Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

March 1, 2023

Given the increased central bank rhetoric about keeping interest rates ‘higher for longer’, the sharp rally in stocks and bonds in January did seem somewhat overdone and reflecting too optimistic an outlook and was perhaps just a ‘counter-trend bounce’ following the substantial weakness in markets in 2022. That scenario became the case in February as stocks gave back much of their January gains while bonds gave back all of those gains. With central banks determined to eradicate inflation, the continued strong economic data so far this year just meant that interest rates will have to rise even higher than expected and stay at those levels longer. That is not good news for stocks! Inflation data show that consumer price growth reaccelerated in January, marking the latest sign that the U.S. economy is defying the Federal Reserve’s attempts to cool demand. This data, along with an employment report that crushed even the most bullish expectations, sent stocks tumbling and sparked calls for a hefty half-point interest-rate hike when the Fed meets again next month. The latest inflation report also fueled further questions about why the economy has been able to remain so hot nearly a year into the central bank’s most aggressive monetary-policy tightening campaign in decades, defying widespread expectations. One key observation about this correction is that there has been no place to hide. Higher yields have penalized growth sectors such as technology as well as high-yielding defensive stocks, while the higher U.S. dollar, lower commodity prices and worries about slowing growth have hurt resource stocks, consumer cyclicals, financials and industrials.

The question of how the economy, despite the substantial financial leverage and the exceptionally sharp increase in interest rates, has been able to defy gravity and stave off recession has given rise to a volatile economic environment, one in which a single data release can send markets soaring one day and plunging the next. The dynamic has forced economists to examine why the combination of geopolitical tensions, inflationary pressures, and tightening monetary policy is having far less of an impact on the economy than historical precedent and conventional wisdom would suggest. The simple answer is that it’s impossible to apply old rules to a new economy, one that has been completely—and permanently—transformed by the Covid-19 pandemic and no longer responds in the same way to rising prices and tighter monetary policy. The long tails of fiscal stimulus, for example, have propped up the economy for far longer than anyone expected. Excess consumer savings and an ebullient labor market fueled demand for travel, restaurant dining, and other services, where spending still has room to grow. Most importantly, though, is that years of low interest rates have transformed the debt dynamics for the overwhelming majority of households, leaving them largely shielded, through fixed-rate mortgages, from the impacts of the central bank’s primary tightening tool. The result is an economy that has yet to fully react to the policy tools designed to slow inflation, which more often than not have forced a recession.

