Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

July 1, 2024

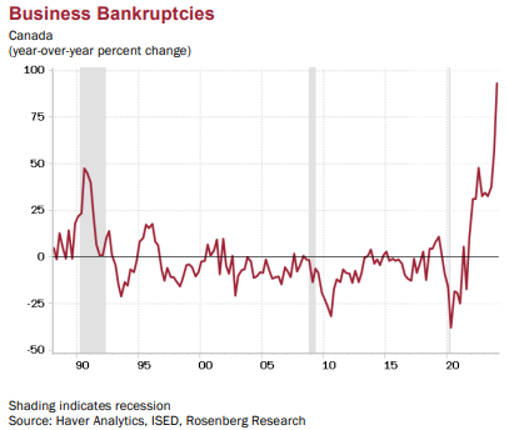

We are seeing many more indications of weakness in the economic data in addition to those mentioned above. In Canada the economic retreat has been even more stark as we didn’t have the excitement around the AI rollout and the same level of fiscal stimulus that supported both the financial market and the economy in the U.S. Our growth has been hampered by a much higher level of floating rate and shorter-term mortgages, which resulted in a more immediate and pronounced downturn in the housing market in Canada than we saw south of the border. Canada’s economy is projected to grow just 0.9% this year, well below the estimated 2.3% growth in the US, according to a Bloomberg survey of economists. But one statistic that really stands out in Canada is the level of business bankruptcies (shown below) which have surged almost 100% year-over-year, a rate far more than what we saw even during the financial crisis in 2008. The Bank of Canada is on the right path as far as we are concerned with their interest rate cut in June, despite a slight uptick in inflation over the past two months. We also still expect the U.S. Fed to cut rates twice this year, at their September and December meetings.

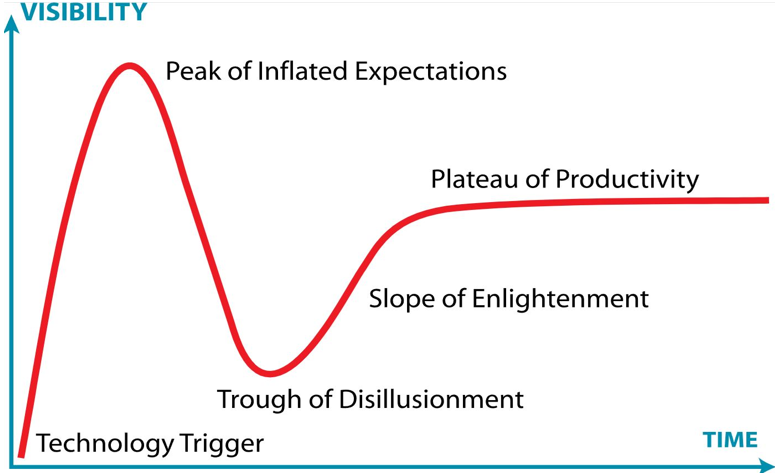

Those companies that can increase productivity most effectively should be expected to be the first beneficiaries from the AI rollout. Telecom companies can see a huge uptick in productivity as well as the online/mobile advertisers, suggesting that Amazon, Meta and Alphabet will continue to accrue early benefits from the rollout of AI. Cyber security companies will also garner a larger piece of the spending pie since companies need to be able to protect the massive flows of data needed to power the AI models. While Palo Alto Networks has been the clear leader in that field thus far, new competitors such as CrowdStrike are making major inroads and its stock is getting that recognition, trading at over 100 times expected forward earnings! Further down the value chain, away from the glow of Nvidia, lurk signs of discontent. Businesses have cut back on whizzy new AI tools out of concern for hallucinations, cost and data security. The proportion of global companies planning to increase spending on AI over the next 12 months has slipped to 63% from 93% a year earlier, according to a recent survey of 2,500 business leaders by software company Lucidworks Inc. Meanwhile, just 5% of companies in the U.S. are using AI, according to the Census Bureau. If you were to measure the malaise with the Gartner Hype Cycle, we believe that AI would be deep at the ‘Peak of Inflated Expectations’ and sooner rather than later headed into the “Trough of Disillusionment:”

