Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jacqueline Ricci

February 7, 2017

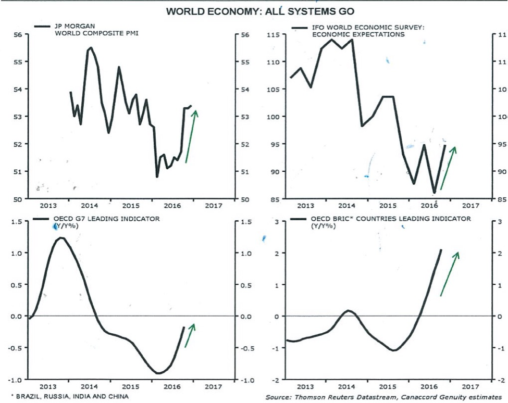

The fourth quarter brought much change and confusion. In November, the US voted in Donald Trump as President, followed by an interest rate hike in December by the US Federal Reserve. Post the election, financial markets viewed Trump as pro-business causing a strong rally in the US dollar and equity markets. Gold sold off sharply, surprising many of the gold supporters while base metal prices rallied. As we set up for 2017, the bulk of leading economic indicators (LEIs) that we track are pointing toward improving global growth. With the OECD Leading Indicator, Global PMI’s and the IFO World Economic Expectations index all in a strong uptrend, we anticipate that we are entering a new phase in the economic cycle, one where global growth accelerates and synchronizes between developed (DM) and emerging market (EM) economies.

As global growth accelerates into 2017, we expect the previous disinflation concerns to be replaced by rising inflation expectations. Add in the expectation that Trump will launch fiscal stimulus, and we anticipate that Canadian small cap stocks will experience another strong year.

The fund is poised to take advantage of stronger global growth by overweighting the material sector (with a focus on base metals). The underinvestment in the mining industry, has led to very few new projects and means that any material increase in demand will lead to higher base metal prices. We also believe that the energy sector should do well in a higher growth world, however new supply is more plentiful and will cap oil and gas pricing. As such the portfolio is slightly overweight energy but not to the same degree as base metals. Within the energy sector, the portfolio is overweight gas stocks which will likely be reduced as we move through the winter heating season in favour of oil service stocks. The portfolio has increased its position in gold stocks again as we anticipate gold to benefit from higher inflation concerns and strong seasonality demand (historically January and February are positive for gold). Within the gold sector, we have increased the fund’s holdings in producing assets with strong balance sheets over exploration companies with higher funding needs. As always, we continue to search for special growth situations in new industries and sectors but are watching carefully the Trump administration and any new policies that might adversely affect Canadian exports (especially Canadian manufacturing, and energy companies).

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.