Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jacqueline Ricci

April 24, 2020

The main detraction to overall returns from an industry perspective was the material sector (ex-golds) as base metal prices were negatively impacted due to the lack of demand from the economic shutdowns. Also, the nature of the portfolio having a smaller than average market capitalization would have detracted from returns as liquidity dried up.

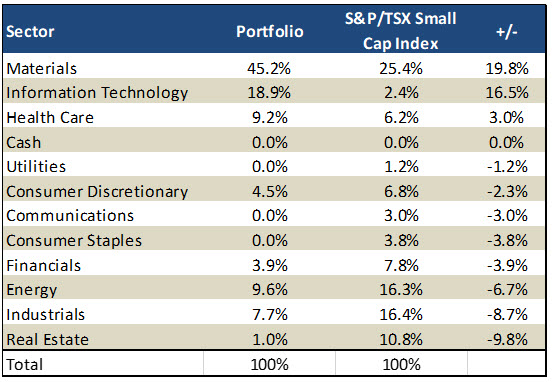

Below you can find the characteristics of the portfolio relative to the TSX Small Cap index.

The names hardest hit in the portfolio include GoEasy Ltd., Torc Oil and Gas Ltd. and Kelt Exploration Ltd. Collectively these three names cost the portfolio -4.0%. Of note, two of these names are from the Energy sector. What happened to energy in the quarter? Energy has been struggling for some time as the US continues to increase its production rate relative to the rest of the world with the focus of the production being the prolific Permian Basin. As the US has continued to increase production, the OPEC nations, led by Saudi Arabia, clearly had had enough. At the March 6th OPEC meeting, instead of agreeing on further production cuts the Saudi’s and Russian’s surprised the market and decided to open the spigot and increase their production substantially. This threw the energy market into a tailspin. This increase in production came at the worst possible time as the Covid-19 pandemic was getting underway and energy demand was falling off a cliff. Of note, 50% of all demand for energy in the Western world comes from transportation and I do not need to tell anyone how often we are all using our cars right now. From that point, oil prices began their free fall with WTI falling from $46 (prior to meeting) to a low of $20 on March 31st. With no demand, refiners are also slowing production. When oil that has been extracted is not consumed, it is stored, and there is only a finite amount of global storage. As storage fills and the system backs up, differentials blow out exasperating the issue until producers are forced to shut in production. Given this backdrop, it is not surprising that two of the worst performers in the portfolio were oil and gas producers. As mentioned before, we had reduced the portfolio’s exposure in January by taking the energy sector to a significant underweight. Post the fall in energy prices in March, we have picked away at both Torc and Kelt as well as other names in the sector that we believe have the balance sheets that can survive this downturn. We believe the current price environment is extreme and not sustainable as it does not work for any party on a global basis, including the low-cost operator, Saudi Arabia. However, it can not be fixed quickly with demand also being curtailed. Valuations in the sector have reached incredibly low levels (assuming energy prices can rebound modestly in the back half of the year). As this is our base-case view, we have taken the energy weight back up. After the quarter, OPEC reintroduced production cuts but there will be little relief to price until demand picks up. On the announcement of this cut and an initial upward movement in the stocks, we have again reduced the portfolio’s weight to the energy sector in April.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.