Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

February 15, 2024

In January, the preferred share market moved sharply higher, with performance significantly better than both bond and equity markets. From the first trading day to the end of the month, investors seemed to be attracted to the yields available in preferred shares. A large index rebalancing at mid-month reinforced attention on the asset class and provided additional impetus to the market. Also, the redemption late in the month of $300,000,000 BNS.PR.I shares generated reinvestment related buying. During the month, all issue types had strong positive returns, with rate reset issues experiencing the largest gains. The S&P/TSX Preferred Share index ended the month with a gain of 5.81%.

In Canada, the economic data released during the month suggested the Bank of Canada would take longer to cut interest rates than the market had anticipated. The unemployment rate held steady at 5.8% despite job creation stalling, as the participation rate fell somewhat. Of concern to the Bank of Canada, though, wage pressures increased with average hourly wages rising by an eye-popping 5.7%. In addition, overall inflation accelerated with CPI rising to 3.4% from 3.1%, while core measures of inflation remained stubbornly above 3.5%.

The Bank of Canada announced on January 24th that it was leaving its overnight target interest rate unchanged at 5.00%. While Canadian economic growth had stalled, in the Bank’s opinion, the central bank wanted to see “further and sustained easing in core inflation”. The Bank’s projections expected inflation to remain around 3% in the first half of this year, then start gradually declining and finally return to the 2% target in 2025. After the Bank’s announcement, StatsCan estimated Canadian real GDP topped expectations with a respectable 0.2% advance in November, and the flash estimate for December pointed to an even sturdier 0.3% rise. If the flash estimate is correct, growth in the fourth quarter would have been at an annual pace of 1.2%. While not robust, that pace is considerably better than the lack of growth experienced in the middle quarters of 2023 and substantially better than the Bank of Canada’s projections. Better than expected growth, of course, reduces the pressure on the Bank of Canada to lower interest rates. In addition, the Bank made no changes to its Quantitative Tightening (QT) programme, which is gradually reducing the Bank’s holdings of Government of Canada bonds accumulated during the pandemic.

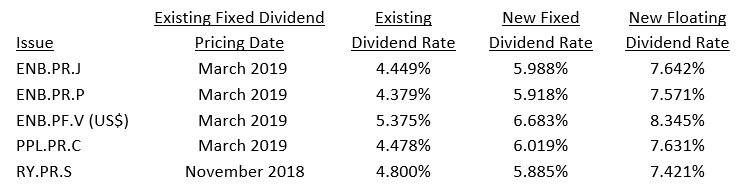

There was no new issuance of traditional $25.00 par preferred shares during the month, however Royal Bank of Canada issued its second institutional preferred share. It raised $750 million with a dividend rate of 7.408% and a reset spread of 390 basis points. Given that the issue had the highest dividend rate of an institutional preferred share and a high reset spread, there was strong investor demand and it performed well after issuance. The issue came a day after the bank announced that it would not be redeeming the RY.PR.S series in February. Those shares have a reset spread of 238 bps, and the extension continued a recent trend in which most bank rate reset issues with similar reset spreads have not been redeemed. In addition, Royal Bank’s decision to not redeem the RY.PR.S shares likely reflected its need to maintain strong capital ratios as it seeks to close its acquisition of HSBC Bank Canada.

During the month, five series of preferred shares reset their dividends. Dividend rates continued to reset significantly higher because the 5-year Canada bond yield continued to be substantially higher than five years ago. Details of the resetting issues were as follows:

Royal Bank investors must make their decision whether to into the floating rate series by February 9th, while Enbridge and Pembina Pipeline investors have until February 15th to make their choice. Despite floating rate yields remaining substantially higher than fixed rate ones and interest rates potentially staying higher for longer, preferred share investors continue to appear concerned that interest rates will fall in the next year and take floating rate dividends below fixed rate levels.

The quarterly index rebalancing features eleven deletions and seven additions. Ten of the deletions were the result of S&P downgrading Brookfield Office Properties from P-3 to P-4, making the shares ineligible for the index. In total, 115 million shares of Brookfield Office Properties and Brookfield Properties, with original par value of $2.875 billion, were removed from the index. As a result of the large number of issues in the rebalance, trading volumes were robust that day, with more than three times average trading volumes, and the market moved higher. The market continued to move higher through the end of the month as some new money seemed to come into the market.

