Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

July 29, 2021

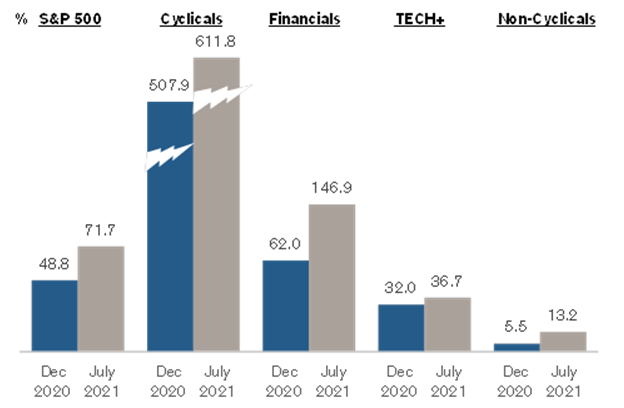

The saving grace for stock investors will be the strength and consistency of the earnings recovery being experienced right now. Stronger pricing power is allowing companies to pass through their cost increases and therefore keep profit margins high. Meanwhile, the continued recovery of the economy is helping companies beat the revenue estimates as well. This has been so clearly apparent in the early reports of second quarter earnings, where over 30% of S&P500’s companies have reported, earnings are beating estimates by an astounding 18%, with 85% of companies topping projections. Expectations were already riding high prior to the releases, with estimates for revenue and earnings growth of 21.2% and 71.7%, respectively. Even before the blowout earnings for tech giants Microsoft, Alphabet and Apple, earnings were on pace for 80% annual gain! Why we continue to favour moving out of the high growth sectors and into the ‘cyclical, value-oriented’ sectors is outlined below. While the technology sector continues to grow at impressive 30%+ rates, the cyclical and financial sectors, which are much more reasonably valued, are see massive triple-digit jumps in year-over-year earnings as they ‘lap’ the very depressed results from the second quarter of 2020.

What worries us right now? Beyond the normal fears about slowing economic growth, record high valuations and extreme bullish sentiment readings, at the top of the list has to be the narrowing of breath, or participation by a larger number of stocks. The fact that the Russell2000 is lagging the S&P500 to such as large degree over the past few months is a bad sign for stocks overall. A real bull market should see a broadening of exposure more indicative of a recovering economy. Maybe this is just a short-term pullback for those ‘value’ sectors of the market. Other research provides yet more evidence that ‘value’ is a good bet to outperform ‘growth’ in coming years. Though the value category on average over the past century has outperformed growth, it has uncharacteristically lagged over the past 15 years. Beginning last fall, value began to reassert its historical dominance. But after a strong run, in the past two months it has begun to lag again. Many are wondering if that means value’s run is now over, or whether this is merely a pause on the way to a sustained period of strong relative performance over growth. Relative valuations of stocks favour those ‘value’ sectors. According to Yardeni Research, the S&P500 Growth Index’s forward P/E ratio is currently 11.7 points higher than that of the S&P 500 Value Index—nearly three times greater than the average differential over the past decade. As parts of the global economy start to catch up with the U.S. and China, we should see broader support for the cyclical stocks. Prices for a few big tech stocks— Facebook, Apple, Amazon, Alphabet and Microsoft—are why the standard, market cap-weighted S&P500 appears so expensive. Those six companies, with a combined market value of $9.4 trillion, account for a quarter of the index’s aggregate value. They have outperformed the index recently, with an average gain of 4.9% in the past month. The S&P500 is up 2.6% over that same time. The bottom line is that investors who are confident in the economy are likely to be able to find value ‘beneath the surface.’

In Canada we continue to find exceptional valuations in the Energy sector, despite some longer-term concerns about the move to renewable resource and away from carbon fuels. Canadian production companies such as Crescent Point, Arc Resources, Suncor, Tourmaline and Cenovus are trading with free cash flow yields in excess of 20% at current oil prices! Canadian banks have also delivered exceptional results in the past few quarters and have amassed substantial capital positions which we expect could be redeployed into share buybacks and/or dividend increases. Basic materials companies are riding a wave of higher commodity prices which are not factored into current stock valuations. Industrial companies and auto parts have been hampered this year by the semi-conductor shortage as well as rising input costs, but most have large order books which will support growth for quarters to come. Consumer spending has been held back primarily by a shortage of the basic goods and services they want to buy. As these shortages ease, growth in this cycle could be extended for longer than many investors currently expect. Risks are always present as mentioned earlier, but we see ourselves early in a new cycle and would prefer to remain invested with a focus on earnings growth, high dividend yields and reasonable valuation support.Still seeing lots of companies that meet that criteria!

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.