Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

June 6, 2024

In May, the preferred share market moved sharply higher. The month began strongly with reinvestment related buying appearing to carry over from the last day of April when investors received $850 million from redemptions. In the last week of the month, additional reinvestment related buying activity boosted the market as investors received another $1.35 billion from redemptions. In addition, a decline in Canada bond yields contributed to strong perpetual share price performance during the month. Over the entire month, perpetual issues generated the best returns, rising 5.5%, while rate reset returns were more modest at 2.7%. The S&P/TSX Preferred Share index ended the month with a gain of 2.94%.

Economic growth in Canada appeared to stall at the end of the first quarter as GDP failed to increase in March. Growth in GDP during the first three months of the year was at a rate of 1.7%, well below the expected 2.2% pace. In addition, the estimate of growth in the fourth quarter of last year was revised down from 1.0% to only 0.1%. Other disappointing data included weaker than expected retail sales and manufacturing sales. The unemployment rate held steady at 6.1%, as job creation of 90,400 new positions offset the growth in Canada’s population as well as a small increase in the participation rate. The headline CPI inflation rate declined to 2.7% from 2.9%, while core price measures fell from 3.1% to 2.8%. The CPI measure was the fourth consecutive month below 3.0%, and combined with slow economic growth caused many observers to call for the Bank of Canada to begin easing monetary policy at its scheduled June 5th announcement.

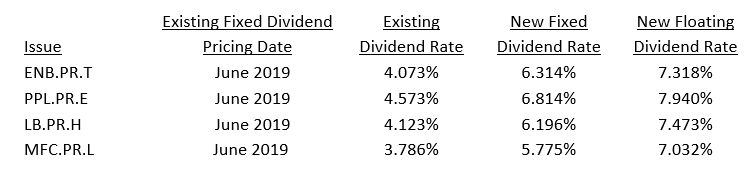

In May, there were no new issues of traditional $25.00 par or institutional preferred shares. During the month, Element Fleet Management announced that it will redeem the $128 million EFN.PR.C series, which has a reset spread of 481 basis points. In addition, Capital Power Corp announced that it will redeem the $150 million CPX.PR.K series, which has a reset spread of 415 basis points and a floor dividend rate of 5.75%. Year to date, announced redemptions have totaled $2.5 billion and been very supportive of the preferred share market’s positive performance. During the month, four series of preferred shares reset their dividends. Dividend rates continued to reset significantly higher because the 5-year Canada bond yield was substantially higher than five years ago. Details of the resetting issues were as follows:

In May, Enbridge Inc, Pembina Pipeline Corp and National Bank announced that an insufficient number of investors wanted to make the switch into their respective floating rate series and all recently reset shares will remain fixed rate ones. Despite floating rate yields that are substantially higher than fixed rate ones, preferred share investors remain concerned that interest rates will fall significantly in the next year and take floating rate dividends below fixed rate levels.

In aggregate, the seven largest preferred share ETFs had an outflow of $52 million in May. The three largest, ZPR, HPR and CPD, accounted for all the outflows with the others having small inflows. Despite another strong month and a robust year to date return for the preferred share market, these ETFs have had aggregate outflows in each month of 2024.

J. Zechner Associates Preferred Share Pooled Fund

In May, the fund earned 3.31% and outperformed the S&P/TSX Preferred Share index. The fund’s outperformance was largely a function of security selection, particularly in two areas. Firstly, fund performance benefited from its approximate 11% allocation to bank institutional preferred shares that are not in the S&P/TSX Preferred Share index. Several of these issues paid dividends in May. Given their high dividend rates and semi-annual payments, these relatively large payments have an outsized positive effect on performance in the month they are received. Secondly, the fund held relatively more perpetual type preferred shares which had the highest returns for the month.

Portfolio activity during the month included selling one half of the TD.PF.C position, which had performed well since purchased. Also, we concluded a couple of switches started last month with small purchases of AQN.PR.D and TRP.PR.D.

Outlook and Strategy

Despite robust year to date performance, we are positive on preferred shares because they continue to offer investment grade quality with significantly better yields than corporate bonds, making them an attractive fixed income alternative. The increase in bond yields in the last five years is resulting in substantial increases in dividend rates on resetting issues, which is reflected in three of four resetting issues in May increasing their dividend rates more than 2.00%. Currently, the yield of 5-year Canada bonds is approximately 3.42%, which compares very favourably to the 1.45% average yield that existed in the second half of 2019. We anticipate all preferred share series resetting their dividend rates this year will see substantial increases in those rates.

As this is being written, we are awaiting the Bank of Canada’s June 5th interest rate decision. We believe the Bank will start lowering interest rates either at that meeting or its subsequent one on July 24th. Economic growth has been disappointing for several months, especially if looked at on a per capita basis. With Canada’s population growing by more than 3% in the last year, and annual growth slowing to just 0.6%, the per capita trend is distinctly negative.

The Bank of Canada has indicated that it anticipates its easing cycle, whenever it starts, will be a gradual one, which suggests 25 basis point increments. The potential scope for the Bank to lower interest rates will be limited by several factors. The first is inflation, which needs to continue to recede. Any reacceleration in inflation would likely lead to a pause in the easing cycle. A second factor is the exchange rate. In the past, if Canadian interest rates fell substantially lower than U.S. ones, the Loonie declined in value, sometimes sharply. While a drop in the exchange rate is stimulative to the Canadian export sector, it also increases import prices leading to higher inflation. A third factor will be the reaction of the housing sector. The Bank will want to avoid a repetition of the housing bubble it caused by keeping borrowing rates too low. Should rate cuts result in a surge in demand when Canada already has a housing shortage, the Bank will need to slow the pace of future easing.

We believe the Bank of Canada will not lower interest rates as much as the market expects. For several years, the Bank has been estimating the “neutral” interest rate, which is neither stimulative nor restrictive, to be between 2.00% and 3.00%. More recently, though, the Bank has indicated that the neutral rate has probably increased. Our view is that the Canadian economy can sustain significantly higher interest rates than prevailed in the 2009 to 2022 period.

Notwithstanding Canadian economic uncertainty, we continue to remain confident in the creditworthiness of the issuers in the portfolio, as these companies have successfully weathered previous economic downturns without impacting their ability to pay the dividends on their preferred shares.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.