Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

October 1, 2025

Economic Outlook. Growth is clearly slowing as evidenced by recent employment numbers in the U.S., comments from the regional bank heads in the updated Beige Book as well as the negative print on 2nd quarter GDP in Canada. Strong consumer spending over the past few years was supported both by Covid support as well as exceptionally strong labour markets. Those impacts have lessened dramatically and even cutting short term interest rates won’t make a big difference. Consumers spend because they have jobs and cutting rates a ¼ point won’t change that and stimulate any quick turnaround. The global economy is still on course for a substantial blow from Trump’s trade measures despite showing greater resilience than expected in recent months, the OECD said. In new forecasts, the Paris-based organization raised its 2025 outlook for world growth and most individual economies, citing the impact of front-loading in anticipation of higher tariffs. The U.S. also saw strong investment in artificial intelligence, while China benefited from fiscal support. But the OECD made little change to its 2026 predictions, when it expects global growth to drop to 2.9% from 3.2% this year and expansion in the US to slow to 1.5% from 1.8% amid higher import duties and elevated uncertainty. The impact of tariffs continues to be underestimated, in our view. The largest increases only came in early August, and we continue to get new tariffs on a weekly basis. The net impact will see the highest increase in global tariffs in almost 100 years, with U.S. tariffs on imports rising from under 3% to over 15%. Companies have initially absorbed much of the increase, but they won’t be able to continue to do that without seriously hampering profit margins. Tariffs will ultimately show up either in inflation numbers or reduced corporate profits (and the standard ‘knock on’ impact to the rest of the economy). Neither scenario is positive for stock prices!

Despite the overall risks, the very recent economic data has painted a surprisingly bright picture of recent trends. Consumer spending in August was stronger than expected and so was income. Companies and households continue to order big-ticket items while inflation has been relatively soft. Even housing showed signs of life, with new sales hitting a three-year high in August. Previously, such trends had been powered by trillions in stimulus from both congressional spending and low interest rates and liquidity injections from the Federal Reserve. But the narrative now is shifting towards the ever-popular wealth effect coming from Wall Street and a succession of new highs in major stock indexes despite lofty valuations. Simply put, almost all the spending is coming from the well-to-do high-income high-net-worth households that are seeing their stock portfolios rise and they’re feeling a lot better off and they’re spending. The risk with that scenario is when that ‘chain of causation’ starts to work in reverse, with any pullbacks in the stock market driving the economy in the same direction.

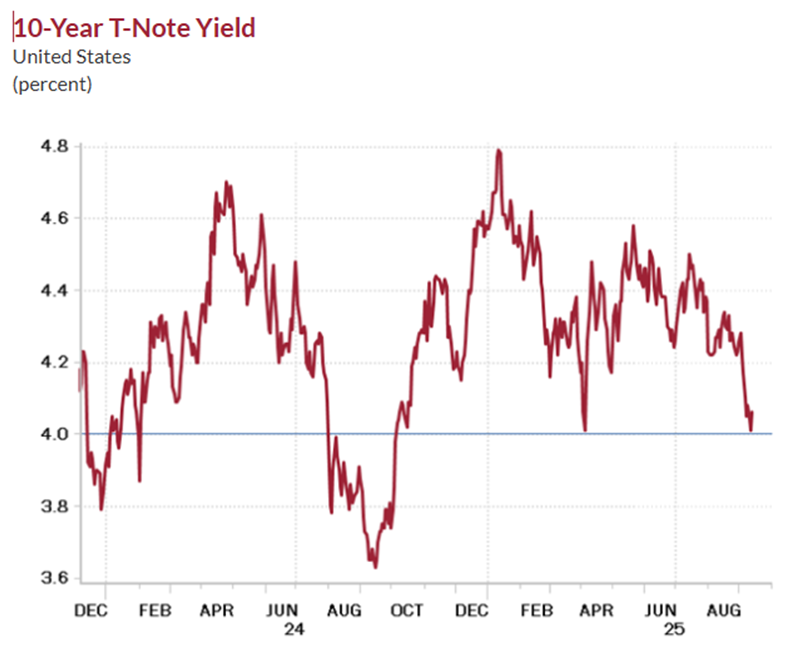

We have adjusted our bond market strategy and lightened up on long bond positions on recent strength, despite our view of slowing economic conditions. While we expect short term rates to go lower, we think that ‘sticky’ inflation and worries about too much easing will keep long bond yields near current levels and maybe even a bit higher. The risk is that the combination of lower interest rates and ongoing fiscal stimulus keep inflation at elevated levels. We reduced long-term bond holdings on last week’s rally and look to move some of that into mid-term corporate bonds or preferred shares. The potential volatility in the structure of the U.S. Federal Reserve and the greater influence over interest rate decisions from the White House have increased the risk that we see long-term interest rates rise even as short-term rates fall. President Trump is attempting to rid the Federal Reserve of the ‘interest rate hawks’ and replace them with his own choices, all of whom would be more receptive to following the White House wish for much lower interest rates. If this were to occur, we could see the next Fed chief become “Arthur Burns 2.0”, a reference to the disastrous term of the Nixon-appointed Fed chief during the 1970s, who acceded to the White House push for lower rates that resulted in inflation at double-digit levels and short term interest rates rising to the mid-teens as the decade ended and a subsequent ‘double dip’ recession in the early 1980s. Looking at the chart below, we are going to have to see almost recessionary economic conditions to drive 10-year government yields below the key 4.0% threshold.

