Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

March 1, 2021

Maybe stock market investors are so conditioned to gains over the past year that it seems funny to even be mentioning potential pitfalls after a month when global stock averages rose another 2.5%. But there clearly was a ‘wake-up call’ in the last two weeks of February when ten-year bond yields in the U.S. surged briefly above 1.5%, causing pullbacks in many of the high growth winners of the past year of between 10-15%. While no one knows if there is a key ‘breaking point’ in terms of when stocks would succumb to rising rates like they did in 2018, but this past week shows that stocks (down ~2%) cannot absorb a surge in bond yields, especially when the growth pocket of the market is priced for perfection. Hardest hit in this brief sell-off were the leaders of the past year, those growth stocks that may not have any real earnings but lots of potential, which gets rewarded so much more when long-term interest rates are at record lows. As evidence, the red-hot exchange-traded funds from ARK Invest, which had five funds in those core growth areas which had risen over 100% in the past year, suffered a major setback. In its worst week since last March, the firm’s flagship product, the $24 billion ARK Innovation exchange-traded fund tumbled 14.6%, as some of its top holdings, including Tesla and Roku, fell sharply and investors pulled substantial money out of the funds.

An improving economic outlook is usually what is thought of as a ‘good reason’ for higher interest rates and is usually categorized as a ‘reflationary’ trade as it reflects a gradually healing of the economy, rising income and higher profit expectations. This is preferred to an ‘inflationary’ trade, wherein prices rise due to physical supply limits or rising wages, or the worst combination, which is a ‘stagflationary’ trade, where prices rise but there is no underlying economic growth. In terms of this advance, the relative strength in commodities this week reinforces that a regime shift is underway whereby rate shocks rather than growth shocks should rule market volatility over this business cycle. This makes sense given how dependent stock market valuations have become on the low-rate environment over the past decade. But, despite continued reaffirmations from central bankers (including US Fed Chief Jerome Powell this week) that rates will remain low for the foreseeable future, bond market investors aren’t fully buying into that scenario. Expectations for growth as high as 8% this year, combined with inflation moving above 2.5%, suggest that a 1.5% yield on ten-year US Treasury bonds is way below where it would historically be. Our conclusion remains that the interest rate trajectory is headed slightly higher over the next two years, but also that the growth recovery beyond 2021 may lose a fair bit of momentum as the initial ‘pent up’ consumer demand is exhausted, support programs are slowly withdrawn and governments begin to deal with the record debt levels that have been created to get through this pandemic. While many pundits have labelled this recovery a potential ‘roaring twenties’, very similar to what occurred a century ago, we believe it will look a bit more like recovery after the Second World War. Then there was an industrial revolution not unlike the technology revolution of today as well as a rebuilding effort not unlike the planned infrastructure spending projects we currently see being planned. Bottom line, it could turn out to be a good long-term period for stocks, but investors need to be wary of short-term bouts of ‘over excitement’ that need to be corrected. Despite those shorter-term risks, we are wary about getting too defensive in our managed portfolios since, in many ways, the market sits in something of a sweet spot, benefiting from the stupendous profitability reported by beneficiaries of the homebound/on-demand economy in big tech and e-commerce, while also drawing energy from the fast Covid-case-rate collapse and vaccine rollout. Consumers are also sitting on almost $2 trillion in accrued household savings, hastened by a lack of travel and leisure spending, with another fiscal package on the way.

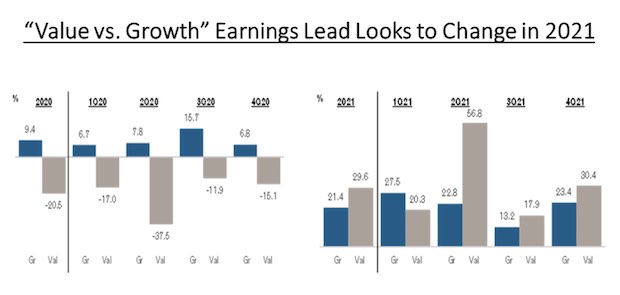

While the technology, defensive, interest sensitive and ‘stay at home’ stocks have lead over the past year, we are starting to see a shift in this performance in the past few months that we should also start to see in the earnings performance of these sectors as the economy recovers and interest rates start to climb. In our Hedge Fund, we continue our recent ‘market neutral’ strategy of maintaining short positions in key growth indices such as the Nasdaq100 (equal weighted) and the Russell2000 Growth ETF against long positions in cyclical stock sectors such as energy, industrials, basic materials and financials. These ‘value’ sectors of the market are expected to show earnings growth of almost 30% in 2021, after falling over 20% last year. While growth sector earnings are expected to remain strong (at over 21%), this is less of a reversal from 9% growth in 2020 and is already reflected in the excessive valuations in growth stocks.

We don’t get proper long bull markets in industrial commodities very often: over the past 227 years, says Saxo Bank, there have only been six. But when you do, they are all driven by the same easy-to-see-in-hindsight dynamics; a glut of supply drives down prices. Producers then stop exploring and innovating. Supply falls behind demand. Stockpiles run down and prices rise. The key thing for investors to note is that once events are under way the price rises tend to go on for some time, due to the fact that it takes well over five years to get a new mine up and running. So where are we in the cycle now? The big metal miners effectively went on investment strike in 2014, stopping almost all expansionary spending with the result that a large number of industrial metals were already in short supply even as we went into the pandemic last year. That shortage of supply is soon to hit a new wave of demand as the growth of 5G, communications, battery technologies and electric vehicles will lead to resurgent demand for base metals such as copper and nickel as well as specialty minerals such as cobalt. The result can be seen in the chart below of the movement in copper prices over the past year, soaring by over 60% to their highest level since 2011.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.