Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jacqueline Ricci

July 31, 2017

The second quarter of 2017 proved to be challenging, with the month of June being particularly tough. Small cap stocks in Canada fell in Q2, with the S&P / TSX Small Cap Index falling -5.5% leaving the index down -4.1% in 2017. The Canadian large cap market faired better with S&P TSX quarter down -1.6% and +0.7% for the year. As the table below shows, Canadian stocks have substantially underperformed the global markets so far in 2017.

[table "0" not found /]

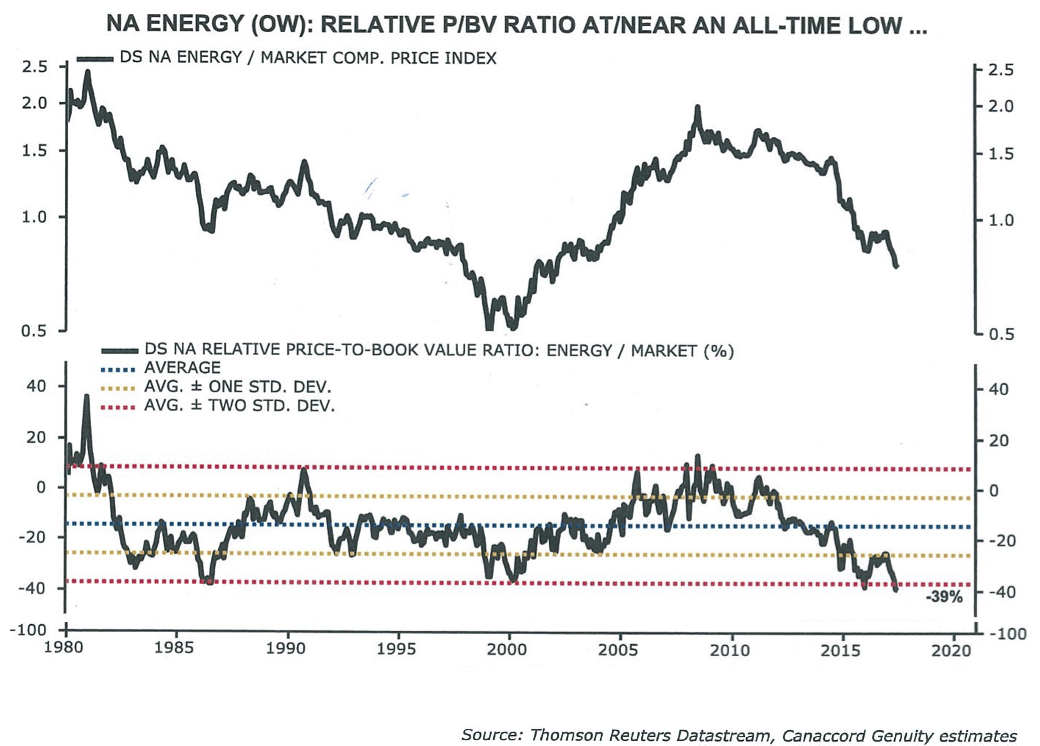

The underperformance in Canada stems largely from the commodity sectors. Last year, commodities outperformed the overall market and although we felt there would be a check back, we certainly didn’t anticipate the magnitude of it. So why the dramatic underperformance of the commodities this year? When analyzing the down draft in commodity prices, the primary underperformance lies in the oil and gas sector, with the price of oil down 14% year to date and Canadian energy stocks down over 21%. Although OPEC has been largely faithful to their production cuts and global demand has been strong, the increase in production from the US shale producers (mainly the Permian Basin) has created a supply glut with oil inventories staying stubbornly high. OPEC has voiced their intentions of running inventories back toward seasonal normal levels but oil inventories remain 280 million barrels higher than the five-year average. Although these levels are well off-peak inventory levels, the length of time required to normalize these inventories is longer than most anticipated.

The Canadian E&P sector has also been hit harder than their global energy peers as international capital flows continue to exit Canada. International investors cite a weak Canadian dollar, Trump threats against NAFTA (with the potential for a US border tax), and a general lack of capital available to the sector, as reasons for the exodus of international investors.

The portfolio is currently neutrally positioned in the Energy sector versus the S&P TSX Small Cap Index, while we wait for US production to roll over and inventories to adjust. From a valuation perspective, the E&P sector is very inexpensive on a historic basis. After the 22% decline in the first half of 2017. We anticipate increasing the portfolio weight in energy stocks in the back half of 2017 as our supply concerns abate.

The material sectors also showed a sharp correction in stock prices losing – 6.4%. That being said, the underlying commodities faired better, with copper up +1.7%, zinc up +4.2% and gold flat (-0.01%). Unlike oil, copper and zinc are experiencing a decrease in mine supply and inventories (especially zinc) are showing significant draw downs. As has been discussed on numerous occasions, the last cycle was not robust in terms of exploration. Although much capital was spent, the pipeline of large zinc and gold projects was not material. Copper discoveries, did increase mine supply over the last few years but much of that increase was needed to offset the decline of older more costly production. The bigger problem for the base metal sector over the last number of years has been demand. As we look forward to the back half of 2017, central banks are anticipated to continue unwinding extreme monetary accommodation due to improving economies. With the global recovery broadening from the US to Europe to Emerging Markets, the recovery is becoming more entrenched and commodities are poised to take off. As can be seen in the chart below, the OECD Leading indicators for emerging economies (a major consumer of base metals) and world exports are both accelerating while commodities lag.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.