Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

July 2, 2022

The bear market in U.S. stocks officially arrived with the S&P500 hitting the 20% decline threshold from its January high at the close of trading on June 13, and then falling further to its current price trough three days later. It ended up ass the worst first half in the S&P500 in over 50 years (since 1970). On this side of the border, the TSX fell ‘only’ 11% in the first half but, as most investors are aware, that was only because the Energy sector held up the average with its 40% gain. Outside of that, everything else in the index was down, with the consumer, health care, technology and base metals sectors leading the declines. Not to be outdone, bonds suffered their worst first half on record. In Canada, the FTSE Bond Index fell 12.2%, highlighted by a whopping 22% loss for the Long-term Index. Despite the already severe drawdown in markets, sentiment appears to be overwhelmingly negative, with many investors now predicting an imminent recession. Speculative asset classes suffered even more, with Bitcoin losing 60% this year as the industry has seen a wave of liquidity concerns, with hedge fund Three Arrows Capital going into liquidation and lending firm Celsius pausing withdrawals for customers. The quarter also saw the collapse of algorithmic stablecoin terraUSD which sent shockwaves through the industry.

The first stage of the 2022 sell-off in stocks (which took the ‘tech heavy’ Nasdaq over 30%) was almost entirely due to the re-valuations of ‘high multiple growth stocks’ from the rise in interest rates. Future interest rate expectations have risen sharply on the surge in inflation, which is proving to be far more broad-based and problematic than the consensus and Federal Reserve members previously thought, due to continued supply chain disruptions, Chinese shutdowns and ongoing geopolitical conflicts. The market’s recovery in 2020 had everything to do with the concept that central banks will always be there to save the day. Now, not only do central banks have no immediate desire to step in, they’re likely to continue tightening into this weakness until they see a clear breakdown in the monthly inflation numbers. Federal reserve Chair Jerome Powell was very clear this past week, saying that the “Fed will not let the economy slip into a high-inflation regime even if this means raising interest rates to levels that put growth at risk”. The Fed simply stated the obvious: that a recession may result from its fight to curb inflation. The net result was stocks incurring further losses to close the quarter.

