Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

April 12, 2022

The preferred share market had an up and down month in March, with downturns followed by rebounds. The initial selloff was due to the general uncertainty following Russia’s invasion of Ukraine but concerns about the start of monetary tightening by the Bank of Canada as well as new issue pressure also had negative impacts on the market. Offsetting positive factors included continued preferred share redemptions and a sharp increase in 5-year bond yields that will mean higher dividend rates when issues reset in the future. However, investors appeared to show apathy to higher future dividends with the S&P/TSX Preferred Share index returning -0.27% in the month.

There were three new issues in March. By far the most impactful was the second ever institutional preferred share issue from TD Bank that followed the first such issue by the Royal Bank last fall. Institutional preferred shares are a structure that the Office of the Superintendent of Financial Institutions (OSFI) wants to become prevalent for banks and insurance companies so that retail investors will be precluded from investing in financial institutions. The shares have $1,000 par values, instead of $25.00, a minimum purchase size of $200,000, and pay dividends semi-annually instead of quarterly. In addition, the institutional preferred shares are not listed on any stock exchange, but trade in the over-the-counter bond market instead.

The TD issue had a generous 5.75% dividend rate that allowed the bank to raise $850 million from its institutional investors. The dividend rate was higher than any bond or other preferred share that TD Bank has outstanding and was higher than most other preferred shares as well. As a result, the TD issue put downward pressure on other preferred shares and set a higher bar for subsequent new preferred share issues.

In addition to the TD issue, Intact Financial brought an issue of perpetual shares and Partners Value Split Corp. issued retractable shares. Details of the new issues were as follows:

In March, Canadian economic activity reverted to a more robust footing as both Ontario and Quebec ended their Covid-19 lockdowns. Notwithstanding the lockdowns, GDP growth for January was estimated at 0.2% which set up first quarter GDP to grow at a robust 4% pace. Employment surged in February, with 336,600 new jobs created, leading the unemployment rate to drop a full percentage point to 5.5% from 6.5%. The unemployment rate fell below its pre-pandemic level and the participation rate improved to near pre-pandemic levels. Other good economic news included retail sales, which increased substantially more than expected. Less positively, Canadian inflation continued to increase, reaching 5.7%, its highest level since 1991.

The Bank of Canada finally began raising its interest rates on March 2nd, with a 25 basis point increase. Subsequent comments by Bank officials hinted that future increases may be more aggressive, and the bond market began anticipating increases of 50 basis points at the next two rate setting meetings. Yields of shorter term bonds were especially impacted as investors anticipated the changing trade-off between money market instruments and bonds. The yield of 5-year Canada bonds, the reference for rate reset issues, surged 75 basis points higher in the month. The increase in prospective dividends presumably was supportive for rate reset issues, but there was not an identifiable “Ahh ha!” moment with a commensurate rise in prices.

There were six preferred share redemptions during March. These redemptions totaled $2.2 billion or about 3.5% of the market, and well spread out through the month. They resulted in reinvestment flows that were supportive of other issues, particularly on the redemption dates. However, we were somewhat surprised that the reinvestment activity was not stronger and the lack of more significant reaction may have been due to the geopolitical and inflation distractions during the period.

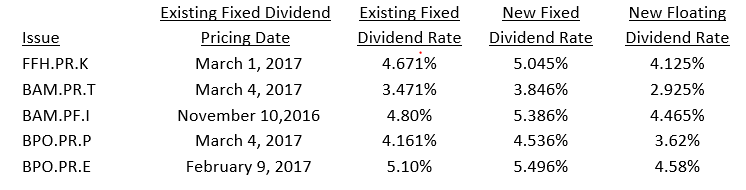

In March, five series of fixed rate preferred shares reset their dividend rates and all noticeably raised the rate. Details of the resetting issues were as follows:

Of note, none of the resetting issues had sufficient interest in the floating rate option and each will remain completely fixed rate for the next five years. The lack of interest in floating rate shares occurred despite the start of rate increases by the Bank of Canada that are expected to push 3-month Treasury Bill yields significantly higher over the next year. Perhaps when 3-month Treasury Bill yields are closer to 5-year Canada bond yields there will be more interest in the floating rate alternatives. Also noteworthy with the resetting activity last month, two of the issues (BPO.PR.E and BAM.PF.I) had dividend floors. To date, most issues with that feature have been redeemed rather than reset, because they also had relatively high reset spreads. Market conditions were clearly not favourable for these issues to be refinanced, however, and their dividends were reset instead.

In issuer news, DBRS upgraded its rating on Financial 15 Split Corp. preferred shares to P-3 from P-3(low). We note that these shares had to extend their termination date from December 2020 to December 2025 because the underlying pool of common shares was unable to support the retraction on the original date. That sort of risk is one of the reasons we do not invest in split share preferred shares.

During March, the six largest preferred share ETFs experienced total net withdrawals of $206 million. This was the second consecutive month that aggregate flows were negative. Only the actively managed DXP and TPRF enjoyed deposits in March. We suspect that profit taking following very strong results in 2021 may be a factor in the withdrawals. As well, geopolitical concerns and the highest inflation rate in 30 years may be distracting investors’ attention from preferred shares.

Zechner Associates Preferred Share Pooled Fund

The fund returned +0.05% in March, which compared favourably with the S&P/TSX Preferred Share index return of -0.27%. The energy related issues in the portfolio, including Cenovus, Pembina Pipeline, Northland Power, and Altagas had particularly good performance in the month.

We believed the new Intact Financial perpetual issue was attractive and we participated in that deal. The subsequent TD Bank institutional preferred share issue was, in our opinion, even more attractive and we added a significant holding of it to the portfolio. Outside of the new issues, activity in the fund was limited during March.

Outlook and Strategy

Given the robust returns in the preferred share market in 2021, it was not surprising that this year began with some consolidation. However, we believe investors have not fully appreciated the benefit that rising bond yields are having on dividend rates. Yields of 5-year Canada bonds have risen approximately 1.15% in the first quarter, which means rate reset preferred shareholders should be anticipating substantially higher dividend rates going forward. We also note that preferred shares have been and continue to offer a good defensive choice for fixed income investors compared with the broad bond market which has declined close to 7.00% to start this year.

Given our positive outlook, we are keeping cash levels relatively low. However, we are being patient in looking for the best yielding opportunities while being mindful of the risk of potential redemptions.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.