Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

October 12, 2022

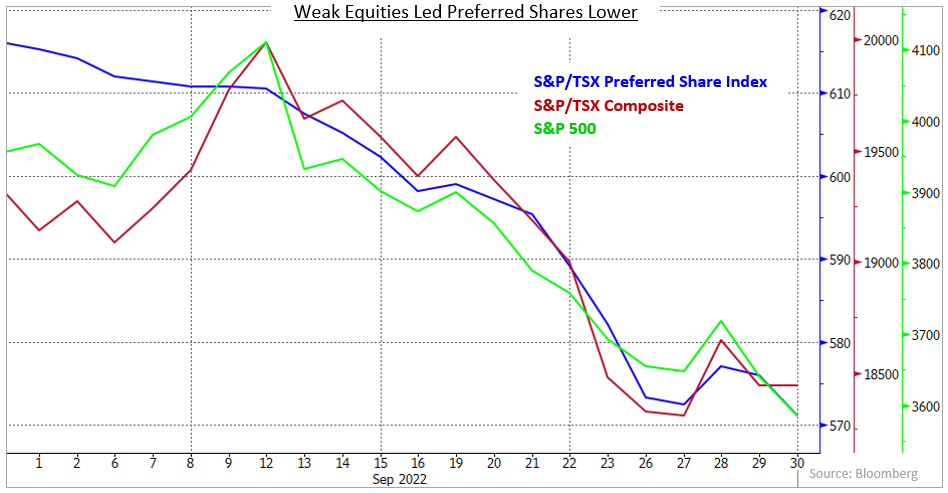

In September, the preferred share market was negatively impacted by volatility in equity markets. Ongoing monetary tightening by the Bank of Canada, the U.S. Federal Reserve, and other central banks led to a selloff in common shares that was followed by preferred shares. The correlation between preferred shares and common equity has been quite high in recent months as the potential for deteriorating economic conditions has generated a risk-off environment. Traditional $25 par value preferred share values have also been hurt by recent new issues of institutional preferred shares and Limited Recourse Capital Notes (LRCNs) by Canadian banks. The banks have been shoring up their balance sheets in advance of some U.S. takeovers as well as preparing for potential economic slowing. The shift from traditional preferred shares (which make up the S&P/TSX index) to the new bank securities by some institutional investors has weakened the traditional preferred share market. The S&P/TSX Preferred Share index returned -6.88% in September.

Canadian economic data mostly contracted in September. Employment fell by 39,700, which was the third monthly decline in a row. (We note some concern about the reliability of the recent jobs data because over 70% of the job losses have occurred in the education sector, which seems improbable.) The decline in jobs pushed the unemployment rate up off its all time low of 4.9% to a level of 5.4%. Retail sales contracted 2.5%, as consumers struggled to deal with rapid inflation and higher interest rates. Canadian inflation slowed to 7.0%, down from 7.6%, but was still near a multi-decade high. This level of inflation is still high enough to keep the Bank of Canada actively tightening monetary conditions. Higher interest rates appear to have subdued the housing market causing monthly home sales and average prices to fall markedly. Year-over-year GDP showed growth at a rate of 4.3%, but the month-over-month growth in GDP was only 0.1% and suggested slower growth ahead.

The Bank of Canada and the U.S. Federal Reserve were both active in September raising their respective monetary policy rates by 75 basis points each, which brought both rates to 3.25%, the highest levels since 2008. While bonds sold off in both countries, the Canadian bond market substantially outperformed its U.S. counterpart. The smaller selloff in Canada bonds was driven by a change in consensus to a lower expected terminal rate for the Bank of Canada’s overnight rate versus the U.S. Fed Funds rate. The market is now expecting the Fed Funds rate to reach 4.50% while the Canadian overnight rate is expected to only touch 4.00%. With both central banks remaining hawkish, though, the potential for a recession increased, which led to widening risk premiums on corporate bonds and appeared to contribute to the weakness in preferred shares.

The only new preferred share issue in the month was an inaugural $600 million institutional preferred share issue from CIBC. It had an initial dividend rate of 7.365% and a reset spread of 420 basis points. The issue was well timed, coming just ahead of the turbulence that occurred in the equity markets. In addition, on the same day in early September, both TD Bank and Bank of Montreal issued LRCNs. TD raised $1.5 billion with an initial coupon rate of 7.283% and a reset spread of 410 basis points, while BMO issued $1.0 billion with an initial coupon rate of 7.325% and a reset spread of 410 basis points. These issues appeared to be related more to maintaining capital levels with pending acquisitions than funding preferred share redemptions. Both BMO and TD have acquisitions in the US targeted to close by the end of this year.

No new redemptions were announced in the month and the small redemptions that occurred on September 30th had no discernable impact on the market.

Only two series of preferred shares reset their dividend rates in September. Each of the series was resetting for the second time, having been originally issued in 2012. In both cases, the new dividend rates were roughly 170 basis points higher than the prevailing rates. The increases in current yields were even larger because both series were trading at significant discounts to their $25 par values. Details of the resetting issues were as follows:

As this is being written, TD Bank has surprised the market announcing that it will not be redeeming its $350 million TD.PF.I series of shares. Instead, the shares, which carry a +301 basis point reset spread, will have a dividend rate of 6.301% for the next five years. It was the first time in over two years that a bank has not called one of its series of traditional $25 par value preferred shares. In that period, banks have been using the proceeds of issues of LRCNs and institutional preferred shares to fund the redemptions, occasionally on financially negative terms. TD Bank’s decision to extend the TD.PF.I shares may have been due to its need to fund the upcoming US$13.4 billion takeover of First Horizon Bank in the U.S. during uncertain financial conditions, but the extension increases the uncertainty about whether other bank preferred shares will be redeemed. Most of the redemptions in the last two years involved series of shares with very large reset spreads, while shares that may be redeemed in 2023 have much smaller ones.

In other news, Fairfax Financial announced its intention to purchase, through a Normal Course Issuer Bid, up to 10% of its outstanding preferred shares over the next year commencing on September 30th.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.