Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

January 20, 2017

The growth in institutional participation in the preferred share market that has occurred over the last couple of years is unlikely to reverse any time soon. With supply somewhat limited by the relatively few issuers utilizing preferred shares, the increased demand by institutional investors bodes well for preferred share performance. Preferred shares remain cheap versus bonds issued from the same companies, even before the tax advantages of dividends versus interest are considered. While preferred shares are economically sensitive (they do not perform well in recessions), we believe economic growth will remain positive in 2017. Consequently, we are bullish on preferred shares and believe they should play an ongoing role in investors’ diversified portfolios.

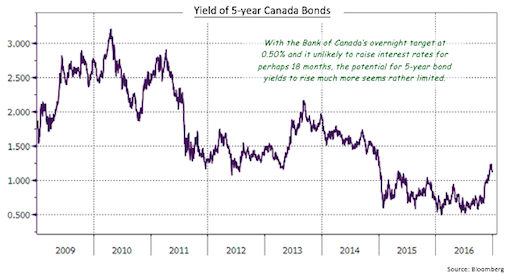

In recent months, rate reset issues have outperformed other sectors of the preferred share market. In part, this reflected the rise in the 5-year Canada Bond yield from record low levels of roughly 0.50% to about 1.10%. With some potential that the Bank of Canada could reduce interest rates in 2017 and very little possibility of a rate increase before mid-2018, the potential for 5-year bond yields to continue to increase seems limited. As a result, the support for rate reset shares from rising bond yields may wane.

The superior performance of rate reset issues in recent months also appears to have been a rebound from their massive underperformance in 2015 and early in 2016. As a result of the strong move upward in rate reset prices, perpetual issues have become relatively more attractive. Combined with eye-catching yields of 5.50% or more, the relative value proposition of perpetual issues has improved significantly. As a result, we are monitoring the market for potential opportunities to add to the perpetual holdings.

Looking ahead to 2017, there are approximately $6.1 billion of rate reset issues that will be resetting their dividend rates. In contrast with the preferred shares that reset in 2015 and 2016 that had reset spreads generally below 200 basis points, the ones rolling over in 2017 have reset spreads between 260 and 350 basis points. The larger reset spreads combined with higher current 5-year Canada Bond yields mean that most dividend rates will not experience as severe reductions as those of the last two years. However, current new issue reset spreads are well above most of those rolling over this year, so we anticipate that issuers will, in most cases, choose not to redeem the outstanding issues.

Within the perpetual sector of the preferred share market, we do anticipate a few redemptions. A number of issues have dividend rates of 5.80% or higher and issuers will be considering the benefit of refinancing the issues using lower rate reset issues. In addition, the BNS.PR.N and BMO.PR.L perpetual issues become callable at par for the first time in 2017 and because they are not NVCC-compliant they are probably going to be redeemed by their respective banks.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.