But significant disappointment may be on the horizon, both in terms of what AI can do, and the returns it will generate for investors. Potentially quantifying the AI bubble is a calculation by Silicon Valley venture-capital firm Sequoia that the industry spent $50 billion on chips from Nvidia to train AI in 2023 but brought in only $3 billion in revenue. That difference is alarming, but what really matters to the long-term health of the industry is how much it costs to run AIs. To enable AI applications, companies have to make the switch from “general purpose computing to accelerated computing. AI can’t run on a traditional computer system, since it would be prohibitively expensive and far too energy intensive. To meet that demand, an estimated 100,000 data centers would need to be built in this ‘arms race’ to build out AI infrastructure. If real returns don’t accrue to those making the expenditures in a reasonable time frame, we could see a considerable downshift in the rate of spending. That would have an even more pronounced negative impact on the excessive stock valuations in this sector. Once again, this could end up being very reminiscent of the ‘post year 2000’ period. During that time the economy slowed down, and tech stocks plummeted, but the average stock did much better since valuations and expectations were already very low.

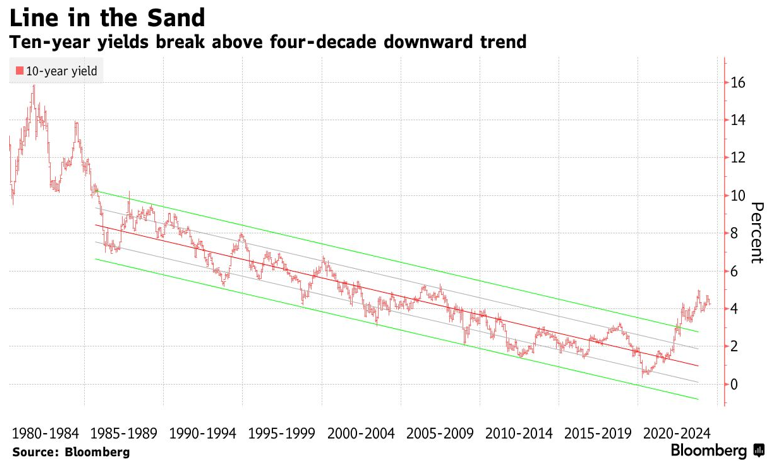

What about the trend in interest rates? Interest rates broke above a 40-year downtrend in the past year. But does this signify a return to the normal levels of the pre-financial crisis period, or will we return to the ultra-low levels of the past decade? We don’t see a return to the ‘zero rate’ world of the past decade, particularly since central bankers now realize that inflation has and will always remain a credible risk if too much money is pumped into the system. Moreover, real rates will return to something closer to prior ‘normal’ levels due to the massive borrowing needs of most governments and the need to finance those deficits in credit markets. Also limiting the central bank’s ability to cut and thus setting up a headwind for bonds is the growing view in markets that the economy’s so-called neutral rate — a theoretical level of borrowing costs that neither stimulates nor slows growth — is much higher than policymakers are currently projecting. With inflation around the world proving stickier than almost anyone predicted, expectations for sharp cuts in interest rates are fading fast. Federal Reserve Chair Jerome Powell confirmed as much on June 12, when he and his fellow policymakers signaled there would be just one reduction in U.S. benchmark rates in 2024.

Higher for longer keeps the dollar strong against other currencies, because the prospect of persistently lofty U.S. rates makes investment in U.S. securities more appealing on a relative-value basis, causing the greenback to appreciate further. With every tick higher in the dollar, things get tougher for developing economies — especially those that have dollar-denominated debt that becomes more expensive to pay back as their home currency weakens. Despite the Fed’s stance to stay on hold, some of its global peers are moving forward with rate cuts anyway. The Bank of Canada in June led the Group of Seven in lowering borrowing costs, with the European Central Bank following suit. If they get too far out of sync with the Fed, that risks driving down their currencies, raising import prices and undermining progress in getting inflation down. But not easing could risk lost growth. We believe that this ultimately gets resolved with both U.S. economic growth and the dollar weakening as stimulus winds down, consumer spending deteriorates further, and unemployment rises. That will open the door interest rate cuts later this year which could help to unwind the negative fallout we have seen on commodities and global growth outside of the U.S.

