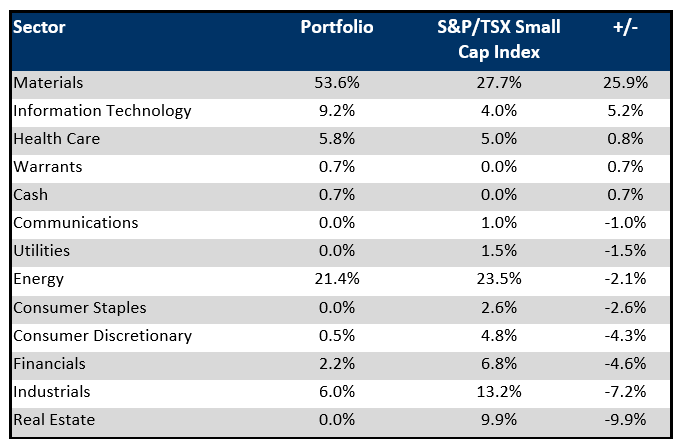

Below are some charts showing portfolio sector composition. Over the quarter, we increased the portfolio’s energy weight by increasing previous positions and adding new Canadian light-oil and gas condensate companies like Hammerhead and Logan Energy. The portfolio also added to its uranium and gold positions.

For the quarter the three positions which detracted the most from portfolio returns included NGex Minerals, I-80 Gold, and Los Andes Copper. Given that materials were one of the worst performing sectors in the quarter, it should come as no surprise that all three names are from that sector. Collectively these three names cost the portfolio -1.0%. None of these names had any relevant news in the quarter but were under pressure as investors reduced their weightings to this sector.

NGex is a high-quality Copper/Gold exploration company with projects in Argentina and Chile. It is currently advancing its newly discovered Lunahuasi deposit in the Sun Juan Province of Argentina in the emerging Vicuna District. This property is adjacent to Filo Mining’s discovery which BHP has taken an interest in. The drilling had been paused over the winter and is just starting up again. Its current program is fully funded, and we expect results to be forth coming in the coming months. We continue to hold this position.

I-80 Gold is a Nevada focused mining company with a goal of achieving mid-tier gold producer status with the development of four new open pit and underground mining operations that will ultimately be processed at the company’s central Lone Tree complex. We are also intrigued by the drilling to date on Ruby Hill which shows potential for significant base metal mineralization. We continue to hold our position in I-80 Gold.

Los Andes Copper Ltd. is focused on developing its 100% owned Vizcachitas copper-molybdenum porphyry project in Chile. The project is well advanced, with great surrounding infrastructure (transport, power, and desalinated water), low altitude and year-round access. We anticipate that Los Andes will be an acquisition target after they receive their permits and complete a bankable feasibility study. We continue to hold a position in Los Andes Copper.

The three positions which contributed most to returns in the current quarter include Athabasca Oil, Snowline Gold, and NexGen Energy. These three names contributed +1.7% to the portfolios return. When we look at the list of positive contributors this quarter, most of the names were from the energy sector.

Athabasca has a diversified asset base located in Alberta producing roughly 40,000 boe/d with a 90-year reserve life. It is made up of two divisions: light oil production and a thermal oil division. Their light oil is very high margin liquid rich production from the Montney and Duvernay shale plays. The thermal division complements by underpinning a low corporate decline with solid dependable cash flow. We put this name in the portfolio to take advantage of oil differentials. We continue to like this position and have added to it in the quarter. Snowline Gold is focused on a district-scale, greenfield gold discovery in the Yukon. The Rogue (Valley Discovery) and Einarson (Jupiter Discovery) projects have multiple primary target areas that host Carlin Style and epizonal orogenic gold mineralization. Although it is a somewhat remote area, the exploration success of Snowline and others in the region highlight the areas prospectivity. In the first quarter of 2023, Snowline’s discovery attracted B2Gold to purchase 9.9% of the company as a strategic investor. Snowline is one of our largest exploration holdings in the portfolio. We look forward to further drilling success with a fully funded drill program and continue to hold the position.

