Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jacqueline Ricci

January 29, 2021

OUTLOOK

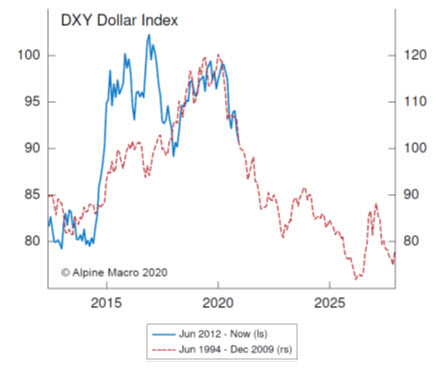

As the pandemic reeked havoc on markets in March, global governments reacted decisively and flooded markets with liquidity which led to a very robust recovery through the duration of the year. This action created a low interest rate environment and resulted in the long-awaited weakening of the US dollar measured by the DXY.

The market felt like déjà vu from the previous financial crisis (2008) and the portfolio was positioned well with a strong materials and technology weight. We continued to follow the reflation playbook and thus the portfolio has increased the base metal and energy weight through the back half of 2020.

As mentioned last quarter, we felt there needed to be a consolidation in the precious metal sector from the highs in August. This played out last quarter, with precious metals lagging the returns of most sectors. The strongest sectors for the quarter were energy (+57.5%), and consumer discretionary (+48.4), while the small cap gold sector was only up +5.1%.

Without a doubt, the fourth quarter was impacted by the global relief that vaccines were being rolled out and our lives would get back to some semblance of normalcy (probably towards the end of 2021). This collective sigh of relief propelled fourth quarter returns. The most speculative areas of the market and, companies most impacted by COVID, showed strong returns with safe havens such health care, consumer staples and precious metals underperforming.

As we look to 2021 the roadmap is somewhat murky given the tremendous performance in the fourth quarter. We have raised a little cash in the portfolio and have re-establish a slightly higher gold weight while taking profits from some of the energy, technology and base metal positions. The risk in the near term is most likely a growth scare as new strains of COVID spread quicker than anticipated or the vaccine roll out is slower than expected. If either of these two things happen, we could have the long-anticipated correction.

The US dollar has also had a significant sell off and is most likely due for a counter trend rally. This too could weigh on commodity centric stocks. Valuations of growth stocks are somewhat stretched.

The above commentary is something weighing on our minds in the short term. As we move forward through the year however, we believe the opportunity to do well in the market continues unabated. If there is a growth scare it will be met with further stimulus and further negative real rates (very positive for precious metals). Any delay in the vaccine or an increase in infections will ultimately be dealt with. The US dollar should resume its downward march setting up further upside for the commodity trade.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.