Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

April 1, 2026

OK, SOMEBODY knew SOMETHING! On the morning of March 23rd with S&P 500 futures setting up for another weak opening, stock and oil futures flashed an unusual burst of activity minutes before a market-moving social media post from President Trump. At around 6:50 a.m. in New York, S&P 500 e-Mini futures trading on the CME recorded a sharp and isolated jump in volume, breaking from an otherwise subdued premarket backdrop. With thin liquidity typical of early trading hours, the sudden burst stood out as one of the largest volume moments of the session up to that point. A similar pattern was observed in oil markets. West Texas Intermediate May futures saw a noticeable pickup in trading activity around the same time. But the oil activity was from a short seller, meaning someone who was expecting oil prices to fall. Roughly 15 minutes later, Trump said on Truth Social that the U.S. and Iran had held talks and that he was halting planned strikes on Iranian power plants and energy infrastructure. That announcement prompted an instant rally in risk assets, with S&P500 futures soaring more than 2.5% before the opening bell. At the same time, West Texas Oil futures dropped nearly 6% following the announcement. The U.S. Securities and Exchange Commission and the CME Group declined to comment!

This was not the first time we’ve seen profitable trading in front of major announcements from Trump. The Reuters review found four prominent instances where trades stood out for their timeliness. In April 2025, options traders made millions in late-breaking bets in the minutes before Trump announced a pause on his blanket “Liberation Day” tariffs, sparking a 9.5% jump in the S&P500 Index. In January this year, an unknown Polymarket trader took in more than US$400,000 after betting on the ouster of Venezuelan President Nicolas Maduro that month. The anonymous account was created the previous month and placed more than US$30,000 in bets that would pay off if the U.S. invaded Venezuela by January 31. Bets placed on prediction markets like Polymarket and Kalshi ahead of the Feb. 28 killing of Iranian Supreme Leader Ayatollah Ali Khamenei sparked fresh insider trading and ethics concerns. Analytics firm Bubblemaps identified six accounts that made a combined US$1.2-million profit from Polymarket bets that were funded in the hours immediately before the U.S.-Israeli attacks that killed Khamenei. Last week, unidentified traders made a US$500-million oil bet minutes before Trump sent crude plunging by announcing he was delaying an assault on Iranian energy assets. The bets were placed on the New York Mercantile Exchange, which is owned by CME Group. Some of the experts said the sheer size and binary nature of some of the bets raised the possibility that people may have had advance knowledge. Monday’s US$500-million oil market trade, for example, indicates extreme conviction as well as deep pockets, some of the experts said. But no investigations of any of these trades has been announced by the SEC or any other regulatory body. The rest of us will just have to invest the ‘old fashioned way.’

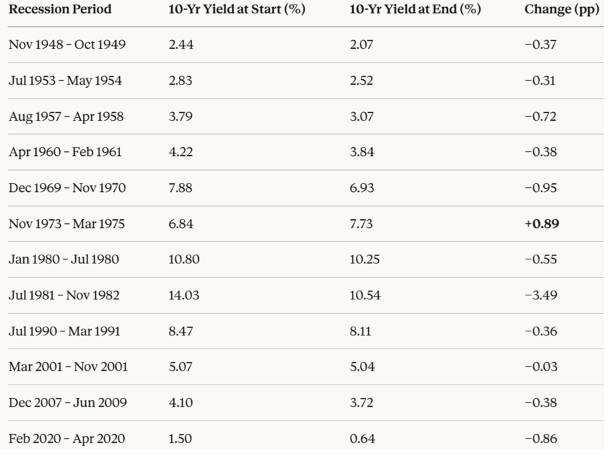

The economic risks from higher oil prices have major historical precedents. All but one of the post-1945 U.S. recessions has been preceded by rising crude oil prices caused by supply disruptions. It has led analysts to implicate oil price shocks as an important “force multiplier” in U.S. slowdowns, even if not the main factor. While recessions have often been precipitated by sharp increases in oil prices, bond prices generally fall during recessions. So far this year, though, oil prices have spiked but bond yields have also moved higher. As shown in the table below, that only happened one other time during every recession since the Second World War. That runs counter to what usually happens in U.S. recessions, during which bond yields decline (despite the adverse impact that recessions have on government tax revenue) and probably help spur recoveries in yield sensitive sectors. The reason it “might be different this time” is that the War could expand the deficit at a time when the US debt load is already high, spurring concerns of eventual monetization and inflation.

