Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

January 12, 2023

In December, the preferred share market was negatively impacted by volatility in equity markets. Common share markets started the month with a weak tone as investors focused on the upcoming Bank of Canada and U.S. Federal Reserve interest rate decisions on December 7th and December 14th respectively. Concern over continued monetary tightening by the central banks led to a selloff which had preferred shares trading lower until after the central bank decisions were made. However, in the last week of the month, preferred share prices moved higher and recovered almost half of the month to date losses. The S&P/TSX Preferred Share index ended the month with a return of -1.75%.

Economic data released in December continued to show strength in the Canadian economy. Employment in November increased by 10,100 jobs which pushed the unemployment rate down to 5.1%, just above the all-time low level of 4.9%. October’s retail sales rebounded strongly from the previous month’s decline, and year-over-year GDP growth was estimated at 3.1%.

With its 50 basis point increase in December, the Bank of Canada has raised interest rates by 4.00% since March but the economy has not yet weakened significantly. In addition, inflation at 6.8% has slowed only 0.2% in the last four months despite this aggressive tightening. Given that changes in monetary policy can take up to a year to have an impact on the economy, the Bank is approaching the difficult decision when it must determine if the interest rate increases to date are enough to have the desired impact on inflationary pressures. In its December statement, the Bank said it was considering whether further interest rate increases were needed, rather than saying they were likely. The bond market took this change as a hint that a pause in rate increases might occur soon. However, given the strong current performance of the Canadian economy and the minimal downward movement of inflation, additional rate hikes remain possible.

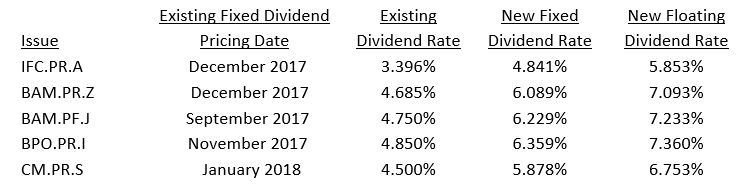

During the month, there were no new issues or redemptions of preferred shares. All preferred share series that had reset dates in December were extended. In addition, CIBC announced that it will not be redeeming its $450 million CM.PR.S shares in January 2023. These shares, which have a reset spread of 245 basis points, will have a dividend rate of 5.878% for the next five years. CIBC’s decision was not a surprise as the last two bank rate reset issues that could be redeemed, TD Bank’s TD.PF.I and National Bank’s NA.PR.C, were not. These issues had much higher reset spreads, 301 and 343 basis points respectively, than CM.PR.S, making them more expensive to leave outstanding than the CIBC shares. Also, before the CIBC decision, the Office of the Superintendent of Financial Institutions announced that it would require banks to increase the minimum regulatory capital they hold by February 1, 2023, thereby making redemptions less likely.

All resetting issues raised their dividend rates substantially in December because yields of 5-year Canada bonds are substantially higher than five years ago. As each issue was trading at a discount to par, the resultant increases in share yields were even larger than the changes in the dividend rates. Details of the resetting issues were as follows:

The deadline for CM.PR.S holders to make the decision on switching into the floating rate series has not yet passed. All the other issuers subsequently announced that, despite the more than 100 basis point initial rate advantage for the floating rate series, insufficient numbers of holders wanted to make the switch into the floating rate alternative. Therefore, all four series will have fixed rate dividends for the next five years. With bond and money market yields expected to peak within the next year or so, investors continue to choose the certainty of a relatively high fixed rate dividend for the next 5 years rather than the floating rate alternative that might decline if and when the Bank of Canada eases monetary policy.

In issuer news, Brookfield Asset Management Inc. announced that it was changing its name to Brookfield Corporation and its ticker symbol from BAM to BN. Most of their preferred share series tickers simply replaced BAM with BN, for example BAM.PR.B changed to BN.PR.B and BAM.PF.A changed to BN.PF.A. However, two series also changed the series letter, BAM.PR.E changed to BN.PF.K and BAM.PR.G changed to BN.PF.L. In addition, Brookfield Renewable announced that it was renewing its normal course issuer bid (NCIB) for preferred shares and units. Under the program they will be allowed to purchase up to 10% of each outstanding of both BEP preferred units and BRF preferred shares.

The seven largest preferred share ETFs experienced net outflows of $78 million in December. The experience of each fund varied, however, with HPR having a $82 million outflow while DXP had a $41 million inflow. We believe some of the difference across ETFs was related to tax-loss selling into year end.

December preferred share trading conditions were good with several days experiencing above average daily trading volumes, until the holiday week when, unsurprisingly, trading volumes were much lower.

J. Zechner Associates Preferred Share Pooled Fund

The fund returned -0.72% in December, which was significantly better than the S&P/TSX Preferred Share index return. Rate reset issues with low reset spreads were the worst performing sector in the index, and the fund benefited from limited exposure to those issues. We also noted that in the thin, illiquid trading conditions that occurred near the end of the year one holding spiked higher in price by approximately 10%. This inflated the fund’s performance by about 0.17%, however, the price appreciation has subsequently reversed on the first trading day of the new year.

During the month, we added to existing positions in several perpetual issues had yields greater than 6.25%, which we believed provided good long term value. In addition, we continued to switch from RY.PR.N into IFC.PR.K shares to pick up incremental yield. Other transactions included adding to existing positions in the National Bank LRCN and the rate reset issue PPL.PR.O (which recently reset its dividend rate), both with attractive yields of about 7.50%. We also added to IAF.PR.I, a rate reset issue, which trades below par and resets in March 2023 with a new dividend rate that we expect will be attractive.

Outlook and Strategy

While we think a recession is increasingly likely in Canada, the economy continues to grow, and unemployment remains low. Inflation remains well above the Bank of Canada’s 2% target, and we believe the Bank of Canada will probably raise rates again at its next meeting on January 25th. We also believe the bond market is currently too optimistic about when the Bank might start lowering interest rates. Unless inflation falls quickly in the coming months, it seems likely that the Bank will not lower rates until late this year or early 2024. As the market adjusts to rates staying higher for longer, we believe that the 5-year bond yield is more likely to rise from the current levels than fall substantially in the next twelve months.

As seen with the issues that reset in December, the current 5-year bond yield results in substantially higher dividend rates. We believe rate reset issues, particularly those with reset dates in the next few months, will benefit from sharply higher dividend rates when they reset. Preferred shares are offering historically high yields, and given the advantageous tax treatment of dividends, they look very attractive versus alternative fixed income instruments.

Given the sharp increase in interest rates by the Bank of Canada this year, the risk of a recession has increased substantially. It is difficult to forecast the severity of a possible recession, however, we remain confident in the creditworthiness of the issuers in the portfolio, as these companies have successfully weathered previous economic downturns without impacting their ability to pay dividends on their preferred shares. Also, as can be seen from the portfolio activity this month, we are being conservative in additions to the portfolio. We will be patient about taking advantage of any weakness in the market that may occur in a slowing economy.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.