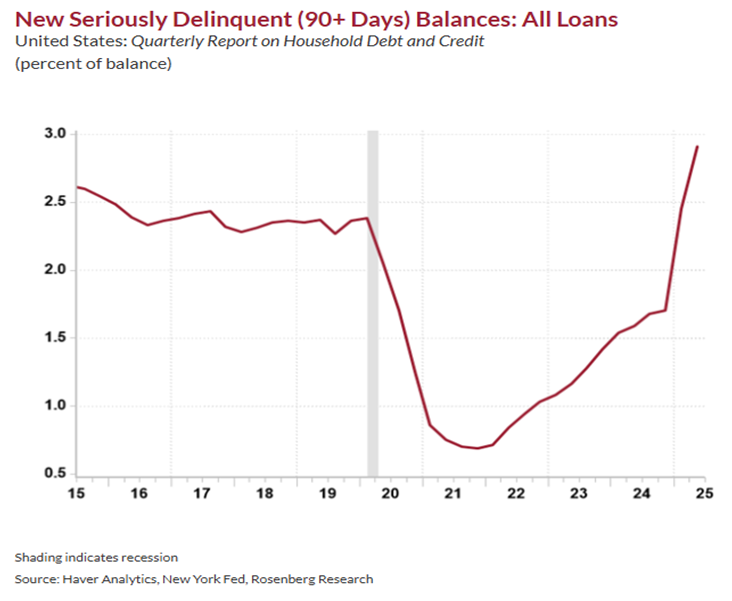

Another economic worry is that the debt bubble continues to expand, and it is not just at the government level. U.S. household debt has expanded every quarter since the 3rd quarter of 2020 to a record $18.4 trillion. More than half of the consumer spending growth we have seen since that time has been fuelled by leverage. Household debt per capita just topped $63,000 for the first time on record and is more than 20% higher than the ratio was heading into the 2008 Great Financial Crisis. But the problem is that loans are now piling up in a lagged reaction to the Fed’s ongoing tight policy stance, with the share of debt shifting into serious delinquency moving up to near 3.0% for the first time in eleven years and very nearly where it was in the third quarter of 2007. Against this background, the banks have sharply curtailed their loan growth to the household sector to low single-digits. The era of loose credit conditions for the consumer has come to an end, and this is a risk for the banking sector is they lose the tailwind of strong economic activity.

Our lack of conviction about the continuation of the stock market advance is that it is occurring in the face of no real improvement in the inflation numbers, an ongoing lack of clarity about the trade landscape and its impact on the economy as well as investor sentiment readings that are moving back to the levels we have seen at most market peaks. The stock market is priced 0% for a recession even though real GDP has contracted in three of the past five months, with the year-over-year trend in growth receding sharply from +3.2% a year ago to a ‘stall-speed of’ +1.3%. The incoming data has shown no significant rebound, and we continue to see weak results from leading economic indicators such as home sales, housing starts and weekly employment claims. Still, the consensus really believes a recession will be avoided. The valuation of the stock market is back to record levels and priced for zero risk. That seems to be a very unattractive risk-reward trade-off for stocks over the balance of the year despite the strong momentum and bullish sentiment going into the final quarter of the year.

The worst could be past for the Canadian telecom sector. After rising sharply during the pandemic when customers were all home using much more online content and the networks of the big telecom providers proved quite resilient to the increased traffic, the sector has lagged sharply over the last few years due to a confluence of negative factors. That included increased debt to fund capex, reduced immigration (particularly foreign students who were one of the greatest sources of new sub adds) and the additions of a more powerful 4th player in wireless, which came about after Rogers bid for Shaw Communications necessitated the sale of Freedom Mobile to Quebecor. In the process, telecom stocks fell to multi-decade lows in valuation. Almost all those headwinds seem to be passing now. Pricing discipline has returned to wireless; subscriber growth has started rising again, ARPUs have stabilized, and the major players have begun selling or monetizing ancillary assets pay down debt. For Rogers particularly, the value of their sports franchises, now ranked in the top 10 in the world, is not reflected in the stock. Deals in the National Football League the past few weeks valuing both the New England Patriots and Chicago Bears at US$9 billion each, among others, are indicative of escalating values in that industry. TELUS, Rogers and BCE all trade in the 6-8 times cash flow range, have strong dividend yields and are generating positive cash flow growth.

There is a new 800-pound gorilla in technology. In one of the largest cloud contracts ever signed, OpenAI has inked a deal with Oracle to purchase $300 billion worth of computing power over the next five years. It also said it had signed four multi-billion-dollar contracts with three different customers, giving the company $455 billion in “outstanding contract revenue” that it expects to collect on. While this solidifies Oracle’s position as the #4 player in cloud computing, it could also signal the potential loss of market share and growth for the current three largest players in cloud computing; Microsoft, Amazon and Alphabet.

Investment strategy update and changes. Cash levels have risen slightly in most of our accounts, but this was due more to reducing positions in long-term bonds on the recent rally and moving some of that money into mid-term corporate bonds and preferred shares. In the stock market we have added to positions in interest sensitive sectors such as telecom and energy infrastructure, including Telus, Rogers, Atkins-Realis, Northland Power and Capital Power. In addition to our holdings in gold stocks, Torex Gold and B2Gold, we are seeing building of strategic reserves in other key commodities, including copper, uranium and oil, mainly by China. With the ongoing weakness in the U.S. dollar, this has put a bid under some key commodity names, and we recently added positions in Nutrien, Sprott Physical Uranium Trust and Teck Resources. We remain underweight oil stocks but did add natural gas producer Arc Resources. In technology, we lightened up on ‘big tech’ names Amazon, Alphabet, Oracle and Nvidia.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.