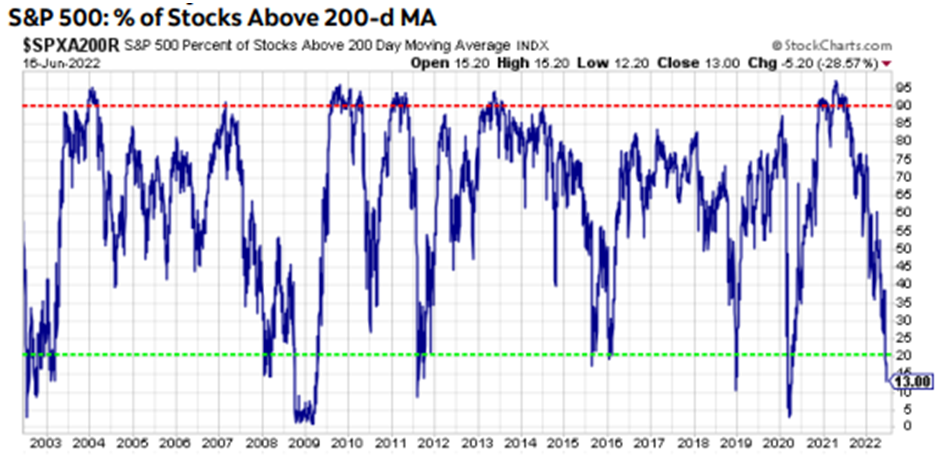

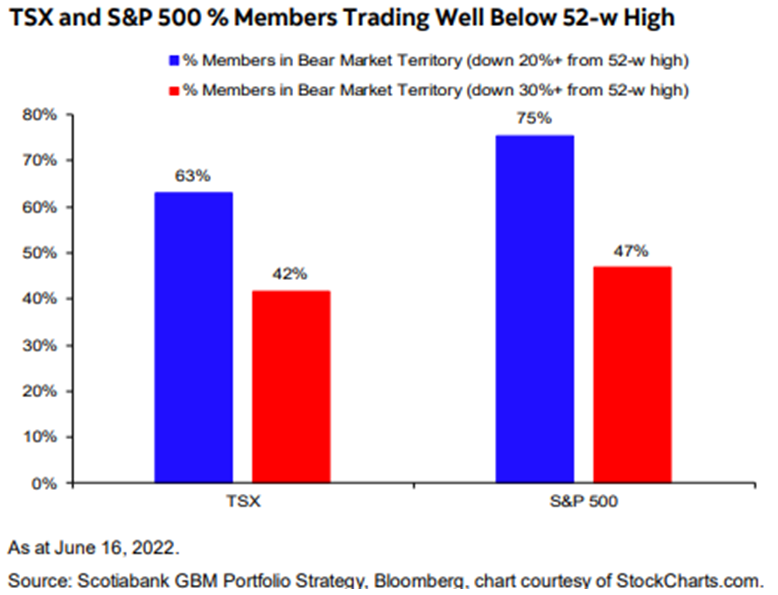

The brutal selloff has spared very few stocks. As shown in the charts below, the percentage of S&P500 stocks trading above their 200-day moving average line has dropped massively and is down to 13%, a level usually seen near bear market lows. The breadth of the losses has also been very wide, both in Canada and the U.S. The lower panel below assesses the extent of the damage, with most members in the TSX (63%) and S&P500 (75%) in bear market territory, i.e. down more than 20% from their 52-week highs, with a large swath now sporting declines greater than 30% from their highs (42% for the TSX and 47% for the S&P 500). Sentiment about both the economy and stocks has deteriorated dramatically in the past six months, as investors seem to now expect a full reversal of many of the factors that lead to the strong markets of the past decade. We would point out, though, that sentiment can shift far more quickly than actual economic trends. While the short term outlook remains shaky, we hesitate to ‘throw out’ all the benefits of globablization and technology-driven productivity gains that have been the hallmark of the growth in corporate earnings.

Whether or not this turns out to be the end of the selling and we see some recovery in the back half of the year depends on whether we see the ‘second shoe’ drop, with earnings missing expectations and/or companies reducing forward guidance. Despite the rise in interest rates, the bullish case for stocks was that earnings were still growing despite rising inflationary pressures. That narrative changed as Microsoft, Apple, Snap and Amazon pointed to currency pressures and the shutdown in China as impacting demand and costs. Then leading retailers such as Walmart, Bed, Bath & Beyond, RH and Target (twice in 3 weeks!) reduced their outlooks due to the negative impact of higher wages, ongoing supply chain problems and rapid changes in consumer preferences, leading to some inventory mismanagement and price markdowns. These ‘earnings warnings’ are the next big risk for the stock market. The upcoming second quarter reports will be absolutely critical to judge how companies are dealing with these conditions. Much attention will be paid to the results from the technology sector. Will we find that many customers ‘double-ordered’ during the chip shortages and are now reducing excess inventories as demand from cell phone makers, cloud service providers and data centres gets reduced. The commentary from memory chip company, Micron, on their June 30th earnings release created more worries for the sectors since Micron sells memory products sold into client, cloud server, enterprise, graphics, networking, smartphone and other mobile-device markets.

