Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

November 2, 2020

The expression “picking up pennies in front of a steam roller” was coined by journalist Martin Wolf and economist John Kay to describe investments which normally provide a payoff of small positive returns, while carrying a small but significant risk of catastrophic losses. We see that as an apt description of investing in bonds in most portfolios today. The bond market has done exceptionally well in the past decade, and for much of the past forty years, as central banks have eased policies and pushed interest rates down to record lows, and even into negative values in parts of Europe and Asia. The tailwinds for bonds has even accelerated in the past few years as ‘quantitative easing’ policies took monetary options beyond just low interest rates by turning central banks into buyers of last resort of massive quantities of corporate bonds and mortgages to suppress their yields as the government prepares to ramp up its debt issuance to fund the deficit. Foreign buying of U.S. bonds has brought in additional buying as the spread between U.S. and German 10-year government yields has grown to multi-month highs. At a time when currency hedges are inexpensive and the dollar weak, this drew overseas buyers to U.S. Treasury Bonds to capture richer yields. But despite all these tailwinds, bonds failed to rally as stocks sold off in late October. Investors, in our view, are starting to look through the short-term economic risks and begin to price in better economic conditions in 2021 and perhaps some upward pressure on previously dormant inflationary pressures. This would mean a further move higher in bond yields so those still looking to ‘pick up pennies’ might be advised to start moving a bit more quickly! Other traditional ‘reflationary’ measures have already turned positive. As shown in the chart below, the ratio of copper prices to gold prices as well as the ratio of financial stocks to utility stocks have both turned higher recently and we believe this sets the stage for higher bond yields.

Consensus is often difficult to find in the investment industry but one view that seems to shared by almost every commentator is that inflation will remain low for the foreseeable future, thus allowing interest rates to stay at record low levels. We find this somewhat surprising given that we have never seen the type of global monetary expansion as we have in the past year. We have many real-world examples, including South America in the 1970’s and some African nations in the 1990’s to see what can happen to inflation and currency values after a period of aggressive money expansion. In those countries the values of paper currencies plummeted and inflation rates surged to above 1000%! For that reason alone, we continue to hold a weight in precious metals as a hedge against all of this monetary stimulus and the ensuing risk to paper currencies.

As mentioned earlier though, we expect to see better economic conditions over the next year as stimulus measures are re-introduced and the probability of a Covid19 vaccine increased. Despite soft consumer numbers in the past month as the stimulus programs wound down, business confidence has turned relatively position. The Conference Board Measure of CEO Confidence™ rose sharply in the final month of the third quarter, after a moderate increase in prior months. The measure stands at 64, up from 45, as capital spending plans improved, with 25% of CEOs anticipating increased spending over the next 12 months, up from only 15% earlier in the quarter. Moreover, 36% foresaw upward revisions in capital spending beyond the next 12 months. CEOs entered Q4 significantly more upbeat than they were earlier this year. Notably, talent shortages eased in the wake of COVID-19 and nearly two-thirds of business leaders said they anticipated little, if any, problems with attracting qualified workers. Nonetheless, uncertainty around the pandemic remains a risk to newfound optimism as we enter 2021. All this is encouraging as far as it goes, implying investors are gaining comfort with a solid growth trajectory into 2021, perhaps boosted by another fiscal infusion, without new Covid-related restrictions undercutting the recovery.

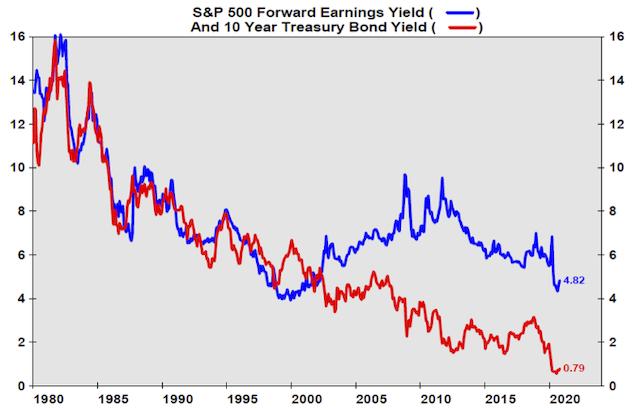

In the end it’s really two key factors that move stocks; interest rates and earnings! Interest rates really drive the ‘P’ in the traditional P-E (price to earnings) ratio. The sharp drop in rates over the past decade has driven valuations close to record levels and we see little further expansion from that source. In fact, we see it more likely that interest rates start to move higher over the next year, pushing valuations lower. The better news is that the ‘E’ component, earnings, are in the early stages of the sharpest recovery we have seen since the recovery from the financial crisis in 2009 (excluding the brief, but temporary, positive impact of the ‘Trump tax cuts’ in 2018). This should support a higher move in stocks. At the very least, it should lead to stronger performance in stocks versus bonds. The chart below shows how the ‘earnings yield’ of stocks (i.e. the inverse of the P-E ratio) has moved in tandem with government bond yields. The blue line above the red line indicates periods when stocks were under-valued relative to government bonds. Clearly we have been in such an environment for a number of years, but that has been during a period of falling interest rates. If we are correct and interest rates begin to rise, we expect that stocks would do much better than bonds and the earnings yield could move in line with bonds. The last time that happened was in the late 1990s during the technology bubble. This time, however, earnings are expected to recover more sharply in areas other than technology. That could lead to more broadly-based stocks gains.

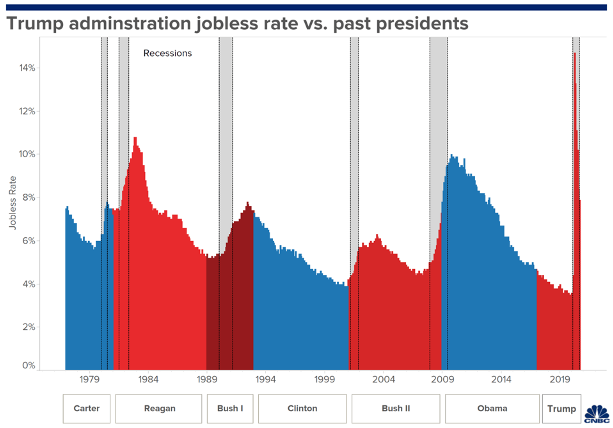

We don’t like to delve into politics in our market comments, but it is hard to avoid given the potential market impact of a change in the occupant of the White House or a disputed outcome that keeps stocks in a period of confusion, much like we saw in the 200 election. In that case we saw a sell-off in the S&P500 over almost 12% before final results were declared over a month later. Today, the president is trailing his challenger, Joe Biden, in national polls and in most battleground states. Polling on the issues shows Mr. Trump losing on nearly every issue except handling the economy, where the two men are essentially in a dead heat. The pre-Covid economy was in fine shape and Trump was claiming credit. But was the strong economy of February 2020 a result of his policies? The nearby chart shows the downward path of the national unemployment rate from the time unemployment started to decline after the Great Recession (November 2010) to right before the Covid-19 catastrophe slammed the economy (February 2020). Unemployment did trail down, from over 9% to a wonderfully low 3.5% rate. The macroeconomy was in excellent shape before the pandemic hit. But we can’t see any discernible change in the trend when Trump replaced Barack Obama or when the tax cuts took effect in 2018. In the end, central banks and the path of the global economy probably have had a far bigger impact on the economic results than any political changes or policies. But don’t try telling the politicians that their impact isn’t as important in the grand scheme of things. Most of us will just be happy to be able to talk about something other than U.S. politics and the impact on stocks!

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.