Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

December 15, 2025

The preferred share market had a seesaw month in November, first declining, then rallying back to finish little changed. The first part of the month was dominated by new issue supply totalling $801 million, while the latter part of the month had $550 million of redemptions requiring reinvestment and announcements of a further $671 million of future redemptions. The surge of new issues caused prices to temporarily dip, but the redemptions resulted in buying as investors tried to reinvest their proceeds. Performance among the three types of shares diverged, with rate reset and floating rate issues having positive returns of 0.4% and 1.5% respectively, while perpetual issues had a negative return of 1.1%. Three of the new issues were perpetual type shares that had relatively attractive dividend yields that put pressure on the price of existing perpetual issues. The S&P/TSX Preferred Share Index ended the month with a small loss of -0.08%.

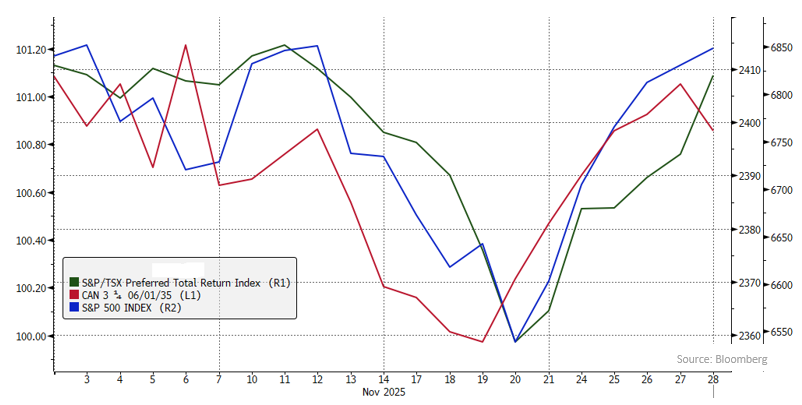

The selloff in the preferred share market and subsequent rebound coincidentally matched the pattern in bonds and stocks during November. As can be seen in the following chart, Canadian bonds and U.S. stocks also declined in the first three weeks of the month before recovering to finish close to unchanged. While the moves in preferred shares appeared to be linked to new issues and redemptions, bonds and stocks appeared to be tracking expectations for interest rates. On November 20th, the U.S. unemployment rate was shown to have risen to 4.4%, outside of the pandemic the highest rate in more than eight years.

The news led to substantial speculation that the U.S. Federal Reserve would lower rates at its December 10th meeting, and bonds and equities rallied on the optimism of easier monetary policy.

Canadian economic data was generally positive in November. The unemployment rate unexpectedly declined to 6.9% from 7.1%, as a second consecutive month of robust job creation more than offset a rise in the participation rate. Canadian GDP was estimated to have grown at an annual rate of 2.6%, well above consensus expectation of 0.5% growth. In addition, estimates of GDP growth in the last three years were revised higher, suggesting there was less slack currently than had been thought. Inflation declined to 2.2% from 2.4%, and the core measures of inflation declined to 2.95% from 3.10% the previous month.

On November 4th, the Government of Canada released its first budget in a year and a half that forecast a deficit of $78 billion, much higher than its previous estimate of $42 billion, but well below some predictions that were as high as $100 billion. The government had anticipated the deficit to be sharply higher and it had increased the pace of bond issuance last spring to help fund the increase. Going forward, the amount of gross issuance is expected to slow modestly, but with fewer maturities scheduled for next year net issuance will be much higher. Despite the large jump in the size of the deficit, the bond market reaction was muted because the deficit was not as bad as some had feared.

In November, the four new issues were the most significant events in the preferred share market. All had strong demand, both from institutional and retail investors, and finished the month trading higher than par. The first three issues were perpetual series. In the first week of the month, Intact Financial issued the $150 million IFC.PR.M series with a dividend rate of 5.50%. Next, Canadian Utilities issued the $201 million CU.PR.K series with a dividend rate of 5.60%. The following day Power Corporation issued the $200 million POW.PR.I series with a dividend rate of 5.65%. Finally, Brookfield Corporation issued the $250 million BN.PF.M rate reset series with a floor dividend rate of 5.65% and a reset spread of 280 basis points. The Brookfield issue was the first rate reset issue since March 2021.

