Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

March 1, 2022

Some potential good news (or opportunities) for Canadian investors is that the TSX Composite Index is trading near its cheapest level on record relative to the S&P500 Index after getting caught up in the global stock rout. That’s emerging as a catalyst for gains, especially since looming interest-rate hikes and surging commodity prices benefit the value-heavy national equity benchmark. Canadian stocks are below their five-year average valuation at about 14.4 while, after years of soaring technology stocks, the growth-heavy S&P500 Index is trading at over 20 times forward earnings. Canadian equities remain a strong relative value play within global markets, with 2022 likely positioned to see expanded reopening of the economy that should result in another year of record earnings and strongest dividend growth. With the Financial and Energy sectors being the two largest components of the composite index, it makes sense that the Canadian market should do better than its southern neighbour in this period of higher inflation, higher interest rates and a focus on lower valuation stocks with cyclical earnings exposure. That would be a sharp reversal from the past 12 years, when gains were driven by rising valuations for growth sectors.

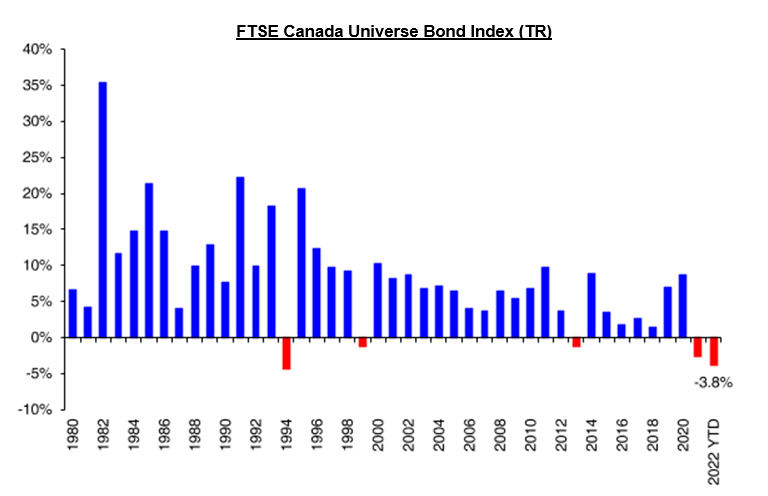

Bond Portfolio Underperformance… A New Trend? After a couple of years of massive easing, the global shift in monetary policy is lifting bond yields around the world. The upswing has been visible from Europe to Japan to the United States. In Europe, for instance, German 10-yr yields (0.22%) have not only gained 40 basis points this year, but they’re also back in positive territory for the first time since early 2019. A true ‘sea change’ looks to be taking place in the fixed income market, after a stretch of over 40 years during which bond yields were on a downward path. The ‘negative interest rate’ experiment was, in our view, an absolute failure as it did very little, if anything, to stimulate real demand. Instead all it did was to force a reallocation of savings to higher risk assets and punish income investors in the process.

As seen in the chart above, the main Canadian bond index experienced only four years of negative returns in the past forty years, but with the negative start to 2022, it could become the first period of ‘back to back negative returns’ for the bond portfolio. However we wouldn’t throw in the towel on bonds in your portfolio. The good news for bond investors is that interest rates will not move anywhere close to where they were in the past. Record global debt levels make the global financial system too levered to the rate regime, meaning that any significant rise in interest rates would most likely collapse the global economy and then unwind the rate increases. Moreove, despite the shortages driven by current supply chain issues, disinflationary forces are still stronger in the long-term, driven largely by the cost reducing impact of technology. Bonds should remain a componetn of any balanced portfolio, even though their income contribtuion has dropped to such insignificant levels. They still provide a hedge against unexpected economic shocks and will ultimately benefit from disinflationary trends.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.