Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

January 12, 2024

In December, preferred shares had a much more subdued performance than the large gains enjoyed during November. Preferred share prices traded down for the first part of the month as investors seemed to take profits following November’s upward surge. However, the key event for financial markets in the month was the December 13th meeting of the U.S. Federal Reserve, which left its interest rates unchanged but indicated that rate reductions were likely in the next 12 months. The market reaction was swift, with bond yields dropping significantly and equity markets moving sharply higher. Canadian bond yields continued to decline over the balance of the month. Preferred shares did not have similar sized returns as bonds and common equities. It took until the last day of the month, aided with the proceeds of two redemptions likely being reinvested, for the index return to turn positive. The S&P/TSX Preferred Share index ended the month with a gain of 0.82%.

The relatively subdued performance of preferred shares in December compared with bonds and equities may also have been due to a classic fear versus greed debate for rate reset preferred share investors. Since late October 5-year Canada bond yields have plunged over 1.00%, thereby significantly reducing potential dividend increases for resetting preferred shares. However, with the yields of alternative fixed income investments dropping sharply, the yields of preferred shares became relatively more attractive. In the end, greed appeared to win out and preferred share prices moved higher.

Economic data received in the month showed the Canadian economy was struggling to grow. Indeed, Canadian GDP failed to expand in October, although the year over year pace of growth increased from 0.6% to a slightly less tepid 0.9% pace. The unemployment rate rose to 5.8% from 5.7% as robust job creation of 24,900 positions was overwhelmed by the 36,000 person increase in the labour force. Adding to the gloom, housing starts were weaker than expected in November, as starts of buildings with multiple units dropped 26% from the previous month over affordability concerns.

The Bank of Canada met a week before the Fed and left its interest rates unchanged. The Bank said it wanted to see more progress on slowing inflation although it acknowledged the economy was no longer in excess demand. As it happened, inflation in November was subsequently shown to be higher than forecasts due to higher food and clothing prices and the year over year rate held steady at 3.1%. With December 2022’s monthly decline of 0.6% falling out of the next annual calculation, it may be difficult to see inflation declining below 3.0% for the next couple of months.

In December, there were no new issues of traditional $25.00 par or institutional preferred shares. As noted above, on the last day of the month, two redemptions announced in November, that of the $200 million ALA.PR.E and $115 million EFN.PR.A series, were completed. The redemptions put upward pressure on the preferred share market as investors, particularly funds, needed to promptly reinvest the proceeds.

Bank of Nova Scotia took the preferred share market by surprise in December when it announced that it would redeem the BNS.PR.I issue which had closed that day at $23.20. The issue had a reset spread of 243 bps and recently, most bank rate reset issues with similar reset spread levels have not been redeemed. The exception was in September, when TD Bank redeemed its TD.PF.K series with a reset spread of 259 bps. However, TD Bank had much higher than required capital following the termination of an acquisition and was trying to reduce its total capital. The BNS.PR.I shares were Bank of Nova Scotia’s only remaining $25.00 par preferred shares, so it appears that the bank was simplifying its capital structure.

Also during the month, S&P downgraded the credit rating of Brookfield Office Properties, lowering its preferred share rating from P-3 to P-4 with a continued negative outlook. S&P expects “sector headwinds facing commercial office real estate will generally remain in place over the next several years, with weaker tenant retention, lower occupancy, and heightened incentives (through tenant inducements) to attract new tenants”. The S&P/TSX Preferred Share index eligibility criteria uses the lowest rating among the rating agencies and requires preferred shares to have a minimum rating of P-3. Therefore, Brookfield Office Properties’ eight series of preferred shares will be removed from the index. The news resulted in further losses for those shares, which had already been among the weakest performers in 2023. In other issuer news, after placing Laurentian Bank of Canada’s credit rating “under review with negative implications” in November, DBRS Morningstar downgraded it in December. This resulted in the rating on the LB.PR.H series moving from Pfd-3 to Pfd-3L with a negative trend. DBRS’s rating reflects its opinion that the bank’s “franchise strength and profitability prospects have significantly weakened with a limited visibility on the Bank’s long-term strategic path”.

