Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jacqueline Ricci

February 9, 2022

OUTLOOK

As we enter 2022 there are still many crosscurrents. The consolidation of the previous 2020 equity run should most likely be in its final stage. Omicron, however disruptive globally is showing signs of the worst being over. The Fed has spoken, and the market’s volatility shows that the market is coming to terms with rising rates. The reason for the change in the Fed’s stance appears to be that inflation is not transitory and needs to be monitored and controlled. China and other emerging markets have come through a difficult 2021, with China increasing stimulus to reinvigorate their economy. As we move through 2022, we believe we will see further rotation from growth stocks (largely technology) in favour of value (largely resources). Part of this rotation is related to valuations and the pressure higher interest rates will have on high multiple stocks. The other consideration stems from the continued tightness experienced in the commodity sector, be that oil and gas or base metals causing upward pressure in pricing with valuations remaining quite low.

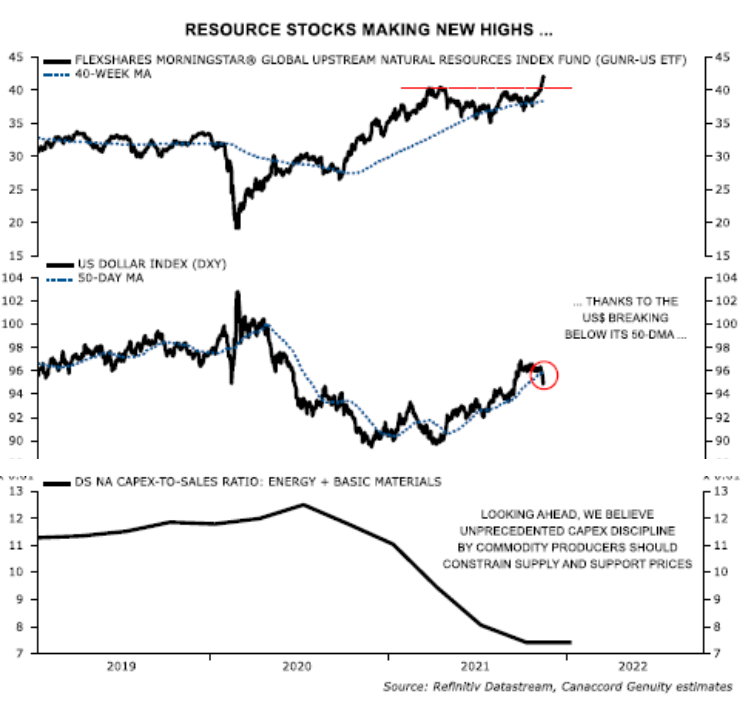

To illustrate this point, the MorningStar Global Natural Resources Index rose to an all-time high in early January (see chart on next page). Factors supporting the advance include the recent break of the US$ below its 50-day moving average and the strong price appreciation of commodities. Another factor helping commodities advance is the unprecedented capex discipline exhibited by commodity producers which is expected to constrain supply in the medium to long term. Importantly, we believe current valuations are far from pricing-in 2022 year-end targets for crude oil ($85/barrel) and copper ($4.75-5.25/lb). With this backdrop we remain committed to our overweight positioning in energy and basic materials. In these resource-based sectors we also like the uranium stocks, as well as EV based raw material stocks mining lithium, cobalt, and graphite.

The gold sector was perplexing in 2021. The backdrop for the gold price was very favourable with higher-than-expected inflation and while the gold price has held in around $1800/ounce, gold stocks have struggled (the S&P/TSX small cap gold sub-sector was down -18.1%). Many argue that the next generation of investors will use cryptocurrencies as a hedge for inflation. We believe this reasoning is flawed, as there is little correlation between crypto and inflation. While some patience is likely needed as we move into the new year and interest rates continue to rise, we strongly believe we will get a good move in the underlying commodity and the stocks as real rates remain negative. Not to mention we have finally begun to see some M&A in the gold space as senior gold producers start to look to replenish their pipeline.

We also continue to look for unique growth ideas in other areas of the small cap market. The last half of the 2021 proved to be one of the worst IPO markets in memory. Although there were some interesting companies’ that became public, their valuations were very aggressive and many of these issues are trading well below issue price. As these growth stock valuations come in, we anticipate buying some of these companies (but at this juncture, many of their valuations are still too rich).

As we have already seen in the first few weeks of 2022, volatility is elevated and will be around for the immediate future. We will continue to navigate these markets, by remaining nimble and alert as to opportunities in the Canadian small cap market.

We look forward to 2022 with optimism. Wishing all of you a healthy and happy upcoming year.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.