Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jacqueline Ricci

November 2, 2018

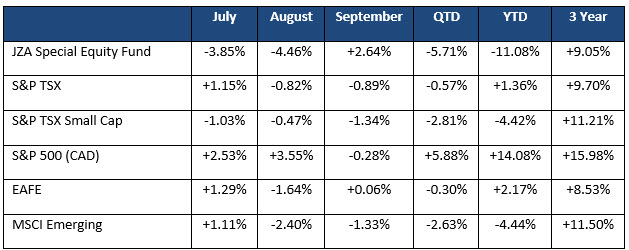

The third quarter was a challenging environment for non-US investors. Global equity returns showed the US markets climbing “a wall of worry” with the S&P 500 posting a +5.9% return, while most international markets struggled. Canada continued to underperform due to its large weight in cyclical stocks. One of the hardest hit equity markets was the TSX Small Cap Index which fell -2.8% last quarter and is down 4.4% YTD.

The return for the portfolio this quarter was disappointing as we saw money continuing to move out of Canada with several international sell programs pressuring small cap stocks. The portfolio was down -5.7% and underperformed the TSX Small Cap Index by -2.9%. The summer doldrums exasperated performance with low liquidity causing continued volatility in small cap stocks. The one area of the Canadian small cap market that continues to outperform and attract capital is the cannabis sector (largely from retail investors). However, we are getting very concerned that the valuations are excessive and unrealistic. With many cannabis stocks valued at huge multiples on future/potential metrics, we look forward to legalization; so we can start seeing what the sector’s “real” economics are. While we are positive on the industry long-term, we believe the stocks will likely experience a significant correction in the next few months. Accordingly, we have reduced the portfolio’s exposure to less than 2%. As mentioned in previous quarterly letters, Cantrust Holdings remains our preferred stock in the cannabis sector. With a strong management team, good operation capabilities (lowest price per gram growing stats), relative “low” valuation and focus on the medical market, we anticipate Cantrust will emerge as one of the market leaders. We believe that, similar to the tech boom in the late 1990’s, cannabis stocks and the sector as a whole, could face a “race to the bottom” and only the strong will survive to lead the way. We are watching this sector carefully.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.