Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

September 4, 2022

In August, the preferred share market continued the positive momentum that started in the last week of July. While perpetual issues outperformed the previous month, it was rate reset issues that were the best performing sector in August. The strong performance of rate reset issues was a somewhat delayed recovery following the weakness caused by two institutional rate reset issues in late July. The S&P/TSX Preferred Share index returned +1.12% in the month and its positive result was in contrast with the negative returns of both equities and bonds.

Canadian economic data released in August was mixed. July’s employment declined by 30,600, but despite the fall in employment, the unemployment rate held at an all-time low of 4.9% as the participation rate also declined. Canada’s GDP expanded at a 3.3% annualized real rate in the second quarter which was higher than the previous quarter, although below market expectations. On a nominal basis (i.e. including inflation) Canadian GDP increased at an eye-popping 17.9% pace in the quarter. However, the economy seemed to be losing momentum with June’s real growth showing a moderate 0.1% expansion. Expectations are for annualized real growth to fall below 1.5% in the second half of this year, with an increasing possibility of recession due to aggressive rate hikes by the Bank of Canada. The Canadian housing sector continued to see lower home sales, as well as falling prices. Year-over-year inflation declined moderately from the prior month’s peak to 7.6% in July, but this remained far above the Bank of Canada’s 2% target.

Despite no new issuance, August was a busy month for preferred share issuers. With eight rate reset preferred series scheduled to reset in September, their respective issuers had decisions to make on whether to redeem or extend these issues. Two companies chose to issue hybrid bonds, with the proceeds to be used to redeem preferred shares. AltaGas Ltd. issued a 7.35% hybrid bond to redeem the US$200 million ALA.PR.C series. Capital Power issued a 7.95% hybrid bond and will use the proceeds to redeem the CPX.PR.I series. This $150 million series of preferred shares was to reset on September 30th with what would have been a new dividend rate of approximately 7.15% given its reset spread of 412 basis points.

On an after-tax basis, it made economic sense for Capital Power to redeem the preferred shares as the hybrid bond’s interest payments will be tax deductible. Two other companies used existing cash balances to redeem their preferred shares. Birchcliff Energy announced that it will redeem all the 2,000,000 shares outstanding of the BIR.PR.A rate reset series and all the 1,528,219 shares outstanding of the BIR.PR.C retractable series on September 30 th . Artis Real Estate Investment Trust announced that it will redeem all the 3,248,300 outstanding AX.PR.A preferred units also on September 30th .

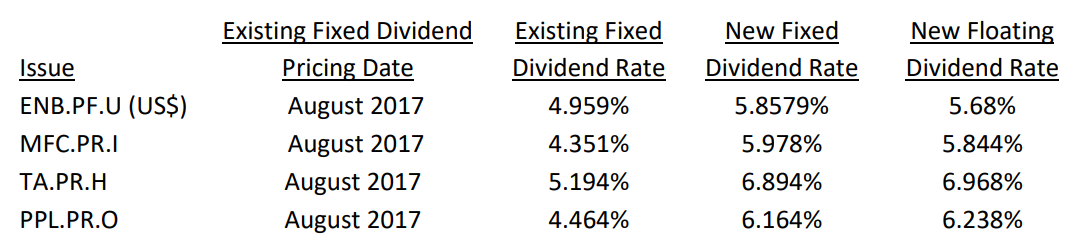

Four issuers chose not to redeem their series of preferred shares and consequently reset their dividend ratessubstantially higherthan their existing dividend rates. Each of the series was resetting for the second time, having been originally issued in 2012. Details of the resetting issues were as follows:

Enbridge announced that an insufficient number of ENB.PR.U holders wanted to make the switch into the floating rate series, therefore all shares will be fixed rate ones for the next five years. Holders of the other three issues had until various dates in September to make their elections.

Also in August, BCE Inc. announced that as of September 1, 2022, the BCE.PR.A will have a new fixed dividend rate of 4.94% for the next five years. Subsequently, the company announced that 1,067,517 of the 11,397,196 fixed-rate BCE.PR.A shares were tendered for conversion on September 1, 2022, into the floating-rate BCE.PR.B series. In addition, 1,977,982 of the 8,599,204 BCE.PR.B shares were tendered for conversion on September 1, 2022, into BCE.PR.A series. Consequently, on September 1, 2022, BCE will have 12,307,661 BCE.PR.A and 7,688,739 BCE.PR.B shares issued and outstanding.

Notwithstanding the substantial rise in interest rates caused by the Bank of Canada’s monetary tightening, and the resultant jump in floating rate dividend rates above fixed dividend rates, there has not been a noticeable rise in demand for floating rate preferred shares. It appears holders of resetting preferred shares prefer to lock in the new, relatively high fixed rates for the next five years rather than taking the chance that floating rates may fall once the Bank of Canada is finished its fight against inflation.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.