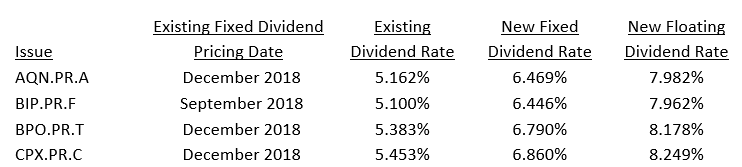

During the month, four series of preferred shares reset their dividends. Dividend rates are still resetting significantly higher because the 5-year Canada bond yield continues to be substantially higher than five years ago. Details of the resetting issues were as follows:

By the end of the month, Algonquin Power and Utility, Brookfield Infrastructure, Brookfield Office Properties, and Capital Power Corp. each announced there was insufficient investor interest in making the switch to the floating rate option and all shares will remain fixed rate ones. Despite floating rate yields remaining substantially higher than fixed rate ones and interest rates potentially staying higher for longer, preferred share investors continue to appear worried that interest rates will fall in the next year and take floating rate dividends below fixed rate levels.

Also, during the month, the Office of the Superintendent of Financial Institutions announced that it will not be making any change to the minimum regulatory capital required to be held by the six largest banks, which was last increased in June 2023. All other things being equal, this would suggest that redemption of bank preferred shares should be less likely in the near term.

In aggregate the seven largest preferred share ETFs had an inflow of $2 million in December.

J. Zechner Associates Preferred Share Pooled Fund

The fund had a return of 2.55% in December, which was well ahead of the S&P/TSX Preferred Share index return. During the month, all issue types had positive returns, although rate reset issues lagged and perpetual issues had returns almost twice that of rate reset issues. Fund outperformance was largely a function of security selection. Good security selection of course depends on choosing what to hold and what to avoid.

Given S&P’s downgrade of Brookfield Office Properties’ preferred shares, it is not surprising that the issuer significantly underperformed the market, with several issues having price declines of more than 10% during December. We have been concerned about the commercial office real estate sector for several months given its elevated leverage and negative outlook. Accordingly, we had deliberately avoided the issuer, and the fund performance benefited as a result. We note that many other preferred share funds had not made the same decision regarding Brookfield Office Properties.

Portfolio activity during the month included finishing the switch from AQN.PR.D into AQN.PR.A, which locks in the certainty of a high dividend yield for five years versus one resetting in several months. We sold the position in BNS.PR.I, prior to the redemption announcement, as the shares had moved significantly higher since the announcement of the TD.PF.K redemption. In addition, we added to several existing positions in rate reset, perpetual and institutional preferred shares to invest cash that had accumulated from dividend payments and new investor fund purchases.

Outlook and Strategy

Despite a second consecutive month of lower bond yields and positive preferred share performance, we believe the market continues to offer attractive yields. Many perpetual and rate reset issues can be purchased with yields greater than 6.5% and 7.5% respectively. In addition, the 5-year bond yield continues to be substantially higher than five years ago resulting in substantial increases in dividend rates on resetting issues, which is reflected in the more than 1.25% increase in dividend rates on each of the resetting issues in December.

As noted last month, we are concerned that the recent bond rally may have gone too far. We are not convinced that inflation will continue to quickly fall to the 2% target, in part because the comparison with price moves last year will be more challenging in December. As well, the sharp drop in bond yields has loosened financial conditions markedly, with lower mortgage rates being an obvious example. That means there is less pressure on the Bank of Canada to reduce interest rates. In addition, we think investors have not yet focused on how much (or how little) the Bank will lower rates when it does begin to loosen monetary conditions. The Bank has suggested that its estimate of the neutral rate, which is neither stimulative nor restrictive, may be revised higher. While we believe the rally may have gone too far too soon, we do not believe it is likely to fully reverse. The high yields seen in October will likely prove to be the peak ones for this cycle.

Given the potential for the Bank of Canada to keep monetary policy restrictive for several more months, a possible widespread slowing of the economy remains a concern. We are particularly cautious regarding the real estate sector given its elevated leverage and the need to adjust cap rates to reflect current interest rates and bond yields. In addition, there is a concentration in equity market gains, particularly in the U.S. S&P500 where seven massive tech stocks are dominating the price performance of the other 493 index constituents. Any correction in equities will likely cause a correction in preferred share prices.

Notwithstanding the growing risk of a recession, we continue to remain confident in the creditworthiness of the issuers in the portfolio, as these companies have successfully weathered previous economic downturns without impacting their ability to pay the dividends on their preferred shares.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.