Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jacqueline Ricci

January 30, 2023

A Challenging 2022…What’s Next…

The past year was one of many challenges. At the outset of the year, the Fed seemed to be behind the curve on its inflation call, arguing that inflation was “transitionary”. Their tune changed quickly and by early March the Fed began raising the fed fund rate aggressively. In total Powell raised rates seven times throughout 2022, taking the federal funds rate from 0.25% to 4.50%.

Inflation remained sticky, only showing signs of rolling over more recently. The yield curve, a reliable predictor of impending recessions became and remains inverted. At any positive action in the market, Fed officials would come out and aggressively state the need for them to remain tighter for longer to beat inflation expectations down.

On the global front, Russia invaded Ukraine in February 2022. Adding to an already challenging geopolitical backdrop. This aggression sent energy prices soaring for much of 2022 adding to an already strong inflationary backdrop.

There were very few places to hide in 2022. Bond markets as well as equity markets suffered. The worst areas of the market were the highly valued growth stocks that have been leaders for almost a decade. Technology and interest-sensitive (such as real estate) performed the worst. The one bright spot was energy which fared well given the tightness of supplies due to the industry’s new capital discipline and European demand for alternative energy sources caused by the Russia-Ukraine conflict.

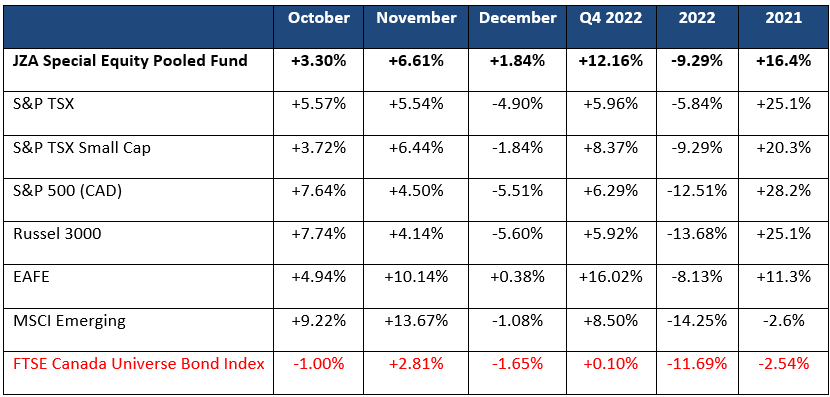

Below is a chart of the global equity market returns for last year. We have also included a bond market index to highlight the general destruction of value in other asset classes. Of note, is that Canadian equity performed better than most markets. This is a result of the higher energy weight in the Canadian indices and lower technology weight.

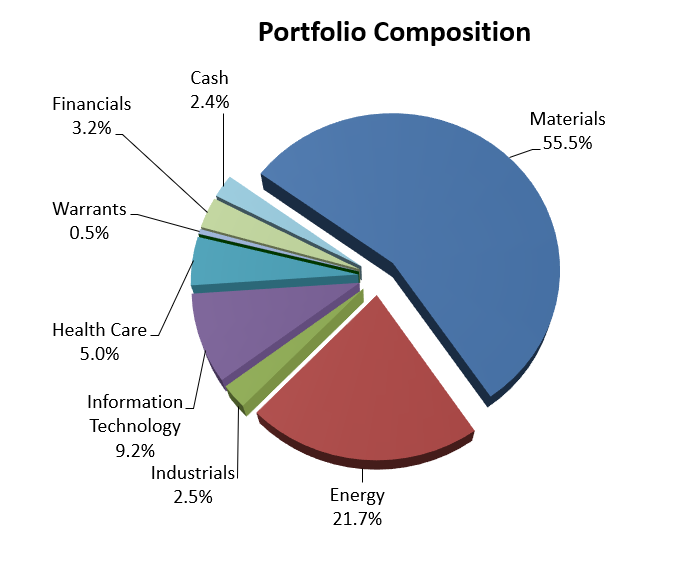

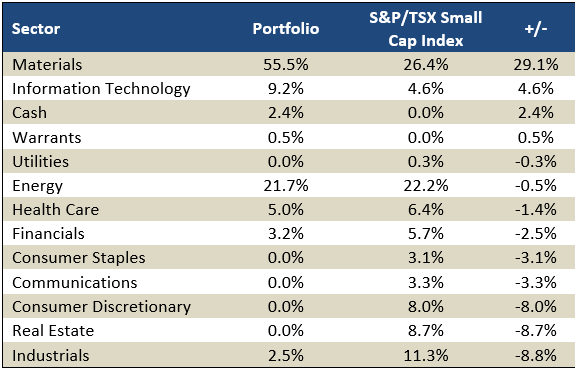

Below is a breakdown of the portfolio’s characteristics as of December 30, 2022. The portfolio has significantly increased its technology sector weight in the last few months after the aggressive sell-off. The portfolio has also decreased its energy overweight in favour of other areas The gold and base metal sector weights have also been increased. Some of the portfolio’s special situations have been reduced after being taken out. We are continually looking for other special situations to add to the portfolio, especially in the industrial sector.

