Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

June 1, 2017

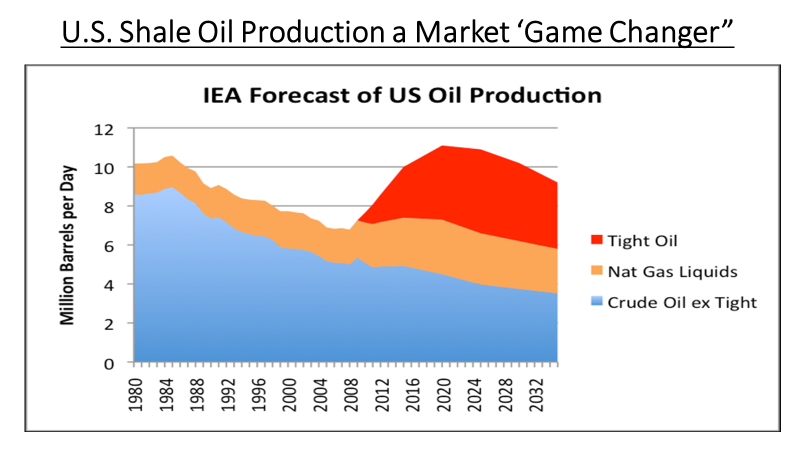

The stock market response was definitely ‘sell on news’ as energy stocks came under further pressure for the balance of May, making them the worst performing sector for the month. The problem has been two-fold. First of all, demand growth has been weaker than expected in the world’s two largest economies, the U.S. and China. But the bigger factor is the resurgent production in U.S. ‘tight’ oil. The shale producers have been shown to be very adept at moving quickly to put oil rigs back to work and to reduce their costs so that they are profitable with prices as low as US$40 per barrel. So while OPEC and its partners can continue to cut production, all they will end up doing is giving up market share to the unrestricted production from the U.S. The chart below shows how shale (tight oil formations) production has reversed the 20-year decline in U.S. oil production by adding close to 4 million barrels per day of production since 2009. Add to that the long-term reduction in gasoline demand as electric vehicles become a larger part of the global auto fleet, we can see why oil prices look like they should be range-bound between US$40-60 for the foreseeable future.

Despite not having a particularly bullish outlook for the price of oil, we have been adding to positions recently including Crescent Point Energy, Tourmaline Oil, Spartan Energy and Trinidad Drilling. Aggressive U.S. selling of Canadian oil stocks this year have caused them to take a bigger hit to valuations than their southern neighbours, with many good quality companies now trading at lower levels than they were in early 2016, when oil prices were under US$30 per barrel. This has created a good relative buying opportunity up here as the stocks are trading at low cash flow multiples despite improved debt positions versus early 2016. Moreover, analysts are now using more reasonable oil prices of US$52 in their models rather than the US$55-65 expectation that was being used in earlier reports. The foreign selling is no doubt related to the weakness of our currency, the risks from renegotiating NAFTA, weak gas prices and the recent BC election results (which have put the future of the TransMountain Pipeline expansion in doubt). That certainly fits the bill of Warren Buffet’s famous line about trying to be “greedy when all others are fearful.”

John Zechner

Chairman and Founder

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.