Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

November 28, 2019

We have to grudgingly give the U.S. President credit on his ability to keep sending stocks upward on continued tweets and other public releases from himself and his ‘minions’ (U.S. Trade Representative Robert Lighthizer, Treasury Secretary Steve Mnuchin and WG economic advisor Larry Kudlow in particular) about ‘how close’ they are to a ‘Phase One’ deal on trade with China. They even have the Chinese government reps on board with playing the same media game by doing releases such as China’s Ministry of Commerce online statement this week that “both sides discussed resolving core issues of common concern, reaching consensus on how to resolve related problems (and) agreed to stay in contact over remaining issues for a phase one agreement.” Stock investors continue to buy into this optimism which has sent U.S. stocks to record highs in November despite negative earnings growth and weakening global economic conditions, most of which were caused by the same President’s tariffs and the ensuing trade friction. If ever we saw a situation that could end up being a ‘buy on rumour’ (repeated many times over) and ‘sell on news’, this has to be it. Even more so since we really don’t expect that a “Phase One” deal, if it occurs, to have any ‘meat on the bone’ in terms of addressing the bigger bilateral trade issues between the U.S. and China such as intellectual rights and foreign business ownership. It probably just means more soy beans being sold out of the U.S. farm belt to China. But stock investors are in a good mood and seem willing to take whatever is offered.

Ironically enough, the economic weakness precipitated by the trade wars gave the President the leeway to berate (his chosen) Federal Reserve President, Jerome Powell, as the cause of this weakness due to the Fed’s interest rate increases in 2018, proving once again that it’s always good to have a scapegoat for whatever doesn’t go right. The subsequent 180 degree reversal in Fed policy in early January ended up being the flame that lit the fire under stocks this year. Let’s face it, with earnings growth negative this year, the entire gain in stocks has been due to an expansion of the multiple on earnings that was enabled by the new, lower interest rate policy of the U.S. Fed. Economic reality has been far less impressive than stock market returns. Fourth quarter growth in the U.S. looks set to come in around only 1.4%, and probably under 2% for the entire year. That seems a long way from the 3%, 4% and even 5% growth promised by the President but, like he says, it’s all the fault of the Fed. This week we saw the Chicago Fed’s National Activity Index (CFNAI) fall to -0.71 in October. A zero reading means the economy is growing at its longer-run trend, with positives pointing to above trend and negatives to below trend growth. Readings of -0.70 or lower have been associated with recessions! We won’t go into our entire list of recent weak economic readings but, suffice to say, the soft numbers have begun to spread from the manufacturing sector to the much larger service sector as well as the consumer confidence numbers. Thirty percent of the U.S. economy is already in recession! We expect that employment growth with be the ‘next domino to fall.’ It does make us feel comfortable with our recently-increased position in bonds in all our managed portfolios!

In terms of the stock market for the balance of this year, the consensus has clearly moved to the idea that the ‘melt-up’ will continue. Investors have positioned themselves accordingly. Portfolio managers who spent much of the summer worried about an impending recession are now afraid of losing out as the stock market heads for new record highs, according to a widely followed survey conducted by Bank of America Merrill Lynch. The investment bank’s latest monthly survey of global fund managers found that cash levels posted their largest decline since 2016 to 4.2% from 5% as investors rushed to take on risk. Cash on hand is now at its lowest level since June 2013. Of course, the marked drop in cash holdings isn’t necessarily a green light for clients who’ve held off on rejoining the stock market. Rapidly falling cash holdings are often a contrarian sell signal and history has that that a better time to invest in stocks is when the crowd is selling stocks and raising cash (think about 2008 again!). Other large sources of buying this year has been from ‘short covering’ in single stocks, ETFs, index futures and options as bearish investors were chased out of their positions to the tune of $90 billion. This combined with asset allocation and macro fund buying of over$120 billion from extremely underweighted equity investors at the start of the year. Add in close to US$800 billion in stock buybacks this year and we can see why positive money flow was the biggest source of stock market strength. Finally, the biggest change has been in the Fed’s balance sheet, which has expanded by over US$400 billion this year, nearly as big as that which occurred in the aftermath of the Financial Crisis in 2008. On top of all this, investors clearly have no worry about stocks, as reflected by the fact that the volatility index (VIX, key measure of investor complacency) has fallen back to multi-year lows. The positioning of investors is even more revealing, with short positions in the volatility at an all-time high. So much for the idea that this is the “most-hated bull market of all time.” Almost all investors are on board now, and we know that usually means we are close to the end of the move!