Late in the month, three issuers announced redemptions of four series of preferred shares on December 31st. First, Brookfield Corporation announced its intention to redeem the $246 million BN.PF.H series, which has a reset spread of 417 basis points. The issuer stated that the proceeds from the new BN.PF.M series would be used for this redemption. A week later, Brookfield Infrastructure announced its intention to redeem the $125 million BIP.PR.B series, which has a reset spread of 453 basis points. Finally, Fairfax Financial announced its intention to redeem the $262 million FFH.PR.I series and the related $38 million FFH.PR.J series, which had reset spreads of 285 basis points. The market had been anticipating these announcements and there was not a significant move in their share prices on the news. However, the announcements helped to reverse the negative sentiment of the first half of the month.

In November, there was news regarding two series resetting their dividend rates. Great West Lifeco announced that it will not be redeeming the GWO.PR.N series, with a fixed dividend rate of 1.749%, on December 31st. As this is being written, the issuer announced the new fixed dividend rate is 4.090% and the new floating dividend rate is 3.518%. Investors will have until December 16th to make their decision to remain in the current series or switch to the floating series. Also, during the month, BCE Inc announced the BCE.PR.R fixed rate series would remain outstanding as enough investors wanted to remain in the series rather than switch into the BCE.PR.Q floating rate series. The new fixed dividend rate is 4.733%.

Also in the month, ECN Capital Corp announced an agreement to be acquired by an investor group led by Warburg Pincus LLC. The investor group will acquire the issuer’s preferred shares, ECN.PR.C, for $26.00 plus all accrued and unpaid dividends. The series is not redeemable until June 30, 2027, therefore, acquisition of the series is conditional on the approval of at least 66 2/3% of the votes cast by the series shareholders present or represented by proxy at a special meeting of shareholders expected to be held in January 2026. Completion of the acquisition is not conditional on obtaining approval from the ECN.PR.C series holders and if not obtained, the series will remain outstanding following closing of the transaction in accordance with its terms. The ECN.PR.C series increased 10% on the news.

In November, the seven largest preferred share ETFs had an aggregate inflow totaling $3 million. Each of the ETFs had relatively small inflows or outflows.

J. Zechner Associates Preferred Share Pooled Fund

In November, the fund had a flat return, which was slightly better than the S&P/TSX Preferred Share index.

Portfolio activity during the month included selling the CU.PR.E position and a portion of the CU.PR.H position to switch into the new CU.PR.K issue, and pickup approximately 25 basis points in yield. A portion of the NPI.PR.A position was sold following disappointing results and a cut to the issuer’s common dividend. In addition, we sold all the Royal Bank 7.408% institutional preferred shares, which had appreciated in price and no longer offered an attractive yield to call.

Outlook and Strategy

Going forward, we see several potential sources of market volatility in the next few months. Clearly trade negotiations remain a source of risk, with President Trump potentially using a threat of cancelling the USMCA as a negotiating tactic. Elevated equity valuations are another risk, as price/earnings ratios are at historically high levels. Should stock markets correct, we would expect a flight-to-safety bid to occur for government bonds. We are also concerned that all of Trump’s threatened tariffs have not been fully implemented, so their negative economic impact has not yet occurred. And a final concern is the selection of the next Chair of the Fed. Should Trump choose a candidate that is perceived as wanting excessive easing with insufficient concern regarding inflation, bond investors may vote with their feet.

The 5-year Canada bond yield continues to be well above the extremely low levels of five years ago. As noted above, the resetting Great West Lifeco issue increased its dividend rate by more than 230 basis points. We believe the Bank of Canada will leave interest rates unchanged at its December 10th announcement. Without further encouragement from the Bank of Canada, we believe bonds are likely to remain in a trading range. Accordingly, we do not expect the 5-year Canada bond yield to rally much from current levels and continue to anticipate large increases in resetting dividend rates for the next few months.

As evident by the performance of the preferred share market over the month, the redemption trend continues to support the market. In early December, investors will receive a total of the $ 775 million from the CU.PR.I, PPL.PR.I, RY.PR.N and RY.PR.O series redemptions, which were announced in October. Also, on the last day of December, investors will receive a total of $671 million from the BIP.PR.B, BN.PF.H, FFH.PR.I and FFH.PR.J redemptions. We expect most of the redemption proceeds will be reinvested in other outstanding preferred share series.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.