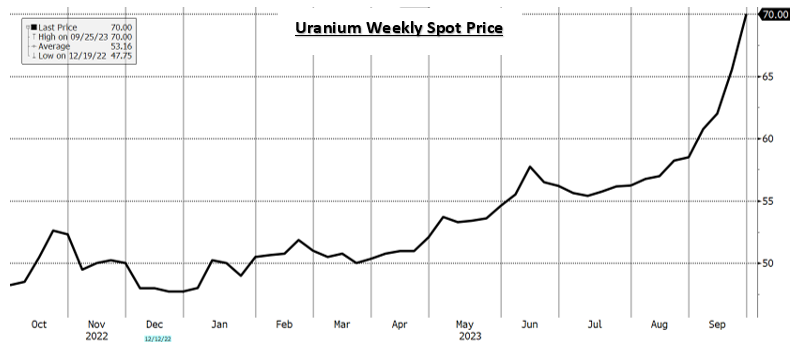

In the third quarter, uranium broke out of a longer-term base and closed the quarter at $70.00/lb, up roughly +45% from a year ago. This move in uranium prices helped propel uranium equities in the third quarter. NexGen has been in the portfolio for some time, and we added to the position in the quarter. NexGen is developing the Rook I Project located in the Athabasca Basin in Saskatchewan. The Rook I Project hosting the Arrow Deposit would be one of the largest low-cost producing uranium mines globally when in production.

WHERE TO FROM HERE…

Typically, September is one of the weakest months for equity returns and this September was no exception. As the Fed kept firm on their messaging that rates would remain “higher for longer”, investors began pricing this reality. For the third quarter, commodity markets and their participants continued to watch China with the hopes of a stronger recovery which did not materialize. Adding to the difficult environment was the war in the Ukraine and now the Israeli/Palestinian conflict.

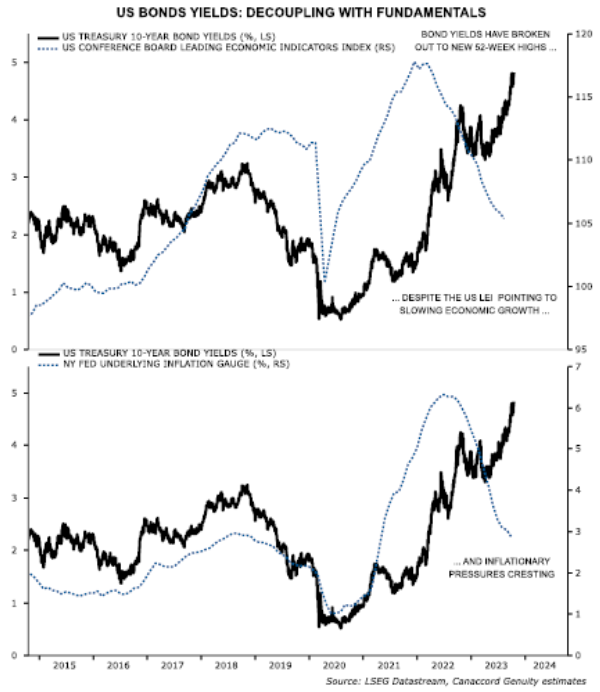

Looking to the future, the market is focusing on US bond yields and whether they are decoupling from fundamentals. The chart below shows that the 10-year bond yield has decoupled from US leading economic indicators and inflation expectations. The chart highlights that despite weaker economic and inflation signals, bond yields have been rising. We believe this is likely due to Japan and China selling US Treasuries to support their currencies. The increase in US bond yields have resulted in US dollar strength, which puts added pressure on commodity-based equities.

We anticipate that this headwind should abate in the next few months when the Fed signals the end of the tightening cycle because of economic weakness and/or job losses. With this backdrop in mind, Canadian equities appear to be undervalued versus world equities.

As we continue to believe we are moving toward the end of the rate tightening cycle we continue to adjust the portfolio by increasing positions in energy, precious metals, and base metals. The expectation is that energy and gold will be first movers, and copper will follow when the economy rebounds. Long-term we are still very bullish on critical minerals and given the extreme low inventory levels, we are maintaining the portfolio positions through the turbulence.

Although the start of the fourth quarter may be much of the same, we do expect markets to improve into the back end of the quarter and are quite bullish for 2024.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.