Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

February 11, 2023

In January, the preferred share market had strong performance, taking its cue from common equity markets. With year-end tax-loss selling in the rearview mirror, it appeared that retail investors were driving the market higher as trading volumes to start the year were below average. The rebound from the oversold condition at the end of last year reversed the combined loss of the previous three months and returned the index to a level not seen since last September. The S&P/TSX Preferred Share index ended the month with a return of 7.27%.

Canadian economic data released in January continued to show strength in the economy. Employment in December increased substantially by 104,000 new jobs and the previous month’s jobs number was revised higher by 26,700. The strong job creation helped push the unemployment rate down to 5.0%, just above the all-time low level of 4.9%. The November year-over-year increase in GDP was 2.8% which was a small decline from the previous level, nevertheless a solid level of growth. Retail sales reported for the month of November declined but were better than expected. December’s year-over-year inflation rate declined by 0.5% from the previous month to 6.3%, which still left inflation at a historically elevated level.

There was no new issuance of traditional $25.00 par preferred shares during the month, however Bank of Montreal took the market somewhat by surprise by issuing its second institutional preferred share. It was unexpected because the bank appeared to have capacity to issue more tax effective Limited Recourse Capital Notes, and many investors thought that a couple of other banks were more likely to be the next institutional preferred share issuer. The Bank of Montreal issue seemed to have been the result of interest expressed by a large institutional investor, which resulted in small allocations for many other investors, despite strong investor demand. Bank of Montreal raised $650 million with a dividend rate of 7.057% and a reset spread of 425 basis points. The issue performed well after issuance and had little impact on either the traditional $25.00 par preferred share market or other institutional preferreds.

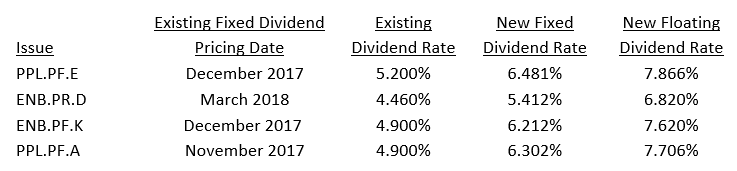

In January, both issuers elected to extend rather than redeem their resetting issues. Given that the yield of the 5-year Canada bond continues to be substantially higher than five years ago, each of the resetting issues raised their dividend rates substantially in January. In addition, as each issue was trading at a discount to par, the resultant increases in yields were even larger than the changes in the dividend rates. Details of the resetting issues were as follows:

In issuer news, Manulife Financial Corporation announced that it will not be redeeming its MFC.PR.J shares. The new dividend rate will be announced on February 21st. Also in January, CIBC stated that an insufficient number of holders of CM.PR.S (which it extended in December) wanted to make the switch into the floating rate series, therefore all shares will have a fixed dividend rate of 5.878% for the next five years. In addition, the previously announced redemption of the Northland Power Inc $120 million NPI.PR.C series took place in early January.

The quarterly S&P/TSX Preferred Share index rebalancing occurred during the month, with four additions (all perpetual issues) and five deletions (four rate reset issues and one perpetual issue).

The seven largest preferred share ETFs experienced net outflows of $20 million in January. However, the experience of each fund varied, with the passive ETFs having outflows while the actively managed ETFs had net inflows. In other ETF news, Invesco announced that it will close its Canadian Preferred Share Index ETF, PPS, in April. The ETF had AUM of $49 million on December 31st.

J. Zechner Associates Preferred Share Pooled Fund

The fund returned 6.74% in January, which was lower than the S&P/TSX Preferred Share index return. Perpetual issues were the best performing sector with a return almost double that of rate reset issues. Fund performance was hurt by the portfolio’s slight underweight allocation to perpetual issues and its cash holdings. In addition, the institutional preferred share holdings that had fared much better than $25 par preferred shares in the selloff in late 2022 did not experience the same rebound from oversold valuations.

During the month, despite the move higher in prices, we continued to add to existing positions in several perpetual issues that had yields greater than 6.00%, which we believe provides good long term value. We also sold the remaining small position in RY.PR.N. Other transactions included adding to the existing Bank of Montreal 7.373% institutional preferred share position. Also, we finished the switch from MFC.PR.Q, which resets in May, into MFC.PR.I, which recently reset its dividend rate. At current 5-year Canada bond yields and share price levels, the MFC.PR.Q shares would reset at approximately the same yield as MFC.PR.I. However, given the uncertain path of interest rates over the next few months, we chose the certainty of the 6.40% yield on MFC.PR.I until September 2027.

Outlook and Strategy

As noted above, the yield on the 5-year Canada bond continues to be substantially higher than five years ago resulting in significant increases in dividend rates for resetting issues. In January, as expected, the Bank of Canada raised its overnight rate by 25 basis points, however signaled that it was likely to pause additional rate hikes while it waits to see the full impact on the economy of the monetary tightening initiated in March 2022. A pause in rate hikes indicates that the Bank is anticipating that this level of monetary tightness is sufficiently restrictive to slow the economy and return inflation to the official target of 2%, despite the relatively marginal decline in inflation so far.

A major concern for Canadian investors is whether the Bank of Canada will have the fortitude to hold current monetary policy levels until inflation returns to their target level of 2%. Currently, the market is expecting the Bank of Canada to pivot and begin lowering interest rates when the economy slows later this year. However, we believe the Bank of Canada is unlikely to ease monetary policy and lower interest rates until inflation has subsided for several months to avoid a resurgence that would require even higher interest rates.

The Canadian economy continues to grow, and unemployment remains low. Currently, the only sector showing real weakness is housing, with data released in January showing annual home sales down 39% country wide, the steepest decline since 2009. While inflation has declined from its peak, it remains historically high and far above the 2% target level. The key question is how quickly inflation slows. We believe that returning inflation to the desired levels will take longer than the market is currently assuming. Inflation has too far to decline in a relatively short period for the Bank of Canada to begin lowering rates in 2023. Therefore, we believe rate reset issues, particularly those with reset dates in the next few months, will continue to benefit from sharply higher dividend rates when they reset. Preferred shares continue to look attractive versus alternative fixed income instruments, particularly on an after-tax basis.

Whether Canada experiences an economic slowdown or an actual recession, we remain confident in the creditworthiness of the issuers in the portfolio, as these companies have successfully weathered previous economic downturns without impacting their ability to pay the dividends on their preferred shares.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.