The risk to earnings is quite acute as the economic data has aleady started to roll over. We may find out later that the U.S. technically fell into recession during the first quarter. While massive inventory build-ups may have bloated real GDP in the second quarter, this will unwind and hurt growth for the rest of the year. Alarmingly, consumer sentiment, as measured by the University of Michigan, is lower today than levels reached during the Global Financial Crisis in 2008-09 and the two recessions in 1980-82 when Fed Chairman Volcker was choking 15%+ inflation with 20% interest rates. The combination of increased interest rates in a levered financial system just as fiscal authorities were in the process of removing or not renewing the stimulus programs put in place during the pandemic has been a short-term shock to the consumer. One key indicator that reinforces the view that growth is buckling is the surprising sag in a wide variety of commodity prices, particularly copper. The red metal dropped almost 20% in June and is now at its lowest ebb since early 2021, after hitting a record high in the immediate aftermath of the Ukraine invasion. In fact, many broad measures of ex-energy commodities—even agriculture—are now lower than pre-invasion levels amid global growth concerns. We take some solace in the view that the slowdown won’t be as painful as the last global one because there aren’t the same imbalances in the U.S. economy, the banks are not in as precarious a financial situation, and there is not the same oversupply of houses and cars. At the same time, consumer finances are in better shape than they were in 2008 and there is still a strong backlog of demand for many goods, such as autos, which were in short supply during the pandemic. Add the resurgence in spending on travel and other services and this economic downturn could easily turn out to be quite ‘short and shallow.’

In terms of our outlook for stocks in the back half of 2022, we remain constructive despite the interest rate and economic risks we’ve described. We have seen the multiple on the S&P500 fall from over 21 times to around 16 at the recent low, close to the long-run average. The chart below shows the Price-Earnings multiple over the past twenty years and how sharply stock valuations have corrected from those peak levels.

We recognize that in any bear market, stocks rarely stop falling at ‘fair value’ and generally bottom at much lower levels, we believe that central bankers may not need to be as ‘hawkish’ as they currently appear since we don’t see inflation being endemic like it was in the 1970s. Wage pressures have not become built-in to expectations to the same degree as they were five decades ago. Moreover, increasing capacity and slowing economic activity will reduce goods shortages and, most importantly, ongoing technological innovation will continue to be a source of disinflation and increased productivity, as it had been for most of the past three decades. While the key market risk is that this strong medicine for inflation could set off a recession, the economic and earnings data has yet to fully reflect that outcome. For now, jobs are abundant, wages are rising, and household and corporate balance sheets look strong.

The basis for being a bit more optimistic on the outlook for stocks is that inflation will recede more quickly than investors are expecting, meaning that central banks will not need to be as hawkish as they are now. Earnings warnings from retailers Walmart and Target show that excess inventories will be sold off at discounted levels. Inventories and stock prices are leading indicators for employment and wages, so fears of cost-push inflation a la 1970’s should disappear during the next six months. The implication for investors is that interest rates will peak sooner than expected and they can start to look once again at many of the beaten-up quality growth sectors, whose earnings are generally more resistant to economic downturns and yet whose valuations have fallen the most over the past year. In fact, bonds have been rallying on the stock sell-offs during June, a clear difference from the first five months of the year when both markets fell in tandem. The ‘read’ from this is that the bond market and stock market both see weaker economic data ahead, rather than the view that all that could see was higher inflation earlier this year.