As the bull market enters its 11th year, it’s also interesting to look at the strategies of the largest funds in the market. In the U.S., state and local pension plans are piling on risk as they try to make up future funding shortfalls. Public plans had 47.3% of their assets in U.S. equities at the end of the third quarter, according to database Wilshire Trust Universe Comparison Service. That is more than they have had since 2007. Those risks can translate to consequences in a decline: Big hits to pension funds’ stock portfolios during the financial crisis were followed by a wave of benefit cuts for government workers hired since then. The increase in risky behavior comes from a need to try to meet future obligations in a period of record low interest rates. State and local pension plans have about $4.4 trillion in assets, according to the Federal Reserve, $4.2 trillion less than the value of promised future benefits. Many plans have also added new kinds of risk since the crisis. Alternative investments such as private equity now make up 5.6% of public plan portfolios, the most since Wilshire TUCS began collecting the data. The problem with those investments is that they have very little liquidity and the valuations are not determined in any marketplace. That means the more liquid investments have to become the source of funds in any downturn i.e. investors will “sell what they can sell.” Some plans have also shifted money out of more conservative investments such as bonds and this is being reflected in total equity allocations, including international stocks, which have risen as high as 59.4% in the past decade. Logic would seem to suggest that it would be better to have stock weightings at all-time highs because they represent good value or the outlook is strong, rather than because other alternatives are unable to achieve the necessary returns for these funds to meet their obligations!

But maybe not all investors are ‘on board’ for this more risky behaviour. The ‘ultra-rich’ investing crowd has actually gotten more cautious! A majority of ‘wealthy’ (definition unknown) investors around the world are bracing for a big sell-off next year, according to a UBS survey. Fifty-five percent of more than 3,400 high net worth investors surveyed by UBS expect a significant drop in the markets at some point in 2020. Amid intensifying geopolitical risks, the super-rich have increased their cash holding to 25% of their average assets, the survey showed. Investors see reasons to be cautious in the new year as global investors believe markets now are driven more by geopolitical events than business fundamentals such as profitability, revenue and growth potential. The ultra-wealthy’s top geopolitical concerns include the U.S.-China trade war and 2020 U.S. presidential election.

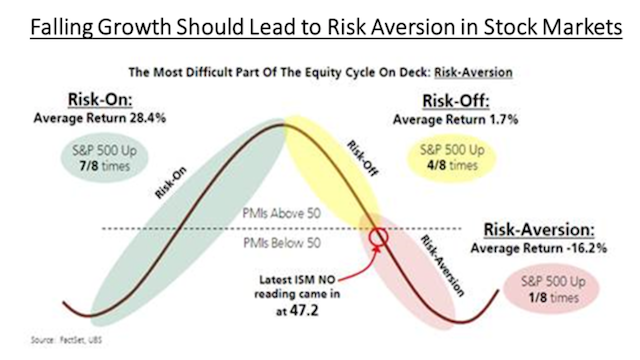

Given the weakening earnings and economic growth fundamentals, we should be entering the ‘Risk-Off’ part of the stock market cycle. In fact, the global and U.S. ISM data are currently in line with levels that have historically been associated with the ‘Risk-Aversion’ part of the cycle. Of course that was before the era of zero interest rates, which has effectively changed the behavior of financial markets as it diverted so much more money to passive investments such as stock index funds.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.