Is Bitcoin worth looking at now that it has dropped over 50% in the past six months? Bitcoin has been touted as a store of value, as a financial advancement with blockchain technology, and as a currency. Bullish investors have seen it as both ‘Gold 2.0’ and ‘Visa 2.0.’ But bitcoin hasn’t worked as a currency, as its value changes too rapidly and you can’t buy most regular items with it. Also, the energy required to process transactions is too expensive. But Bitcoin also hasn’t acted well as a store of value. When investors got spooked earlier this year, the price of gold rose but Bitcoin’s price cratered, so it’s not really doing either job very well. Bitcoin has mainly succeeded in terms of brand recognition. “It has become the Kleenex of crypto.” Recent legislation in the U.S. to add a regulatory framework to cryptocurrencies and stablecoins could accelerate the adoption of Bitcoin and boost its price but the reality for now seems to be that the biggest driver in Bitcoin buying is the expectation that the price will go higher. That is basically the definition of a speculative asset and not, in our view, a good reason to make it part of your portfolio, even at these more depressed levels.

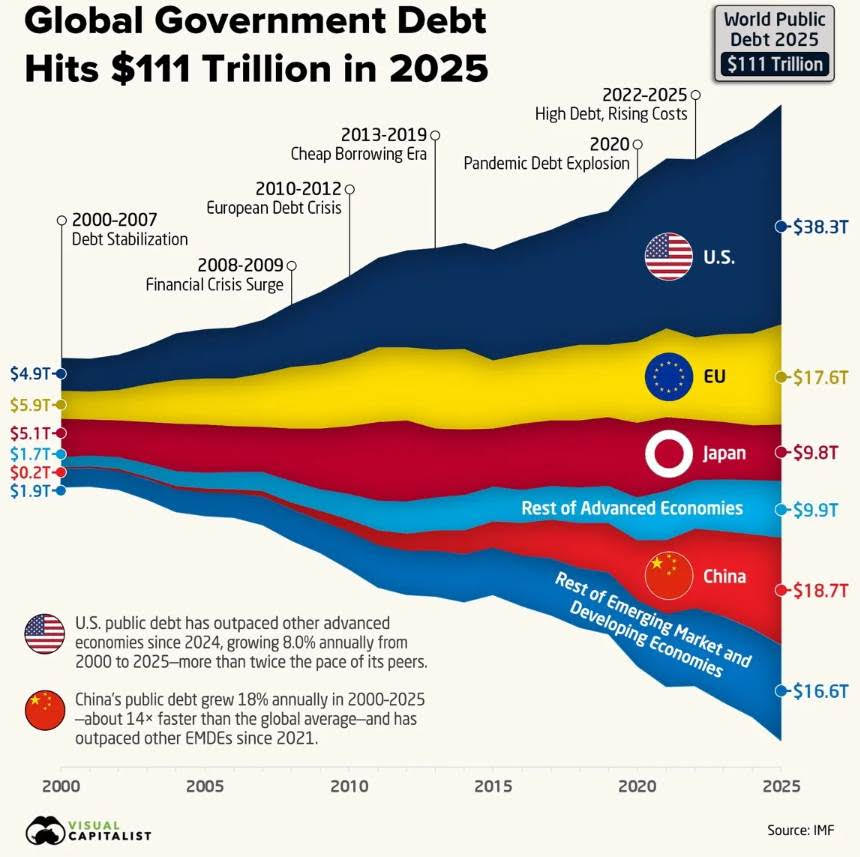

Gold has not been ‘golden’ in the recent turbulence. Gold had been on a record run for the past two years as central banks were big buyers to diversify their reserves away from the U.S. dollar and this strength also drew in public investors at a much higher level in the past year. That run ran into some serious resistance when the U.S. and Israel started bombing Iran and central bankers moved quickly to increase their liquid assets. Turkey’s central bank sold and swapped about 60 tons of gold, worth more than $8 billion, in two weeks after the start of the war in Iran, adding to downward pressure on bullion prices. The sales mark a reversal for Turkey, which has been one of the world’s most aggressive gold buyers over the past decade as it sought to reduce exposure to US dollar-denominated assets. Gold prices have fallen by about 15% this month, with investors taking profits following a strong rally since last year. The economic shock from the war in Iran will likely dent demand for bullion from some central banks while forcing others to sell from gold reserves to meet dollar-denominated obligations. However, this is only expected to be a ‘short-term, war related’ move. In the end, we expect central banks to continue to diversify their reserves, which have been largely held in U.S. dollars for decades. The simple reason is that the world public debt levels continue to soar and the U.S. has become the largest ‘net debtor.’ Much like Britain was the dominant global economic power and the Pound was the global reserve currency a century ago, the slow loss of economic power eroded that advantage over time while debt continued to climb. The ultimate fall of the British Pound as the global reserve currency and its replacement by the U.S. dollar was inevitable as the U.S. was in the process of becoming the leading global economic power. The mantle of global economic strength now appears to be in the process of being handed over to China, but their currency is a long way from being accepted as a global reserve currency. Ditto for the Euro and the Yen, which have better global acceptance and liquidity, but their economies do not have the global clout or growth to let them replace the U.S. In the meantime, holding some gold still seems like a very good idea!

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.