Investment Strategies for the Next Decade

As we enter a new decade, the time is right for many investors to step back and look at their overall financial goals as well as the structure of their investments. We also believe that this should be done in conjunction with some informed view about the expected investment environment over that period. . Using the history of the past decade, we believe the key trends that will influence the investment environment in the coming years are as follows:

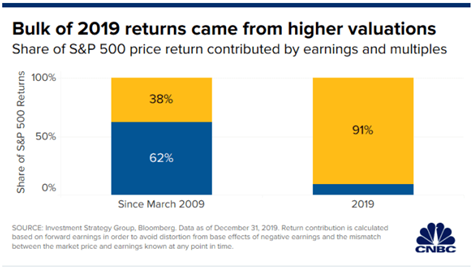

The past decade was characterized by ongoing bull markets in both stocks and bonds that were fueled by the record low interest rates put in place by global central banks in the wake of the Financial Crisis. But it was also witness to the slowest economic recovery on record as those low interest rates did more to inflate financial assets than to promote economic growth. Those low interest rates are expected to stay in place for the next decade as global economic growth will remain low, inflation will remain restrained and profit growth will stay muted. However, we don’t expect to see the same kind of expansion of stock valuations that we have seen over the past decade, suggesting that stocks will only be able to rise at this expected ‘muted’ rate of profit growth.

- The past decade was unusual in that growth remained low but there was no global recession, thus giving rise to the longest expansion in over 50 years. We don’t see a repeat of that in the coming decade and expect that we will see at least one major recession or two smaller, back-to-back recessions similar to what we saw in the early 1980’s; consequently, we would experience the first full-blown bear market in stocks since the Financial Crisis. That scenario would continue to support positive returns from fixed income investments, particularly government bonds, where we expect to maintain overweight positions in mid-term maturities.

- In an environment of slower growth, low interest rates and stable stock valuations the strongest returns will come from those ‘disruptor’ companies which can maintain superior growth rates. Some of the most successful long-term growth stocks have been multi-national corporations domiciled in the U.S. market. While the great pharmaceutical, communications and media companies such as J&J and Disney have been the steadiest winners for decades, a new breed of technology companies such as Microsoft, Facebook, Alphabet and Amazon are laying the foundation for growth leadership going forward. These are the types of growth stocks that we expect to maintain leadership in global stock markets.

- Global debt has sky-rocketed in the past decade to a record level of over US$250 trillion! Servicing this debt will necessitate continued low interest rates but any remote ability to reduce this debt burden would require a global depreciation of the paper currencies of the most indebted nations, particularly the U.S. and China. By default, gold would have to rise in such an environment. With gold stocks at multi-decade low valuations, we advocate a 4-5% weighting in gold equities as a hedge in any balanced portfolio.

- Cash in a savings or money market account does not earn more in interest than the current rate of inflation such that investors would continue to lose purchasing power over time by holding substantial cash positions. We advocate other asset classes that can generate positive real returns with limited downside risk.

1 2