What Worked, What Didn’t

In the fourth quarter of 2022, the three names that detracted the most in the portfolio were New Stratus Energy, Lifespeak Inc., and OpSens Inc. Collectively these three names cost the portfolio -1.9%.

New Stratus Energy is a Canadian Oil and Gas company in Latin America. In the fourth quarter, the company was informed by the Ecuador Government that it will not fulfill its commitment to provide an extension and migration of the contracts for Blocks 16 and 67 and their permits will expire. Although the company was shocked at the sudden change, the company has sufficient capital to pursue other opportunities. Although disappointing; given the stock is trading at its cash position, we intend to be patient and see if management can benefit on other opportunities they have.

Lifespeak is a mental health and well-being platform that provides expert education and advice through technology. Employers opt to provide Lifespeak’s platform to their employees through the company’s benefit plans. Prior to purchasing shares in the company, Lifespeak lost a significant customer which dropped the stock over 70%. We bought the portfolio position after the selloff because we felt there was sufficient value in the company and its award-winning platform would be taken up by others. Loblaws has subsequently started to roll out Lifespeak’s platform to all employees. However, given the challenging environment in technology stocks and the negative economic backdrop we have begun selling the position as the next few quarters will likely be difficult and there are better opportunities elsewhere.

Opsens develops, manufactures, and supplies fiber optic sensor solutions for the medical, oil and gas, energy, and laboratory industries. The company’s main focus is currently in interventional cardiology, where it offers advanced optical-based pressure guidewire to improve the outcome of patients with coronary artery disease. The company is currently going to market with its SavvyWire and TAVR solution. Breaking into medical markets is challenging but we like the companies’ prospects with two breakthrough products. The stock sold off aggressively in the fourth quarter and have recently added to the position.

The three names contributing the most to performance in the 4th quarter are Magna Mining Inc, Capstone Copper, and Magnet Forensics. These three names contributed +6.0% to performance in the 4th quarter.

Magna Mining is a nickel-copper exploration and development company in the Sudbury region. Last year the company made a transformational acquisition in the Crean Hill Mine. We participated in the funding of the acquisition. The company has two significant assets with known reserves of nickel/copper and is fully permitted. This seasoned management team (previously with FNX Mining) will drill up the asset and expand the resource base. This complex will be brought into production relatively quickly given the spare processing capacity in Sudbury and their existing permits. The stock has been a massive performer (up +266% in the fourth quarter) it is still under restriction. The hold period expires in January, and we expect to take profits but maintain a full position.

After a significant base metal sell-off through most of last year, copper stocks began outperforming towards the end of 2022. Capstone Copper, one of the largest positions in the portfolio, gave the portfolio a strong bounce when it appreciated over +75% from June 30th to Dec 30th. We bought Capstone stock in July, August and October on market weakness. With the negative economic backdrop last year, copper had sold off significantly. However, inventory levels remain exceptionally tight, the energy transition narrative is still proceeding, and China, which followed a zero COVID policy last year has begun reopening. Although we are mindful that the rest of the world may be entering a recession, we feel most of the negativity is priced in the commodity and stocks. China’s reopening and recovery should also provide a positive backdrop for the red metal. The portfolio took some profits in Capstone recently but still holds a large position.

Magnet Forensics provides law enforcement and government with digital investigation software as a service. Integrating built-in investigative analytics, artificial intelligence, and automation on the cloud helps investigators see the whole picture. The company is focused on a go-to-market strategy with a very concentrated consumer base. The management is strong, has significant ownership and is focused on profitability. The portfolio purchased its position during the technology sector downdraft between $17-$19 in June. With the stock trading over $$37 we recently reduced the position but still hold a meaningful position.