The World Gold Council released its annual central bank gold reserves survey, which shows 29% of central banks intend to increase their gold reserves in the next twelve months. Rebalancing to a more preferred strategic level of gold holdings, domestic production, and financial market concerns around crisis risks and higher inflation were highlighted as motivations behind gold purchasing plans. Moreover, Developing Economies central banks in particular expressed continuing concerns about the impact of geopolitics and potential financial instability on their reserve management decisions, with more central banks expressing less confidence in the U.S. dollar’s sustained supremacy. We expect emerging markets to dominate central bank purchases and investment demand, as the push to de-dollarise continues. Demand is being driven by record central bank buying, the largest buyer being China. They took a month off buying in May, according to the official numbers, and we saw a brief pullback in the price. But precious metals consultants we follow believe the actual buying is bigger than the official numbers, and that China is in a multi-year program of increasing its gold holdings – currently only 4.7% of its foreign reserve holdings – there is lots of room for this to keep growing as they look to diversify away from treasuries. As we head into a period of central bank easing of interest rates, which is historically good for gold, we remain positive on the outlook for gold and particularly the gold stocks, which continue to trade at multi-decade lows in terms of their valuations.

Putting it all together. Technology stocks still have all the momentum for now, accounting for all of the earnings growth in the past year and now benefitting from an expected round of interest rate cuts and continued buildout of the AI infrastructure. But we also have pointed out many slowdown risks as well as other technical and sentiment indicators that suggest a more defensive investment posture is appropriate. This may not be 1999, but there are increasing similarities. When that bull market finally ended, tech fell quickly and sharply but the rest of the market actually hung in surpisingly well and the economic damage was actually fairly minimal. We see those conditions again coming into place sometime in the next year. For now we are sticking with a ‘market weight’ in the tech sector and stocks overall, but are looking to increase positions in stocks in other sectors where the valuations are more attractive and the growth opportunities actually exist in an economy that experiences just a mild recession. Some of the key names we have added to in the past month include:

MDA Ltd (MDA-T) MDA is a market leader in geointelligence and earth observation (EO) data and satellites; robotics; and satellite systems. Demand for space-based industries and businesses is accelerating, driven by satellite cellular and internet service, missions to the Moon and Mars, new space stations and demand for space infrastructure and commercial services from defense and intelligence organizations. The award of lead contractor on the Telesat LEO project added over $1.5 billion to the backlog and secures double digit growth in cash flow over the next five years. The stock remains largely undiscoverd within its peer group and still trades at a discount to the group despite superior growth and much improved financial performance.

Capital Power (CPX-T) Capital Power is a North American independent power generation company based in Edmonton which develops, acquires, owns and operates power generation facilities using a variety of energy sources. We view CPX’s ability to build, optimize, and add value to dispatchable assets critical for system reliability as attractive given broad tailwinds for electricity demand. This underpinned by a growing need for reliable electricity in its core markets, where it has assembled a high-quality thermal asset base and complementary renewable power development. The stock has a reasonable valuation, a strong pipeline of growth projects and a fully-funded 6% dividend yield.

BCE Inc (BCE-T). BCE, along with the rest of the telecom sector and other high dividend yield sectors, has seriously lagged the overall market move since the beginning of the interest rate increase cycle in 2022. Telecom stocks had the additional negative due to the addition of a legitimate 4th player in the wireless sector and the worries about an impending price war and less subscriber growth due to more limited immigration growth. BCE has suffered the most due to its lower free cash flow generation as it continues to spend on network upgrades. But we see limited downside in valuation going forward and we expect the 9% dividend yield to add further support. Meanwhile, cash flows should continue to grow as traffic volumes expand on both higher streaming activity and the implementation of large language models for AI. Finally, the telecom industry should be a huge beneficiary of the cost reductions available from wide scale AI implementation as they communicate more efficiently with their customers.

Torex Gold Resources (TXG-T) Canada-based intermediate gold producing company, which is engaged in exploration, development, and operation of its Morelos Gold Property, located 180 kilometers southwest of Mexico City. The company has done an admirable job offsetting the decline and ultimate closure of the El Limon open pit and replacing it with the Media Luna deposit, which is an advanced stage development project located approximately seven kilometers from the ELG processing plant and related infrastructure. Moreover, once fully up and running, the Media Luna deposit will generate 30-40% of the value of production in copper, thereby also participating in the bullish outlook for the ‘red metal.’ The company has a stellar balance sheet with enough excess cash to fully develop the Media Luna facility and begin to generate free cash flow again.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.