Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

November 30, 2022

Stocks continued to shake off the worries from sharply rising interest rates and some shaky earnings projections and focused instead on some indications from a few central bankers that we could be closer to the end of this aggressive rate hiking cycle. This helped stocks generate a great start to the fourth quarter and their traditional year end strength, which was much needed following the brutal stock sell-off to end the third quarter. Canadian stocks have risen over 4% so far this month and are ahead over 10% in the 4th quarter, reducing the 2022 loss to under 2% on continued strength in the energy and utility sectors and a recovery in technology stocks. Similar story south of the border where the Dow Utilities have jumped over 5% and the Nasdaq has surged over 6% so far in November. The broader S&P500 however, has risen under 3% this month due to weakness in some retail and financial stocks and the ‘small cap’ Russell2000 is actually down almost 1% in November, suggesting a fairly ‘narrow breadth’ to the advance. Clearly the implication of these stock moves is that investors feel comfortable moving some money back into stocks on some interest rate optimism, but are limiting their exposure to the safe, defensive sectors and eschewing more cyclical sectors due to worries about the economy.

Bond markets also cheered both the prospect of a cessation of rate increases as well as sharply lower economic growth next year. Ten-year bond yields in the U.S. have retreated from the 4.2% level seen at the beginning of the month to the current rate of about 3.7%. In Canada, the long-term government bond index rallied over 6% in November. The 10-year US Treasury yield is typically regarded as the best temperature gauge for assessing global economic worries and it has fallen by more than 50 basis points in the past three weeks, showing how popular the safety of fixed-income bonds suddenly is again over more volatile equities. What’s changed after a year when the benchmark yield almost tripled from 1.5% in January to a rate expected to be more than 4.3% before the end of the year? The short answer is pervading gloom about the outlook for growth, along with a bit of optimism about a retreat from peak inflation and the potentially seismic impact of a Covid backlash uprising in China.

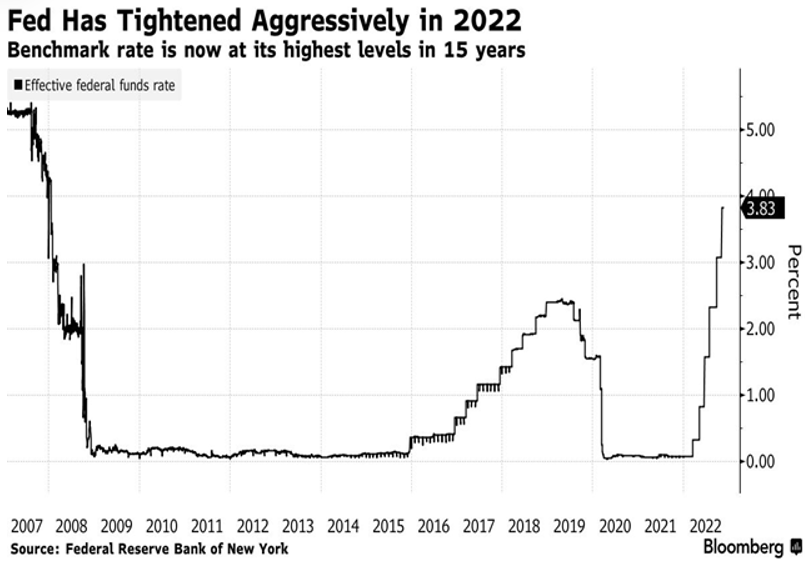

The economic data has remained relatively robust this year though, despite the aggressive moves to increase interest rates by the major central banks. That economic resilience as well as the four-decade highs in the inflation rate have empowered central banks across the globe to become even tougher on the interest rate front. The chart below shows how aggressive the rate moves have been this year compared to the ‘tightening cycle’ that began at the end of 2015. In fact, the rapidity of these rate increases has exceeded anything seen as far back as the early 1980s, when inflation was running at an annual in the ‘high teens’ (those of us old enough to remember will recall the famous target of “6 and 5” for annual inflation rates set by Canadian PM Pierre Trudeau in 1980). Those targets were eventually achieved, but only after intense ‘double dip’ recessions that the economies went through in 1981 and 1982. While the recent recovery in stocks and bonds has been predicated on some easing in rate policy by central bankers, none of those making public speeches in the past month have alluded to the possibility of a reversal of their ‘hawkish’ interest rate policies. The Fed clearly does not want to give markets a reason to rally since asset price inflation was one of the things they were trying to ‘put a lid on’.