Where to in 2023

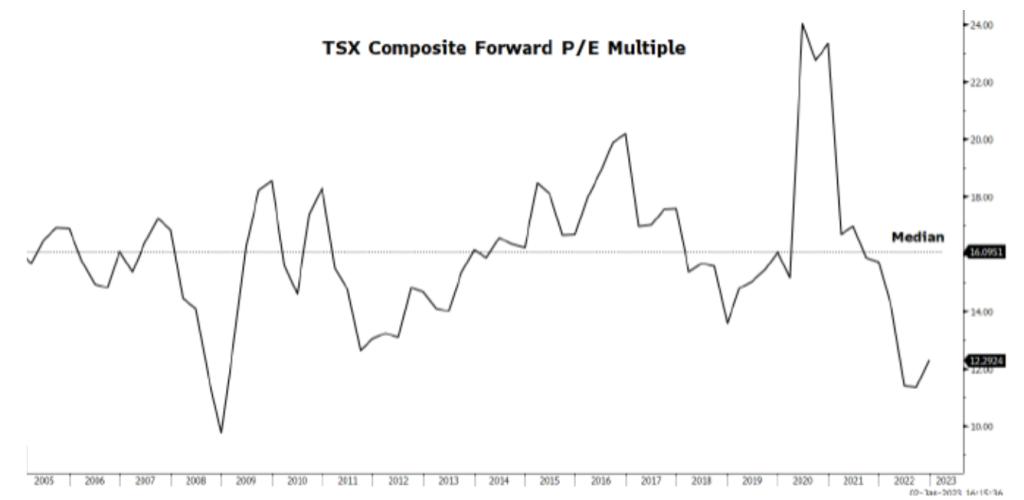

We are cautiously optimistic but do not believe we have been given the all-clear signal. Markets have sold off aggressively, but Powell has not yet pivoted and does not appear likely to do so soon. P/E multiples in Canada have sold off significantly as can be seen below. Canadian equities valuations appear inexpensive versus the historical average with the TSX Composite forward price/earnings multiple trading at 12.3x versus the long-term median average at 16x.

While the TSX Small Cap Index was down last year, it has held significant technical levels and appears to be trying to move higher (see chart below).

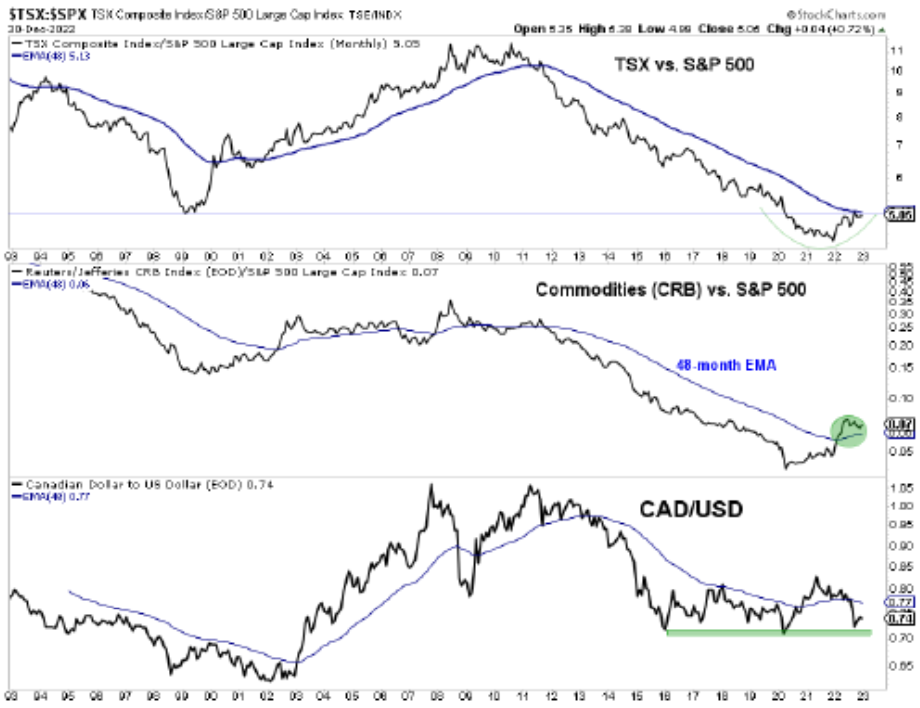

We have stated for some time that we believe market leadership is changing from high-valuation growth stocks to hard assets like energy, gold, and base metals. We believe this transition has begun. In this environment, Canada will outperform the US indices. This emerging trend is already starting to form and is being advanced by US dollar weakness.

The area we are currently most comfortable investing in near-term is in the golds and precious metal stocks. The US dollar is finally showing signs of exhaustion. Inflationary pressures on the cost side seem to be abating and ultimately, we believe the Fed will pivot in the coming months as inflation has peaked. Gold, although not recession proof is recession resilient and provides some safety to the portfolio if the recession looms deeper than anticipated. The portfolio’s overweight in gold stocks is a good offset for the more aggressive positioning in other commodity sectors.

We prefer base metals over energy given that China’s reopening favours base metals. Inventory levels are at extremely low levels and eventually the market will look beyond the economic slowdown and value base metal stocks on their long-term opportunities from the energy transition.

The energy sector is still favourable given the incredible capital discipline the group has committed too. Energy transition will keep valuation multiples muted but cash flow yields will remain strong, and the industry appears focused on returning capital to shareholders. Given our thesis that hard assets (commodities and commodity stocks) will be the next cycle’s leadership, we continue to assess the technology sector cautiously. It is unlikely that we are going to return to the era of aggressive growth multiples in 2023. With an ultimate slowdown approaching and the fast pace of interest rate increases we are concerned about the leveraged consumer and businesses that require discretionary spending. While large cap businesses have increased debt over the last few years, the small cap companies we focus on are entering this new environment with healthy balance sheets and strong fundamentals.

As said at the outset, we are cautiously optimistic. We believe much negativity has been priced into stocks but realize there could be another “shoe-to-drop”, particularly if the recession is deeper than expected. However, while this year will be challenging, we anticipate that stock markets will be higher in 2023 and small cap Canadian growth companies will outperform most asset classes.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.