Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

October 1, 2021

The ‘summer doldrums’ in the stock market continued into September with most stocks struggling but the large technology stocks keeping the overall averages from falling sharply. However, markets in both the U.S. and Canada did experience some mid-month weakness that pushed the major indices down 5% from their peaks, before recovering slightly. The fall in stocks was not caused as much though by typical trepidation about either an economic slowdown or the long-awaited end of massive bond buying support (quantitative easing) from central banks. The worries this time were about corporate earnings, which have been the backbone of the stock market’s strength over the past year The upcoming third quarter earnings reporting season is taking on more importance after some major industrial and consumer companies (i.e. PPG, Fedex, Sherwin Williams, Starbucks, Nike) all pointed to the negative impact of rising material and labour costs on their profit margins. Second quarter earnings had been a blowout to the upside, surpassing expectations and putting 2021 earnings growth on a 40% plus rate! Third quarter could end up being a disappointment relative to expectations and stocks are likely to react poorly, as FedEx showed last week. The company reported its fiscal first-quarter numbers, which missed earnings projections and they then cut full-year profit guidance, causing the stock to drop sharply. For FedEx, labour was the big issue in the report as “first quarter operating results were negatively affected by an estimated $450 million year over year increase in costs due to a constrained labour market.” This is an early quantification of the kinds of problems that investors will be hearing about when third-quarter earnings start getting reported in October. Companies are paying more for less and that is becoming a problem for stocks going into the fourth quarter as bottlenecks continue and costs rise. The upshot is an implied margin squeeze, the likes of which we haven’t seen since the 1970s when U.S. President Nixon severed the dollar’s link to gold and imposed 90-day wage and price controls. Those weren’t good times for corporate profits! Despite the margin squeeze, analysts remain sanguine on the profit outlook. FactSet expects third-quarter earnings to be 28% above the depressed results in the comparable 2020 period. Looking ahead to 2022, when comparisons won’t be nearly as easy, the consensus sees a sturdy 9.3% rise.

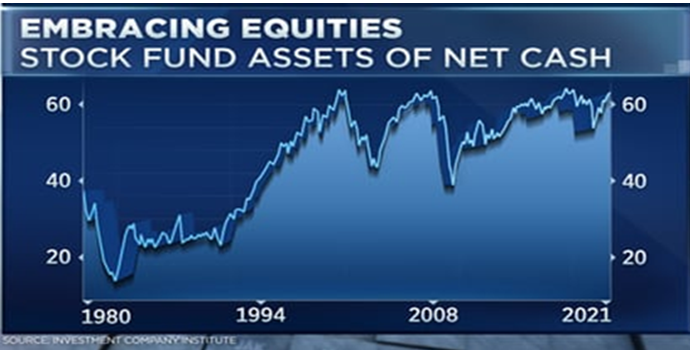

While making short-term predictions about stock market movements is rarely a successful endeavour, what worries us in the short term is that investors have become accustomed to massive earnings beats in the past four quarters, and we don’t see the same level of outperformance ahead. Meanwhile, investors are already ‘all in’ on equities, as shown in the chart below. Stock fund assets in the U.S. are once again over 60%, much like they were in 2000 and 2008! Expectations need to come down, which would cause stock prices to correct. At the very least, we don’t see any catalysts for any sharp upward moves. For those reasons, we have raised cash levels slightly going into quarter end and moving to a more defensive position with stock holdings, focussing on those with high dividend yields, low valuations and stable earnings.

Investors in major survey have gotten bearish on the economy but remain bullish on stocks. Barely 10% of respondents in a monthly fund manager survey expect a stronger global economy in the coming months, marking the lowest proportion since last April’s initial COVID-19 panic, Bank of America’s September edition of the survey showed. Economic growth expectations are now at a net 13%, the lowest since April 2020 and markedly down from a 91% peak in March this year. The spread of the Delta variant was cited as the reason for the pessimism, the popular monthly survey said. Despite the growing caution on the macroeconomic outlook, positioning in asset markets remains overwhelmingly bullish. Equity market protection designed to shield portfolios against a sharp drop in asset values was at the lowest levels since January 2008. Nearly half of BofA’s clients, with $840-billion in assets under management, said they have removed protection against a sharp fall in equity prices over the next three months, the lowest figure since January 2018. Moreover, broader equity market positioning remains firmly bullish with net global equity allocations at 50%, far above a 20-year average of 29%. Bottom line, the survey called it “a rare disconnect between asset prices and fundamentals.

Another worry for stocks, not that they needed any more, is coming from China. The headlines have all been about the Evergrande real estate crisis, with the company potentially defaulting on over $300 billion in liabilities and interest payments coming due. Its stock price had collapsed to near zero while its bonds were quoted at around about one-quarter of their par value, clear indications of the market’s awareness of the storm gathering around the heavily indebted real estate outfit. But what happens to Evergrande in China is apt to stay mostly in China. This is not going to be another ‘Lehman moment’, referencing the bankrupcy that cascaded into the Financial Crisis in 2008. The government doesn’t want to be seen as engineering a bail out, but is likely to organize a debt restructuring to reduce systemic risk and contain economic disruption. The bigger issue in China (as well as parts of Europe) is a power crunch that has shut down factories and left some households without electricity under an effort to meet official energy use targets. That could have global repercussions, including on supplies needed for manufacturing throughout Asia, ahead of the year-end shopping season. That’s on top of parts and raw material shortages that already ail regional manufacturing because of supply disruptions caused by the coronavirus pandemic.

In many ways, this is turning into an economic cycle unlike anything we have ever seen. While the early recovery from the pandemic and the coincidental anomoly that the last pandemic occurred one hundred years earlier lead many investors to predict another “roaring twenties”, the surge in inflation, rising oil prices and the recent pullout of U.S. troops from a 20-year war halfway around the world likened the current situation to the 1970s! The 2020s, in our view, is shaping up as a whole new scenario. Record doses of monetary stimulus rescued financial markets while massive fiscal support engineered a sharp rebound in consumer spending to help the global economy recovery from the pandemic. But the interwoven supply chains that the global economy had spent the last three decades building were severely damaged by uneven shutdowns in countries across the globe. While demand and revenue continue to be strong as the global economy recovers from the pandemic, the acute labour shortage and supply chain disruptions from semi-conductors and other materials are forcing companies to either cut back production or else absorb much higher costs. Bottlenecks in any part of that chain lead to production problems that have only started to emerge. Recent estimates show the auto industry worldwide could lose $210 billion in revenue this year due to chip shortages and other supply bottlenecks. That’s twice the amount of losses estimated a few months ago. Because of the disruptions, carmakers will lose production this year of 7.7 million vehicles.

Despite all the worries mentioned above, we don’t see economic risks as being longer-term risks for stocks. The supply bottlenecks will get sorted out. Even if the recovery stays more anemic in the short term, the demand for goods and services is still there and will continue to be supported by fiscal and monetary policies. More importantly though, the employment situation continues to improve such that wage grwoth and falling unemployment rates will sustain consumer spending. The U.S. economy is actually in the unusual situation of having more job openings right now than unemployed workers, a rare occurrence. While this has lead to rising costs for restaurants and other service businesses that need to fill these positions, it’s hard to see that this is a negative development for the economy as a whole. Clearly a sharp reversal from eighteen months ago when unemployment surged to an 80-year high.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.