Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

September 27, 2023

The preferred share market was quite weak in August as prolonged selling of preferred shares combined with equity market volatility in illiquid summer market conditions caused a sharp drop in preferred share prices. Initially, preferred shares traded only slightly lower, but the release of stronger than expected Canadian inflation data at mid-month led to a selloff in the S&P/TSX Composite as well as in bonds. Bond yields rose reflecting investor expectations that monetary policy would need to remain restrictive for longer than previously thought necessary to bring inflation under control. This increased investor concern that a recession could come about with higher rates in the next few quarters. The weakness in equities and bonds appeared to trigger a selloff in preferred shares. However, while stocks and bonds subsequently recovered most of their losses, preferred shares did not.

Preferred shares were also negatively impacted by ongoing selling as investors exited the asset class. Most large preferred share ETFs experienced net withdrawals almost every day in August. In addition, National Bank Investments Inc. announced that it would be closing the NBI Canadian Preferred Equity Private Portfolio Fund. In the coming months the portfolio sub-advisor, Fiera Capital Corporation, will be liquidating the fund’s assets. We estimated the fund had approximately $140 million in assets at the time of the announcement in early August, and the subsequent selling in the liquidation programme contributed to the market weakness over the balance of the month. The S&P/TSX Preferred Share index ended the month with a return of -4.21%.

Canadian economic data released in August was somewhat limited. The unemployment rate edged up to 5.5% from 5.4% the previous month. A small decline in the number of jobs was partially to blame, as was a slight drop in the participation rate. Of note, the unemployment rate jumped from 5.0% to 5.5% in only three months, and that rapid increase led to some speculation that the economy was about to tip into a recession. The labour market data also showed that the increase in average hourly wages accelerated from 3.9% to 5.0%. As noted above, the Consumer Price Index (CPI) data released showed a larger than expected 0.6% increase in the most recent month and a jump in annual inflation from 2.8% to 3.3% a month earlier, suggesting the Bank of Canada’s monetary tightening has yet to be fully effective.

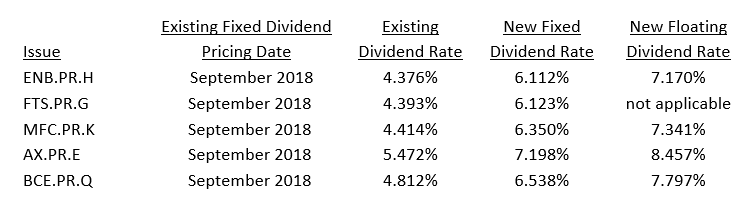

In August, there were no new issues of either traditional $25.00 par or institutional preferred shares.

During the month, five series of preferred shares reset their dividends. Dividend rates continue to reset significantly higher because the 5-year Canada bond yield continues to be substantially higher than five years ago. Details of the resetting issues were as follows:

The sharp rise in dividend rates for these shares resulted in even larger yield increases because each of the series was trading at a substantial discount to par. Using month end values, the new running yields of the BCE.PR.Q (7.65%), ENB.PR.H (8.94%), FTS.PR.G (8.25%), and MFC.PR.K (8.04%) seem very attractive relative to other fixed income alternatives. For taxable investors, the better tax treatment of dividends makes the preferred shares even more compelling.

For several months, the holders of resetting fixed rate preferred shares have been reluctant to choose the floating rate option that has usually been available. In August, though, Enbridge announced that enough ENB.PR.H investors had opted for the floating rate option and a new floating rate ENB.PR.I series would be issued. As a result, on September 1, 2023, Enbridge will have 11,649,398 ENB.PR.H and 2,350,602 ENB.PR.I shares outstanding.

In issuer news, DBRS Limited downgraded its rating on Brompton Split Banc Corp. preferred shares to Pfd-3 from Pfd-3 (high). These preferred shares have experienced a drop in downside protection due to a decline in the portfolio’s net asset value. The portfolio is comprised primarily of the common shares of the six largest Canadian banks, on an approximately equal weighted basis. Also in August, Brookfield Corp. renewed its normal course issuer bid for up to 10% of outstanding preferred shares.

In aggregate the seven largest preferred share ETFs had an inflow of $80 million in August, driven largely by $106 million of net inflows into ZPR. ZPR’s total was mainly due to the two days in which it received $124 million of in-kind deposits. In-kind deposits are ones in which the investor deposits preferred shares rather than cash into the ETF. The timing of those deposits suggested they may have been related to the closure of the NBI Canadian Preferred Equity Private Portfolio Fund. If that was the case, the fund’s manager must have decided liquidity in ZPR was better than the portfolio in the NBI fund. On balance, the ETF outflows in August indicated continued selling of preferred shares despite their very competitive yields.

J. Zechner Associates Preferred Share Pooled Fund

The fund had a return of -2.93% in August, which was significantly better than the S&P/TSX Preferred Share index return. Fund outperformance was largely a function of security selection, which included almost 14% of the fund invested in institutional preferred shares and LRCNs that are not in the S&P/TSX Preferred Share index and which markedly outperformed the index. The fund also held BCE.PR.Q shares which, as a result of its reset dividend rate, was one of the few series of preferred shares with a positive return in the month.

In August, portfolio activity in the fund was limited.

Outlook and Strategy

As noted above, the yield of the 5-year Canada bond continues to be substantially higher than five years ago, which resulted in dividend rate increases of more than 1.50% for the five resetting issues in August. In addition, since all these issues were trading below par, the increase in dividend yields was even higher. The preferred share market continues to provide yields greater than 7.50% on resetting issues and often better than 6.75% on perpetual issues, which we believe are compelling investment opportunities.

As this is being written, Canadian GDP for the second quarter of the year has been reported to have declined an annual rate of 0.2%, much weaker than the expected growth of 1.2%. While much of the shortfall was due to reduced inventory accumulation (which can be reversed in coming quarters), and final domestic demand grew by 1.0% in the quarter, we do not disagree with forecasts that the Bank of Canada will hold interest rates unchanged at its September 6th announcement. However, whether the Bank needs to raise interest rates again, perhaps as soon as its October meeting, will be determined by inflation rather than by the pace of economic growth. That is a concern because inflation appears to be strengthening again despite the substantial increase in interest rates in the last year and a half. We anticipate the annual increase in CPI will accelerate to above 4.0% in the coming months and that will force the Bank of Canada to raise interest rates again. Reasons for the resurgence in the inflation rate will include base year effects as weak increases from a year ago fall out of the calculation, oil prices that have rebounded to the highest level in 10 months, ongoing mortgage rate increases, elevated wage settlements, and a decline in the Canadian exchange rate.

Even if the Bank of Canada does not increase interest rates further, it is unlikely to lower rates for several quarters. Consequently, we believe the risk of a recession beginning in the next few quarters is significant. Indeed, a recession may be required to bring inflation back to the 2% target on a lasting basis. Importantly, we believe the Bank of Canada is willing to tolerate a recession as it struggles to control inflation. Despite this increased economic risk, we continue to remain confident in the creditworthiness of the issuers in the portfolio, as these companies have successfully weathered previous economic downturns without impacting their ability to pay the dividends on their preferred shares.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.