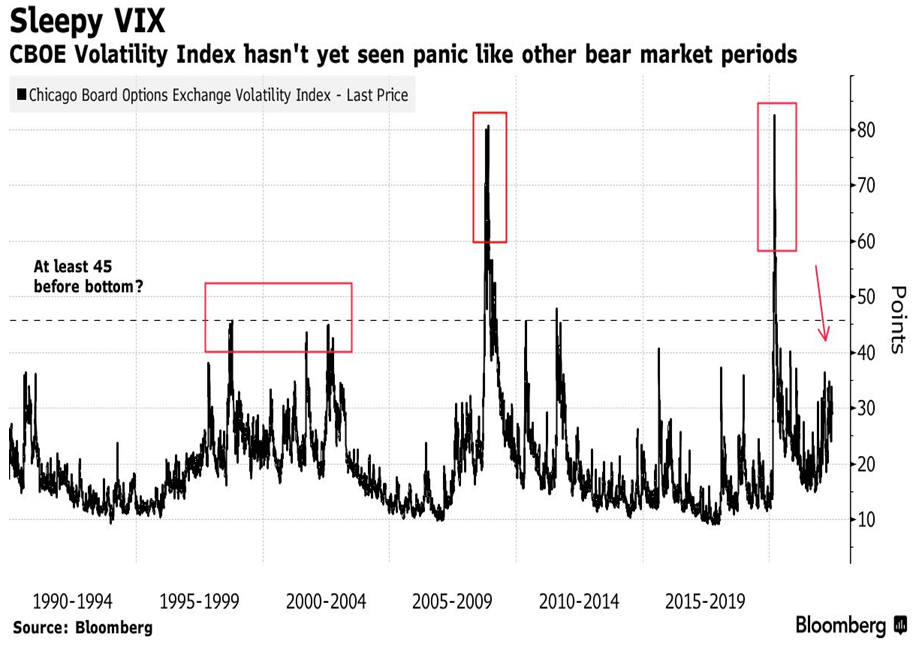

Despite the dismal results for stocks over the first half of the year, we have not yet seen the same surge in the ‘Volatilty Risk’ as we have seen in prior market sell-offs. The Volatility Index, or VIX, is used as a measure of investor fear. Options strategists and bankers cite a simple reason why this measure has not spiked higher: The S&P 500 has been staging a long, orderly descent from the record level hit at the start of the year as the Federal Reserve pulls back its flood of pandemic-era stimulus. That differs from ‘shock-driven crashes’ like the ones caused by Covid-19 in March 2020 or the collapse of Lehman Brothers Holdings in September 2008, both of which sent the VIX surging as investors sought to hedge the risk of wild market swings. The worry is that we have not yet seen the flush of ‘panic selling’ that would send the VIX soaring and has usually been the harbinger of the end of the downturn. In that regard we might see some further selling into the third quarter until it becomes clearer that either inflation is starting to recede and/or the damage to earnings from the economic slowdown will not be as severe as feared.

Trying to assess the potential depth of any downturn and the ultmate impact on stocks, Swiss bank UBS noted that shallow recessions are associated with central banks hiking rates, typically in response to high inflation. It noted that stock sell-offs typically begin eight months prior to the start of a recession, reaching a bottom within four months of the start of the subsequent recovery. On a sector basis, share price returns of financials, industrials, and consumer discretionary stocks are notable for being the “most sensitive” to the depth of recession — whose prospects are most improved if one can be confident that a deep recession would be avoided. So far this downturn in stocks is worse than the average experience, assuming that the economy moves only into a ‘short and shallow recession.’ Our view is that the market peaked in November 2021 and the economy moved into a shallow recession sometime in the first quarter. We expect the recession to continue in the second half of the year and begin to recovery by the fourth quarter. In that scenario, the stock market should bottom sometime in the current quarter, which is why we have been adding to stocks despite the shorter-term earnings and interest rates risks. I should always add “for what it’s worth” since trying to ‘time’ that move to such a degree is clearly subject to timing risk.

Another old adage say that ‘those who fail to learn from history are doomed to repeat it.’ So when looking at the past two years in particular, we need to remember that financial market ‘bubbles’ always eventually burst and rational investing returns in long term. Whether we go back to the Dutch Tulip mania in the 1600s, the South Seas bubble in the 1700s, the real estate bubble in the 2000s, the ‘Nifty Fifty’ or ‘Dot Com’ stock market bubbles in the U.S. or the ‘pot stocks’ here in Canada, the reality is that these bubbles always do come to an end. The ensuing selloffs then takes back all the gains and then some since the bulk of the money flows into these investments late in the cycle. The Ark Innovation Fund, the ‘poster child’ for pandemic investing, went from the March 2020 low of $40 to $160 and then a ‘round trip’ all the way back down to and below that $40. However, the losses would be even greater since most investors got into the Funds later on and the average dollar in the Fund has a cost base of over $100, meaning that most investors in the Fund have lost over 60% on their investment.