But the tight rate policies have yet to show up in the economic data, particularly in the employment numbers in the U.S. This time around, all the damage so far has been done to the stock and bond markets, crypto and other financial assets, which had been the biggest beneficiaries of the ‘zero interest rate’ policies of the past decade. But investors shouldn’t assume these higher rates won’t ultimately drive the economy into a recession in 2023. Economies move much more slowly than financial markets and the interest rate increases take time to pass through the system. Moreover, the economy had a lot of momentum going into this ‘rate hiking cycle.’ Consumers were still relatively ‘flush’ from all the fiscal stimulus put in place during the early stages of the pandemic. Also, due to supply chain shortages, there weren’t the goods available that all consumers wanted, so inventories never got a chance to build up. Another tailwind for the economy was that services spending was still increasing due to the full re-opening of the economy, including ‘pent up’ demand for travel and other services. But the higher rates are starting to be felt in the most ‘interest sensitive’ parts of the economy, such as housing. The other reason that the higher rates haven’t slowed growth yet is that companies and consumers haven’t all rolled over debt, so they haven’t seen the direct impact of these higher rates. Supply chain issues had kept inventories very low in a couple of key industries such as autos and other durable goods. Production in these businesses has remained strong as they rebuild those depleted inventories. But once that is done, they will be facing a period of weakening demand and will have to make downward adjustments accordingly. We are already seeing that throughout the technology sectors, where hiring freezes, mass layoffs and reduced guidance all point to a negative impact on the economy next year. Moreover, 20% of Canadian mortgages were taken on when rates were at the 1.5% floor. With mortgage rates at 5%+, and 40% of this debt rolling over, the hit to consumer spending could be huge.

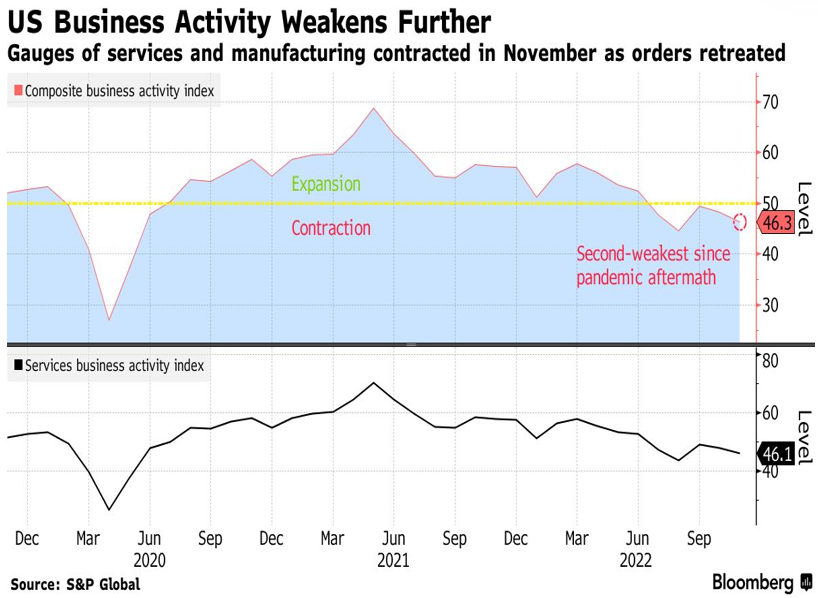

Another factor that will make these interest rate increases worse is that global financial leverage is at record levels, a result not unexpected after over a decade of zero interest rates. The cumulative impact of these rates moves will be huge. There is basically no way that the sharpest series of interest rates increases ever won’t ultimately lead to either a slowdown in growth or another outright financial accident. Our view seems re-enforced by recent comments from former Bank of Canada governor Stephen Poloz, who warned that today’s economy is more sensitive to interest rates than it was ten years ago. The full effects of interest rate hikes have yet to be felt — and will be “even more powerful” than many anticipate. High interest rates that are deterring new borrowing will also trigger a dangerous increase in debt service costs, according to the International Institute of Finance. “The global interest bill is about to surge,” the IIF economists wrote. “Higher funding costs represent a major source of risk for financial and social stability across countries with highly indebted sectors.” While the employment data and consumer spending has stayed relatively firm during the rate tightening over the past year, other more ‘forward looking’ indicators are rolling over. The S&P Global Business Activity Index (shown below) actually peaked in the middle of 2021, months before central banks even started pushing rates higher. But the cumulative effects of rising interest rates will weigh on future investment. The growth trajectory for the fourth quarter is slowing but not yet contracting. While we expect that the slowdown in global economic activity increases the risk of recession in 2023, the economy is not yet in recession. Stocks typically bottom about six months before the end of any recession. But, outside of the anomalous case of the Covid pandemic in 2020, there are no historical cases where we saw the final low in stocks even before the recession began!