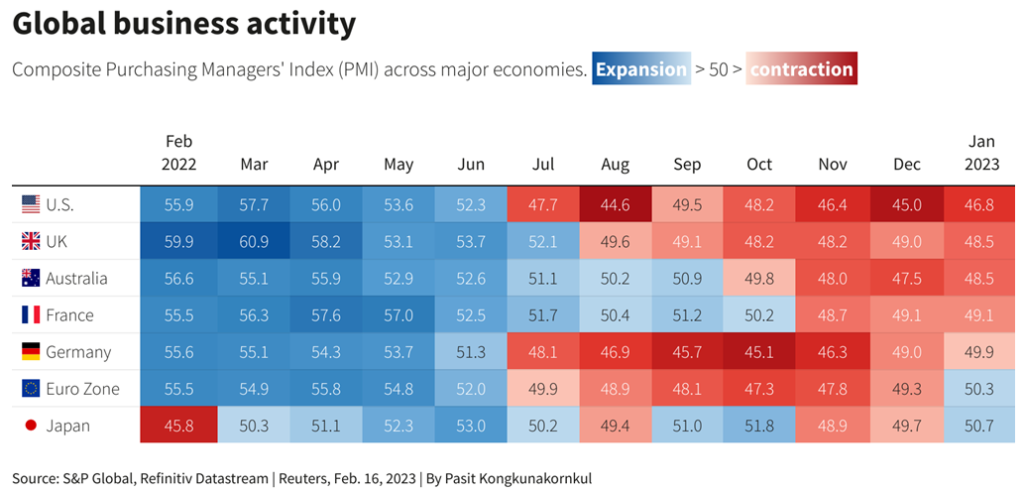

Despite the changes brought about by the pandemic, we think it is pre-mature to ‘toss out the old rulebook’ on the relation between interest rates and economic growth. The lags will just be longer. This is still a very ‘highly levered‘ financial system and there is no way that the sharp rise in rates will not ultimately impact economic activity. The recent spate of positive economic data has fueled hopes of a “no landing” scenario, in which the economy continues to expand, rather than a hard or soft landing. But a more realistic outlook is less benign: Interest rates are likely to stay higher for longer to tamp down stubborn price growth, probably forcing at least a mild downturn along the way. We believe that we are already starting to see some ‘cracks in the armour’ of the bullish economic scenario. The chart below highlights this outlook in a simplistic way; the global ISM readings below 50 (i.e. economic contraction) are in red while the ISM readings above 50 (expansion) are in blue. The trend in the shading of the chart clearly indicates that most global economies began slipping into a slowdown mode in the second half of 2022 as the impact of rising interest rates works their way through.

One area where we are starting to see an impending slowdown is from the ‘big box retailers’, who remain a key litmus test for the overall economy. While Home Depot, Walmart and Target all reported strong Christmas period sales over the past week, their outlooks for 2023 were more muted as they face a shift in both sales trends and market sentiment. Inventory troubles, squeezed profit margins and concerns about inflation-pinched, middle-income consumers caused there major players to miss Wall Street’s earnings expectations for the balance of the year and warned investors to expect softer sales. The stocks did take this news in stride however, since investors seemed prepared for something more dire than those slowdown warnings.

