Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

April 29, 2020

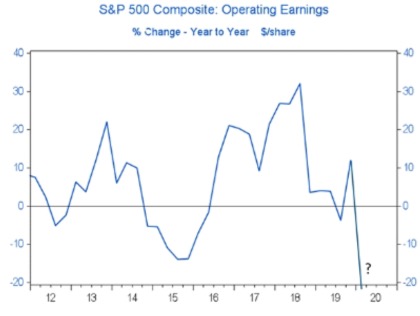

While we did increase stock exposure on the March sell-off, we are once again reducing many of those positions of the belief that stocks have just gotten too far ahead of the underlying fundamentals. The strength of this rally appears suspect in our view because the likely extent of the slowdown will be severe relative to historical experience, full impact to corporate earnings has yet to be seen and the path to recovery is completely unknown and will probably disappoint the more bullish views. Moreover, the ‘already highly levered economy is now dealing with contracting loan volumes and increasing loan loss provisions in the banking system. All of that suggests the economic data will be weaker than the consensus expects and remain that way for a longer time, which we believe will ultimately unwind much of the recent rally in stocks. When the S&P traded at these levels in both January 2018 and March 2019, forecast earnings over the next year were appreciably higher (meaning that stocks now look more expensive than in either of those past periods). Another less-talked about problem is that credit spreads have widened sharply in the past two months, meaning a higher cost of capital for most businesses and a riskier environment). Earnings for the first quarter have been bleak so far, down about 14% according to Refinitiv. But those include less than one month of the shutdowns of most businesses, the cancellation of sporting and cultural events, the mass reduction in travel and the curtailment of retail spending on dining and shopping. Second quarter results are expected to be far worse, most likely falling by over 30% year-over year!

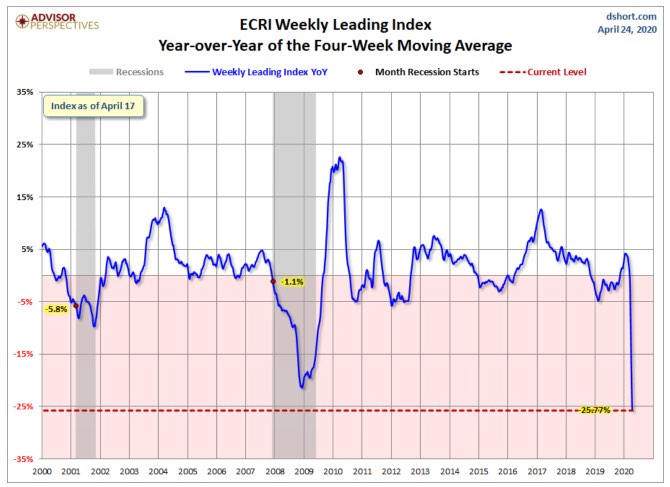

All of the world’s major economies contracted sharply last month, with record job losses in Canada and the U.S. Economists have slashed back their economic forecasts in the midst of an historic economic contraction. The western world economy has largely shut down, paralyzed by measures to contain the coronavirus pandemic, plunging oil prices and plummeting confidence. Given how quickly the downturn has been, many expect the recession to be short and severe, but there is also becoming less expectation of a ‘V-shaped’ recovery. Any re-opening of the economy promises to be gradual and limited. Nobody is expected to be going into big crowds, events or airports any time soon and the protocols for most businesses and retail operations will change dramatically, not unlike the change we saw to air travel ‘post 9/11. The Canadian economy is likely in its deepest recession on record and will only recover modestly over the coming year as it takes a direct hit from the coronavirus outbreak and a collapse in oil prices, a Reuters poll of economists showed.

Oil markets seem to be giving a truer picture of the rough roads ahead. The collapse in oil prices seems to be more reflective of what is going on in the real economy than the stock market. Despite coming to a production cut agreement that is beyond anything investors could have imagined just a few months ago, oil prices continued their meltdown, falling to levels not seen since the lows of the 1990s. The OPEC-plus group agreed to cut back production in stages by almost 10 million barrels per day (bpd), starting in May. But that came nowhere close to offsetting the fall in demand, which looks to be in excess of 20 million bpd, as lower industrial output, almost no air travel and less driving combined to lessen the need for refined products. The negative price on the May crude contract showed how desperate the situation was in the near term, as this anomaly suggested that investors in the contract would rather pay someone to take their oil rather than trying to find space in storage tanks that are almost full or tankers which are charging elevated rates. The ultimate supply response will come from the fact that many producers will end up going bankrupt and all will cut back their development spending dramatically. This suggests that getting any substantial recovery in oil prices will take a long time. In the meantime we see exceptional risk with almost all of the producers and oil field service companies but still have a level of comfort owning the pipeline stocks, which have relatively safe dividends and are mostly volume, rather than price, sensitive and have longer term supply contracts.

Bye-bye to buybacks! Corporate behaviour is also undergoing a significant change in this new world. Companies now seem to understand in this crisis that it is more important to have capital and liquidity to survive the downturn than it is to be doing any ‘financial engineering to keep their stock prices elevated. Companies such as General Electric, which spent over $25 billion buying stock from 2015-18 which is now valued at less than $10 billion, would rather have that capital available now to run their business. To that end, most have announced either reduced buyback plans or a hiatus altogether while much of the bailout money made available by the new government loan and grant programs, dictate that recipients cannot be involved in stock buybacks if want to apply for any of those funds. Buybacks have annualized US$600-800 billion over past six years, the biggest single source of buying in the stock market. I think we can safely say that era is over for now. While many companies, especially banks, want to keep their dividends intact, share buybacks are a different story. They are viewed in general to be a benefit to senior management and large shareholders, two groups that are nowhere near the top of the list of those needing help in this environment.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.