Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jacqueline Ricci

January 24, 2020

Kew Media Group operates as an independent media content company. The company produces and distributes a catalogue of film, television and digital assets across a range of viewing platforms. The company has grown aggressively over the last few years through the acquisition of other independent production companies. Last quarter the company reported disappointing financial results and announced their CFO was being released for providing inaccurate financial information. The company also announced it had formed a special committee to examine strategic alternatives. Given the quality of management and the board, we are surprised by the revelations and await further information.

Reunion Gold is a gold exploration company focused on the Guiana Shield assets in French Guiana and Guyana. The team are seasoned explorers in the region dating back many decades. After some early success with their Dorlin project, the latest results were underwhelming. Following the results, the company raised equity to finance their current drilling program. The Guyana properties are part of a strategic alliance with Barrick and is funded. The portfolio had trimmed the position on the initial early success of Dorlin and will now await further exploration results.

Outlook

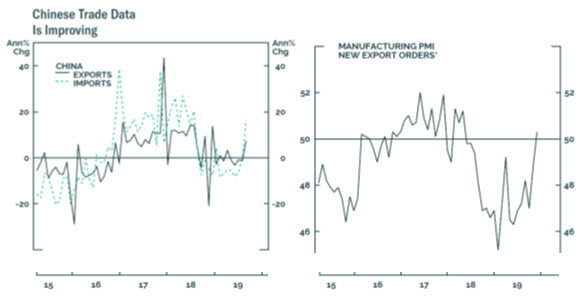

It appears that 2019 was about climbing the wall of worry. We started the year with the Fed tightening monetary policy, but as recessionary fears mounted, the Fed reversed course and followed with three interest rate cuts during the summer. Along with the recessionary fears, trade worries mounted as Trump placed more tariff and sanctions on China. Adding to global concerns were Brexit and more Middle East unrest. In reaction to these headwinds, global central bankers stimulated their economies which reduced global risks and propelled stock markets higher. After the impressive gains in 2019, we anticipate that markets will need to work off overbought conditions before moving higher. The global economy is entering 2020 on a weak note with 70% of OECD countries economic growth decelerating. Inventory destocking will likely continue and further hamper growth in the first part of 2020. However, over the next 12 months we are positive on equities. Easier fiscal conditions, a turn in the global inventory cycle, looser fiscal policy and Chinese credit easing should all support global growth. Already this year China data is showing improvement.

With a reacceleration of global growth in 2020, cyclical stocks should fare better than defensives. As a result, non-US stocks typically outperform their US peers when global growth accelerates. With stronger global growth outside of the US, we anticipate that the US dollar should weaken which should boost commodity prices.

Where does that put the portfolio? The portfolio entered the year overweight material, technology and energy stocks. Last quarter we increased the energy weight in the portfolio on low valuation and slowing US oil supply growth (specifically in the Permian). Not only has the US oil production slowed, but the capital available to US companies has also dwindled.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.