Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

June 2, 2022

The preferred share market enjoyed robust gains in May as it rebounded from weak performance in April. In doing so, preferred shares generated the strongest monthly performance the market has seen in more than a years’ time and the first positive month this year. On a relative basis, the preferred market strongly outperformed equities and corporate bonds during the period. In relatively poor liquidity conditions, preferred shares were driven by redemptions that totaled $1.5 billion. The S&P/TSX Preferred Share index returned 5.01% in May.

Canadian economic activity showed continued growth in May. Canadian year-over-year GDP came in at 3.5% and the unemployment rate fell to 5.2%, a new all-time low. Starts of new homes were stronger than expected, but resale activity slowed from year ago levels and average prices dipped slightly. The slower resale activity and price decline followed the start of the Bank of Canada’s monetary tightening, but it remains to be seen whether the one month’s data is the start of a weakening trend. Importantly, inflation continued to rise, edging up to 6.8%.

The high level of inflation led the Bank of Canada to follow through on its promise of another 50 basis point rate hike in interest rates, which they delivered as this is being written on June 1st. Market expectations had been for another 50 basis point increase in July, but the Bank’s June 1st statement warned that it was prepared to act more forcefully if inflation did not appear to be slowing.

In issuer news, iA Financial issued an inaugural Limited Recourse Capital Note (LRCN) and used the proceeds for the planned redemption of the IAF.PR.G shares. Provincially regulated by Quebec, rather than by OSFI, iA Financial only recently received permission to issue LRCNs. The new LRCN had an initial coupon rate of 6.611%, which compared with the approximate new rate of 5.70% on the preferred shares. The LRCN coupon interest is tax deductible while the preferred share dividends are not, which made the LRCN somewhat lower in cost to the issuer. However, when the costs of issuing the LRCN and redeeming the preferred shares are included, it does not appear iA Financial gained much in the process.

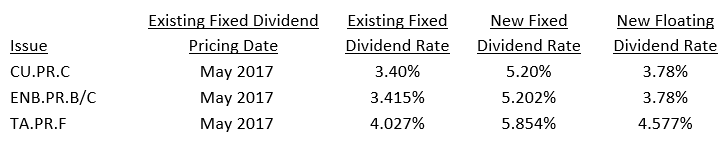

In May, three series of fixed rate preferred shares reset their dividend rates and each raised their respective rate substantially. Details of the resetting issues were as follows:

In each case, there was little interest in switching into the floating rate alternative because 3-month Treasury Bill yields were substantially below 5-year bond yields. Indeed, sufficient numbers of ENB.PR.C holders wanted to make the switch into the fixed rate ENB.PR.B shares that Enbridge announced all of the floating rate shares would be converted into fixed rate ones for the next five years.

Redemptions will continue in June, as three series of preferred shares totaling roughly $650 million have been called by their respective issuers. Details of the issues to be redeemed are as follows:

The Enbridge redemption announcement was completely unexpected by the market, because the ENB.PR.U shares were trading at $22.20 when the news broke; the share price immediately moved above $25.00. The redemption prompted buying of other Enbridge preferred shares as investors speculated about other series being redeemed. The Industrial Alliance redemption was also a surprise as the shares were trading at $24.15 when the announcement occurred. As noted above, Industrial Alliance’s parent company, iA Financial issued a LRCN to fund the IAF.PR.G redemption.

There were no new preferred share issues in May.

The seven largest preferred share ETFs experienced total net withdrawals of $95 million in May. This was the fourth consecutive month that aggregate flows were negative. Only TPRF, which holds common shares in addition to preferred shares, and DXP enjoyed net deposits, albeit rather small ones.

J.Zechner Associates Preferred Share Pooled Fund

The fund returned 4.98% in May, which was in line with the benchmark result. Good security selection during the month was somewhat obscured by Market on Close (MOC) orders on the final day of the month as index funds tried to reinvest the proceeds of the $1 billion redemption on that day. Over 25 issues went into extension, meaning the MOC orders could not be filled with regular liquidity and the prices of those less liquid, somewhat random issues were forced higher following the normal market close.

During the month, we sold the balance of the TD.PF.K shares to bring the TD Bank exposure back below 5%. We believe the TD 5.75% institutional preferred shares offer better value. We also added to the holdings of MIC.PR.A, a perpetual issue, and ENB.PR.N, a rate reset issue, both of which offered good value and attractive yields.

Outlook and Strategy

We were not surprised to see the preferred share market rally as it did in May. For many months we have been mindful that the market has not been appreciating the magnitude of dividend increases that will result from the spike in 5-year bond yields. The Bank of Canada will continue to raise interest rates going forward and the benchmark bond yield (and dividends) will likely rise further from current levels. The preferred share market will also continue to benefit from ongoing redemptions of rate reset series.

Preferred shares are an attractive option for fixed income investors, offering higher yields and low long-term correlation versus the bond market. In addition, the expected future rate increases by the Bank of Canada will likely mean lower bond prices, but even higher preferred share yields. Accordingly, the fund currently holds an overweight allocation in rate reset preferred shares.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.