But when bubbles are in place they seem to ignore proven fundamental models and make everyone wonder ‘is it different this time?’ We have once again come through such an episode and I was questioning everything I learned in university in the 1970s about monetary theory. The old adage that “inflation is always and everywhere a monetary phenomenon” espoused by Milton Friedman seemed to go out the window as global central banks created unprecedented levels of money as they drove interest rates to zero over the past decade (or even the non-sensical idea of negative interest rates) as they tried in vain to raise inflation to a 2% target. Clearly the conclusion could only be that the old monetary model did not work anymore!

That has all changed in the past nine months as inflation soared to 30-year highs and the speculative bubble in all of those assets that were inflated by ‘free money’ policies (SPACs, high growth/profitless stocks, crypto currencies, NFTs) have collapsed. The lesson for all investors should be to never forget that fundamentals do matter in the end and the most important focus should be on looking for companies with reasonable valuations, strong balance sheets, growth and cash flow.

Our short-term strategy in this downturn has been to look to for positions in depressed valuation sectors or those reflecting excessive pessimism, which should have limited further downside yet some strong recovery potential. We are seeing such trading opportunities energy, where the stocks dropped over 20% in June despite trading at record low valuations. But the forces keeping energy prices high are enduring, whether there is a recession or not. There is a structural supply shortage in oil which was been worsened by the Ukraine conflict and loss of Russian supplies. Slower economic gorwth and the onoing China shutdow have hurt demand to some degree, but not enough to send oil below US$100. Key names in the sector that we have been adding include Crescent Point, Whitecap Resources, Suncor and Baytex as well as natural gas producer Arc Resources. We see similar oversold opportunities in the consumer sector, which has been the main clearing house for investor hopes and fears about inflation, interest rates, and the economy. Consumer discretionary stocks, specifically, have the worst returns of any S&P500 sector, with year-to-date losses sitting at 30% as sectors such as autos and travel have sold off dramatically and already reflect a recession scenario. We have added to positions in General Motors, Fedex, Magna, BRP (skidoo/seadoos) and Air Canada on this weakness.

For the longer-term we are looking back at the growth sectors such as semi-conductors, communications services and technology that would benefit from a peak in interest rates. We believe that we will ultimately return to the slower growth mode of the past ten years, which will limit inflationary pressures and keep interest rates low, all of which benefit these higher growth sectors. The larger risks in the short term are more related to the economic risks associated with the rise in interest rates, including the earnings risk to many economically-sensitive sectors such as industrials, transports, retailers and basic materials. We have also not gone back to the Financial sector to a large degree yet despite some attractive dividend yields and moderate valuations. We are concerned that some of the earnings ‘tailwinds’ of the past two years (booming capital markets, strong economic growth, loan loss reversals) have turned to ‘headwinds’ in the short term. In Canada, we are concerned that the major (US$15 billion+ each) U.S. acquisitions done by TD and Bank of Montreal may impair capital ratios in the short term.

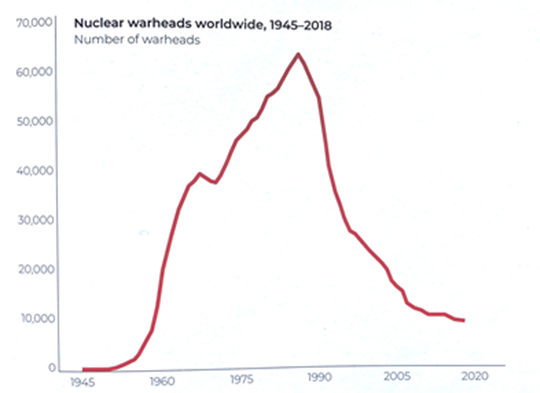

Finally, Something to be cheerful about! No, this is not a chart of equity markets following unprecedented central bank liquidity injections following the Covid pandemic, but rather the number of nuclear warheads held globally With an increasing amount of news to get depressed about in the current environment, it’s worth remembering charts like these that show on the whole, the world is getting better and despite the conflict in Ukraine, things like nuclear war are by definition, a much lower risk than they have been in the past (an 86% reduction from the highs)

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.