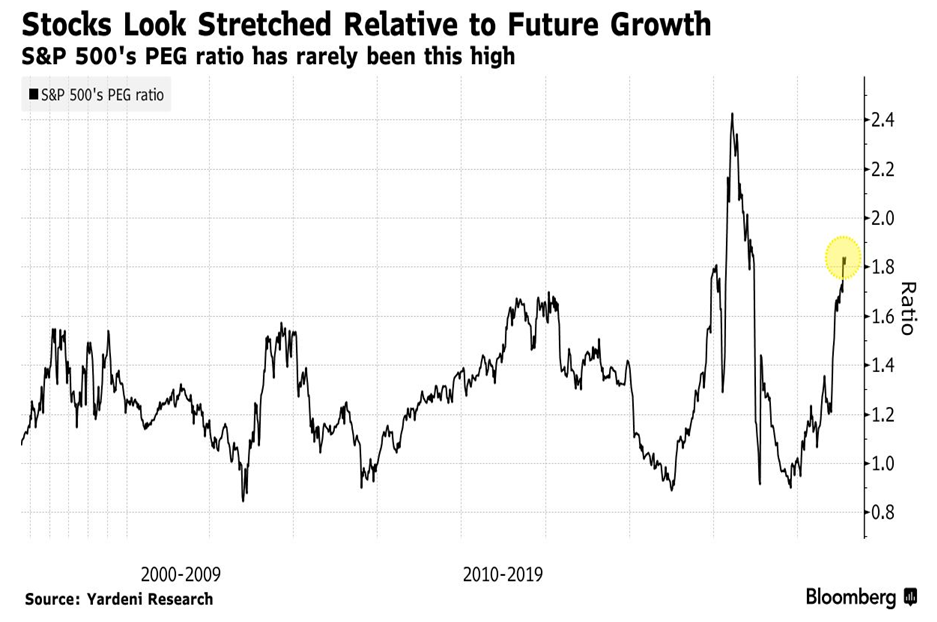

While the re-emergence of hotter-than-forecast inflation was the proximate cause of the latest pullback in stocks, another force is also at play in the longest series of weekly declines since last May, namely high valuations. One measure of the increasingly anemic growth expected in S&P 500 earnings shows equities as richly priced as they’ve been in almost three decades of data. The PEG ratio is the market’s price-earnings multiple A higher PEG means more expensive stocks. divided by its forecast growth rate. At about 1.8 times based on longer-term estimates, the indicator’s message is ominous particularly since we believe that many earnings estimates are still too optimistic given our outlook of slowing economic growth later this year. Stretched multiples at a time of stiffening Federal Reserve resolve to whip inflation now is a cocktail that investors have wanted no part of in February.

In terms of our investment strategy, we remain cautious. After January’s rally we became even more defensive and moved to a full underweight position in stocks (around 40% in balanced funds, right at the low end of our traditional 40-65% range). We reduced technology stock exposure as we wanted to see how the economic slowdown impacted some key growth areas of the past few years, particularly cloud services, phone sales and mobile advertising. We did maintain an overweight in semi-conductors, though, as they have already adjusted to lower estimates and still need to rebuild productive capacity given the ongoing chip shortage in key sectors. Earnings reports from Nvidia and AMD seemed to support this view. We also reduced exposure to economically sensitive sectors such as consumers (autos, retails and housing), industrial production (steel, base metals and rails) and remain underweight financials. Gold stocks continue to look like a good contrarian play this year as we expect more U.S. dollar weakness, decades-low valuations and a reversal of the tight interest rate environment later this year. We also continue to like the pipeline and telecom companies for their high dividend yields, stable earnings and moderate valuations. Top names in those sectors remain Rogers, BCE, Telus, Enbridge, Pembina and TC Energy. We also continue to like the energy sector, particularly the Canadian oil stocks. With China opening up again and the U.S. done selling from their SOR (Strategic Oil Reserve) we expect oil prices to remain at least in the US$75-80 range and potentially move higher. The oil stocks are trading at less than four times operating cash flow and generating substantial free cash flows, most of which they are returning to shareholders via stock buybacks and dividend increases after debts were reduced to below one times operating cash flow.

While the reduction in stock exposure, in retrospect, worked out to be a good call for February, we cannot make the same claim for our increase in bond exposure. Bonds gave back all of their January gains as stronger economic numbers and stubbornly high inflation pushed long-term interest rates back up to the high end of their recent range. Going forward though we did add further from our cash reserves into bonds on this pullback, as we still expect central banks will succeed in bringing down inflation, but will do so by driving the economy into at least a mild recession. The timeline for this pullback has clearly been stretched out as the economy has proven to have tremendous momentum still from strong employment and ‘pent up’ post-pandemic demand for services. But we believe that a more severe slowdown has only been delayed, rather than avoided. This means that earnings and stock prices remain at risk and we continue to manage stock exposure accordingly, maintaining an underweight position in stocks and a bias towards lower valuation stocks with more ‘recession resistant’ earnings. Elsewhere, we continue to have larger than normal cash balances in all accounts (especially since cash returns have risen so sharply in the past year) and have taken bonds to a slight overweight position, with a focus on government mid-term debt.

While we see many impediments still ahead for stock investors, there are some factors that we believe would limit the downside in stocks to the lows seen in June and October last year. First and foremost, the sentiment toward stocks has become much more pessimistic as traders have built short bets in both U.S. and European equity futures, according to Citigroup Inc. strategists. In a “markedly more bearish” swing last week, traders added nearly $3 billion of new shorts to S&P500 futures positioning and pulled a net $5.1 billion from exchange-traded funds. Markets do tend to find their lows when negative sentiment moves to extreme levels. We seem to be close to that point, something that might limit the downside on stocks despite a hawkish interest rate forecast and softening economic growth. While stocks always rally prior to the start of a new economic cycle, they never bottom before the recession has even begun. In that regard, we deem it still too early to be adding to stock market exposure.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.