Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

January 29, 2019

Growth worries are not confined to North America as things are looking rather bleak ‘across the pond’ as well. Europe appears closer to the edge of an earnings recession, with analysts at Deutsche Bank forecasting earnings growth of just over 1% in 2019 for European stocks. The most important economy to global growth is also having some slowdown issues. China’s economic expansion languished to its slowest pace in nearly three decades last year, as a bruising trade fight with the U.S. exacerbated weakness in the world’s second-largest economy. The 6.6% growth rate for 2018 is the slowest annual pace China has recorded since 1990. The economic downturn, which has been sharper than Beijing expected, deepened in the last months of 2018, with fourth quarter growth rising 6.4% from a year earlier. Adding to the gloom was the trade conflict with Washington. The uncertain outlook for Chinese exporters caused companies to delay investing and hiring and, in some cases, even to resort to layoffs. The official jobless rate ticked up to 4.9% last month. China’s economy has been decelerating partly due to President Xi Jinping’s initiative of the past three years to contain debt and fend off financial risks. That campaign has curbed borrowing by local governments and businesses and caused a sharp fall in capital spending, where fixed-asset investment grew 5.9% last year, a sharp drop from 7.2% in 2017.

The International Monetary Fund (IMF) lent further credence to this cautious outlook as it revised down its estimates for global growth, warning that the expansion seen in recent years is losing momentum. The Fund now projects a 3.5% growth rate worldwide for 2019 and 3.6% for 2020. These are below its last forecasts in October, making it the second downturn revision in three months. IMF’s Managing Director Christine Lagarde said: “After two years of solid expansion, the world economy is growing more slowly than expected and risks are rising. But even as the economy continues to move ahead … it is facing significantly higher risks.” In October, the IMF cut its global growth forecasts on the back of increased trade tariffs between China and the United States. It said the latest revision is due in part to carry over from last year, mentioning weakness for German auto manufacturers and soft domestic demand in Italy after recent sovereign and financial risks. But the IMF also high-lighted weakening sentiment in the global financial markets that’s now projected to be deeper than anticipated. According to the Fund, advanced economies have been on a declining path in terms of growth and this is taking place more rapidly than previously thought. There’s also been a simultaneous growth slowdown in emerging economies.

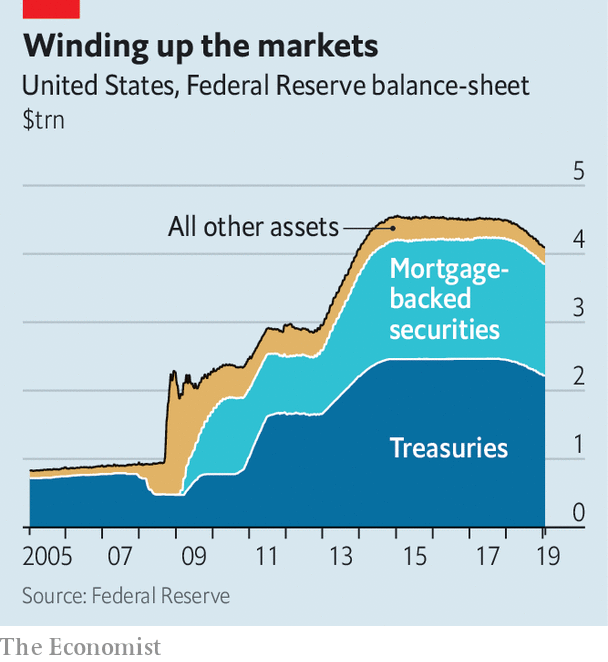

One more risk for financial markets is the 2017 plan by the U.S. Federal Reserve to gradually unwind its $4.5 trillion balance-sheet by not re-investing in or adding bonds. The Fed’s stock of assets had swelled during the previous decade as it engaged in “quantitative easing” (QE), seeking to ease the effects of the global financial crisis. After the economy recovered, it planned to shrink its balance-sheet again. The Fed’s expanding balance-sheet was first intended to provide banks in crisis with liquidity. The second was to signal to markets that monetary policy would remain loose for some considerable time. The third was to reduce bond yields, encouraging investors to buy riskier assets. All of this worked and helped to fuel a bull market in financial assets.

Investors now are justifiably worried that the operation is adding to pressure in markets which had already been upset by a series of interest rate hikes that began in 2015 and increased four times in 2018. The balance sheet reduction has come through allowing a set level of proceeds from the bonds to mature each month. In total, the bond reduction has been about $400 billion, so it’s still a long way from where it started back in 2009. While that does not imply that the Fed plans to shrink its balance-sheet to pre-crisis levels, it does remove a key ingredient for the easy financial conditions that existed for most of the past decade. Moreover, the U.S Fed is not the only one ‘pulling back the punch bowl.’ The end of Quantitative Easing in Europe, announced last December, is a new source of uncertainty. The biggest risk to financial markets in all of this is that the liquidity is being removed at a time corporate debt has risen to record levels, thus increasing the risk on another financial crisis!

Given our continued overall caution it should be no surprise that our investment outlook remains cautious, to say the least. While financial conditions have improved somewhat with the very recent less aggressive comments from the U.S. Fed, economic conditions have deteriorated further and this is the more important factor for markets going forward. The slowdown in the growth of output and trade world-wide has accelerated since the third quarter of last year. The stress is in the global producer space, in Asia especially. The Chinese economy is in trouble and the tariffs imposed by America are just one more problem. The economic slowdown in China is more significant than any period of weakness experienced since the 2008-2009 recession. In Europe and Japan there is virtual recession in manufacturing and the macro-economic data relating to activity in the Eurozone has become more negative than at any time since the crisis of 2011.

We continue to hold substantial cash balances in our managed accounts, and those are generating better returns than they have for the last five years. We have slight overweight positions in short-term bonds and preferred shares for their gross yields. When it comes to stocks, we see value in the beaten-up energy sector, particularly as geo-political issues in Venezuela, Iran and Nigeria continue to threaten supplies and we expect smaller production gains in both the U.S. and Russia. The risk, though, for all commodities remains a demand slowdown emanating from weakness in China, Japan and Europe. Technology stocks have been under selling pressure as they are ‘over-owned’ in most indices and portfolios and therefore remain an area of risk. It is still too early in this downturn to begin looking at financial stocks yet but their valuations, particularly in the U.S., have become attractive. We expect some weakening in the U.S. dollar this year due to slower economic growth and continued excess borrowing to fund ‘trillion dollar plus’ budget deficits. This should continue to lend some strength to the gold market and gold stocks as ‘currency alternatives.’ But, overall, we remain bearish about the outlook for stocks this year and expect we will return to the lows seen in late December and head lower from there.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.