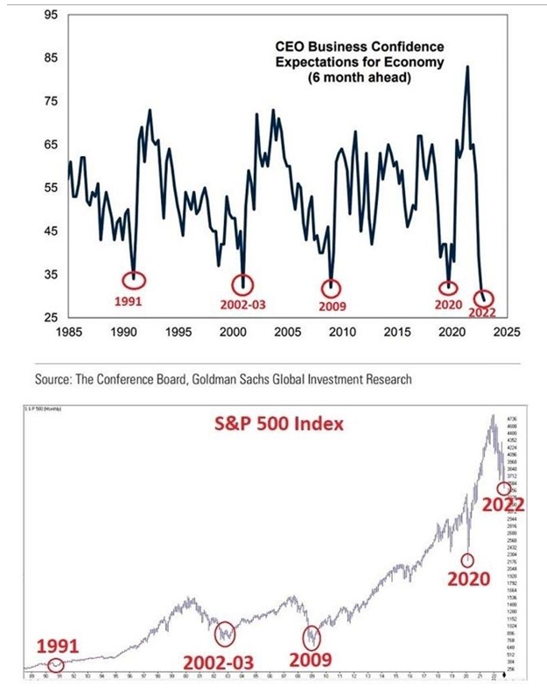

Putting all the charts aside for a second, we also want to consider the ‘wealth effect’, which is the impact that changes in consumers perceived wealth impacts their spending habits. With the prices of stocks, bonds and housing all sharply lower in 2022, the simple reality is that the wealth effect will be negative! The dour economic outlook can also be seen in the CEO Business Confidence Surveys for the six months ahead, which have fallen to the lowest levels in over 40 years, below those seen immediately after the initial Covid shutdowns in 2020 as well as the period around the Financial Crisis in 2008. This will be reflected in both capital spending by business as well as hirings and employment levels. We have never seen such a sharp drop in business confidence without a subsequent recession!

For the ‘silver lining’ crowd, the only good news for investors in this scenario is that those lows in business confidence have often coincided with the cyclical lows in the stock market. While the warning signs about a likely recession in 2023 are clear, history has shown that periods of extreme worry have actually been good buying opportunities. Moreover, stocks have now bounced off their lowest level on three occasions (June, September and October) and have shown resilience at those levels that we expect could hold as cycle lows. We have made note of all these thoughts for our yearend investment strategy and outlook for next year. Weak capital market results in 2022 have created some good investment opportunities which are hard to ignore when investing with a somewhat longer time horizon and a moderate ability to absorb shorter-term risks. While we still see a good chance of a full recession in 2023 and therefore an upcoming reduction of earnings estimates and consequent risk for stocks, this should also mean lower inflation and an end to the aggressive rate hiking cycle. That will provide a positive backdrop for bond prices in particular and we have added to our long-term government bond holdings in both the U.S. and Canada. Longer duration stocks (i.e. in the tech, telecom and health care sectors) should also do better going forward as earnings growth will be stronger in those sectors and multiples should not contract any further since we expect to see peak interest rates early in 2023. Consumer cyclical and industrial stocks, however, will face more headwinds due to slower economic growth. Energy should do better than most cyclical stocks due to exceptionally low long-term valuations. Financial stocks such as banks will struggle due to rising loan losses, inverted yield curve and lower capital markets activities. However, valuations in Canada are already at low levels and we also don’t foresee any risk of dividend cuts, so losses should be contained. Telecom and pipeline stocks as well as REITs provide better potential, though, in those high yield sectors. We have also taken another look at the metals sector as the stocks are incredibly undervalued and they could rally if we get some expected weakness in the US dollar. Gold stocks in particular look like great value and we also see opportunities in some copper names such as HudBay Minerals and First Quantum.

The other big market news in November was the collapse of crypto company FTX, which filed for Chapter 11 bankruptcy protection. The crypto powerhouse, once valued at $32 billion, collapsed in a matter of days amid a liquidity crunch and allegations that it was misusing customer funds. The Securities and Exchange Commission and the Department of Justice are investigating. We had not put any client money into crypto currencies despite the prior strength and popularity of investments in that asset class. The issue we had and continue to have were both the lack of regulation, the protection of capital and, most importantly, the lack of any clearly visible advantage of using a crypto over any other type of electronic payments system, especially since those other digital payment systems are all backed by reputable financial institutions. Crypto currencies are not yet embedded in the life of most consumers. We don’t use it, we don’t spend it and we don’t think of it as a medium of exchange or currency. It isn’t in most pension funds outside of the major players such as the Caisse de Depot or Ontario Teachers Pension, which always have at least some representation in these potentially emerging technologies. Most importantly, though, if anyone asked you what problem in your life it might solve, you probably wouldn’t be able to think of any. Crypto believers tell us that thanks to its limited supply, Bitcoin is an excellent inflation hedge and therefore a fantastic store of wealth. But while scarcity combined with usefulness or desirability creates intrinsic value, scarcity in itself does not. Is there then a good use case for crypto that will add value over time? Believers say yes — that it is transferable, easily divisible, liquid, independent of government and private, and that these things make it desirable.

Speculators have definitely made some substantial gains over the past few years on the surges in crypto trading and new money flowing into the sector. On the lighter side of that development however, the following YouTube video should remind investors about the risks of ‘following the crowd’ into hot money trades. Buyer Beware!

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.