Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

October 10, 2024

In September, the preferred share market finished with a positive return despite trading sideways for most of the month. Both bond and common equity markets had strong months due to the prospect of declining interest rates. Numerous central banks around the world lowered interest rates, including a 50 basis point cut by the U.S. Federal Reserve, in efforts to stimulate their respective economies. On the last day of the month, preferred share investors received $335 million from the redemptions of the DC.PR.B, DC.PR.D, EFN.PR.E and EQB.PR.C series. Subsequent reinvestment related buying activity resulted in the preferred share market having a late rally. In response to lower bond yields, perpetual issues were the best performing type with an average gain of 2.6%, while rate reset issues gained 0.8% and floating rate issues declined 0.8%. The S&P/TSX Preferred Share index ended the month with a gain of 0.48%.

On September 4th, the Bank of Canada made its third 25 basis point reduction in interest rates since it began easing its fight against inflation. The inflation data released later in the month supported the Bank’s decision as prices declined 0.2% in August and the annual rate fell more than expected to 2.0% from 2.5% the previous month. The unemployment rate also supported the Bank’s decision, as it jumped to 6.6% from 6.4%, with a higher participation rate and surging population growth dominating reasonably strong job creation. Other data gave a more positive impression of the Canadian economy as retail and manufacturing sales were stronger than expected, building permits were up strongly, and capacity utilization was much better than forecasts.

In September, TD Bank announced that it will not be redeeming the TD.PF.A series, with a reset spread of 224 basis points. The extension surprised market participants because, in July, TD redeemed two issues that had reset spreads of 227 and 356 basis points. With its September decision TD was likely taking a conservative approach with its capital levels as it tries to resolve its U.S. anti-money laundering issues. The TD.PF.A series traded down 7.3% on the news and the market starting reevaluating the potential for redemptions of other resetting bank issues in the next few months, including TD.PF.C, BMO.PR.W and CM.PR.P. However, as this is being written, Bank of Montreal has announced that it will be redeeming the BMO.PR.W series.

There was one new issue in the month. Partners Value Split Corp. issued $150 million of a 5.50% hard retractable series, PVS.PR.L, that will mature in June 2030. Proceeds of the issue paid for the maturity of the PVS.PR.F series of shares. Partners Value Split Corp. is a split share structure based on Class A shares of Brookfield Corporation.

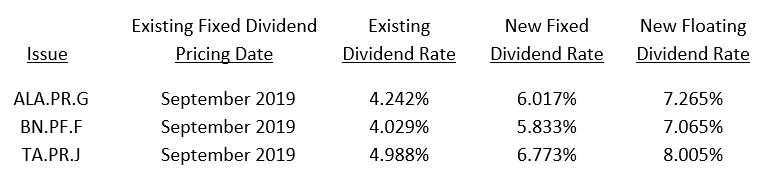

During September, three series of preferred shares reset their dividends. Dividend rates continue to reset significantly higher because the 5-year Canada bond yield is substantially higher than five years ago. Details of the resetting issues were as follows:

During the month, AltaGas announced that the ALA.PR.H floating rate series would not remain outstanding after September 30th. The combination of existing ALA.PR.H investors wanting to remain in the series and ALA.PR.G investors wishing to switch into ALA.PR.H was insufficient to keep it outstanding. Brookfield and TransAlta also announced insufficient investor interest in making the switch to the floating rate series and all shares will be fixed rate ones for the next five years. Despite floating rate yields substantially higher than fixed rate ones, the prospect of further rate cuts by the Bank of Canada is discouraging interest in floating rate shares.

In other issuer news, S&P downgraded the preferred share rating of BCE Inc. to P3(high) from P2(low). The credit rating agency expects the issuer’s debt leverage to remain elevated through 2026 due to increasing competitive pressures, ongoing capital investments, and high dividend payouts. They noted that company management has indicated its desire to reduce leverage by 2026 with non-core assets sales and other corporate initiatives, although the timing and amount is uncertain.

In September, the seven largest preferred share ETFs had an aggregate outflow of $69 million. All but one of the seven ETFs experienced net withdrawals in the month.

J. Zechner Associates Preferred Share Pooled Fund

In September, the fund returned 1.39%, well ahead the S&P/TSX Preferred Share index. The fund’s outperformance was largely a function of two factors. Firstly, the fund held relatively more perpetual type preferred shares, which had the highest returns for the month. Secondly, the fund has an approximate 10% allocation to institutional preferred shares and LRCNs that are not in the S&P/TSX Preferred Share index, and these securities also outperformed the index.

Portfolio activity during the month was mainly focused on increasing the allocation to perpetual type shares. This included additions to CU.PR.H, EMA.PR.C, FTS.PR.G and WN.PR.E.

Outlook and Strategy

With the Bank of Canada having lowered its interest rates three times, many market participants are considering the potential pace and number of future rate cuts. Some Canadian observers have called for the Bank to shift to 50 basis point moves from its current 25 basis point pace. We disagree because there has not been a recent deterioration in the Canadian economy that would necessitate greater urgency on the Bank’s part. In addition, the full impact of the three interest rate cuts is still working its way through the economy.

We expect the Bank will lower interest rates at each of their remaining two scheduled announcement dates this year, barring a significant resurgence in inflation. Should inflation pick up, the Bank is likely to only pause its easing cycle, rather than begin raising rates again. We note that Canada’s annual rate of inflation may experience upward pressure over the balance of this year due to base effects. The final four months of 2023 saw prices decline, so unless that happens again the annual rate will rise from its current 2.0% level.

Of greater importance than the pace of interest rate reductions by the Bank of Canada is the level at which it stops, otherwise known as the terminal rate. The bond market is anticipating several more rate cuts because bond yields are well below the Bank’s target. The Bank’s overnight target is 4.25% while most federal bonds are yielding 3.00% or less. In our opinion, unless the terminal rate is at least 150 basis points lower than the Bank’s current target rate (a level below today’s bond yields), then bond yields may not decline much further. Given the interest rate reductions to date, we are not convinced there will be an additional 150 basis points of rate cuts this cycle.

We are positive on preferred shares because they continue to provide investment grade quality with significantly better yields than corporate bonds, making them an attractive fixed income alternative. As reflected in the resetting issues in September increasing their dividend rates more than 1.75%, the 5-year bond yield continues to be substantially higher than five years ago. Our expectation is that this will remain the case for the next year and preferred shares that reset their dividend rates should continue to see substantial increases in those rates. We note that next year will mark the fifth anniversary of the pandemic and preferred shares resetting in 2025 will benefit from substantial increases in their dividend rates because bond yields should be much higher than in 2020 when yields fell below 0.50%. We anticipate that investors will remain focused on locking in the current attractive dividend yields which should be supportive of perpetual issues. In addition, all types of preferred shares prices should benefit from the ongoing redemption trend as investors reinvest the proceeds among fewer outstanding issues.

Despite the sputtering Canadian economy, we remain confident in the creditworthiness of the issuers in the portfolio, as these companies have successfully weathered previous economic downturns without impacting their ability to pay the dividends on their preferred shares.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.