Prior to their deletion from the index, Brookfield Office Properties announced a normal course issuer bid (NCIB) to purchase up to 10% of the public float of its each series of outstanding preferred shares. The announcement resulted in the shares rallying strongly, recovering the losses that occurred following the S&P downgrade announcement in December. The NCIB will run from January 12, 2024, to January 11, 2025.

In aggregate the seven largest preferred share ETFs had an outflow of $56 million in December. Given the strong market performance during the month, the outflow was surprising.

J. Zechner Associates Preferred Share Pooled Fund

The fund had a return of 4.17% in January, which significantly underperformed the S&P/TSX Preferred Share index. The fund’s underperformance was largely a function of security selection, particularly in two areas. Firstly, fund performance was hurt by its approximate 16% allocation to bank institutional preferred shares and LRCNs that are not in the S&P/TSX Preferred Share index. These securities had enjoyed strong relative performance in 2023, and consequently did not enjoy the rebound that other preferred shares experienced in January. Secondly, we had deliberately avoided Brookfield Office Properties’ preferred shares. While the issuer’s preferred shares were removed from the index on the 19th of the month, their performance prior to their removal was very strong with several gaining more than 10% since the start of the year. As a result, they were significant contributors to the index’s gains.

Portfolio activity during the month included starting to switch MFC.PR.Q into MFC.PR.K for a pickup of approximately 40 basis points. We sold the position in CU.PR.C, which had appreciated in price, and bought IFC.PRG which yields approximately 40 basis points more. In addition, we sold the position in RY.PR.S and participated in the new Royal Bank institutional preferred share issue.

Outlook and Strategy

Notwithstanding robust performance over the last three months, we are positive on preferred shares because they continue to offer investment grade quality with significantly better yields than corporate bonds, making them an attractive fixed income alternative. The 5-year bond yield continues to be substantially higher than five years ago resulting in substantial increases in dividend rates on resetting issues, which is reflected in the more than 1% increase in dividend rates on each of the resetting issues in January.

We are cautious about the direction of interest rates because we believe investors are too optimistic about inflation and because of the potential for fewer interest rate cuts by the Bank of Canada than many investors are anticipating. Economic forecasting is quite difficult because the economy is so complex, however the nearly universal consensus that has developed around a slowing path for inflation reminds us of a 1960’s hit song that begins: “Wishin’ and hopin’ and thinkin’ and prayin’”. It is the very complexity of the economy that makes us less optimistic about inflation. Inflation has impacted virtually every segment of the economy, but each sector has a different reaction function. Some sectors, such as supply constrained goods in the pandemic, responded quickly while others, such as wage settlements, are still trying to catch up. In addition, ongoing inflation leads to further inflation. Only a reduction in aggregate demand, as in a recession, has led to inflation being tamed in the past. If the consensus about inflation continuing to slow proves incorrect, the Bank of Canada and other central banks will need to keep interest rates higher for longer than the bond market currently anticipates.

If and when the Bank of Canada begins lowering interest rates, a key consideration will be how low rates might go. For several years, the Bank has been estimating the “neutral” rate, which is neither stimulative nor restrictive, to be between 2.00% and 3.00%. More recently, though, the Bank has indicated that the neutral rate has probably increased. Given the recent bout with inflation, we believe the Bank will be reluctant to lower its target interest rate below 3.00%. We suspect that level differs from investors who started their careers in the last fifteen years, a period when the Bank of Canada kept its interest rate well below 2.00%. We believe that period was an aberration, rather than the new normal, and the Bank will be reluctant to return interest rates to such low levels, given the negative consequences that included a housing bubble. Prior to the Great Financial Crisis, the Bank’s overnight target rates never went below 2.00% and yet the Canadian economy performed reasonably well. Our view is that the Canadian economy can sustain significantly higher interest rates than prevailed in the 2009 to 2022 period. And if money market yields do not fall below 3.00%, we do not see bond yields falling much further.

As we noted last month, given the potential for monetary policy to remain restrictive and interest rates to remain relatively high for several more months, “a possible widespread slowing of the economy remains a concern. We are particularly cautious regarding the real estate sector given its elevated leverage and the need to adjust cap rates to reflect current interest rates and bond yields. In addition, there is a concentration in equity market gains, particularly in the U.S. S&P500 where seven massive tech stocks are dominating the price performance of the other 493 index constituents. Any correction in equities will likely cause a correction in preferred share prices.”

Notwithstanding the growing risk of a recession, we continue to remain confident in the creditworthiness of the issuers in the portfolio, as these companies have successfully weathered previous economic downturns without impacting their ability to pay the dividends on their preferred shares.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.