Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

January 3, 2025

Being a ‘crypto critic’ is apparently age related! I read some studies lately that showed the largest buyers of crypto-related investments are males in the 18-49 age bracket. That makes sense since it fits with both the longer-term horizon needed to see the full acceptance of crypto as well as the shift in political polling in that age group in the recent U.S. election, where the incoming administration became major crypto supporters. For the older crowd (myself clearly included) we have mostly not bought into the crypto boom. It lacks many of the traditional characteristics of good investments, including a viable business model, some level of income generation and/or a valuation that is in line with other risk investments. Bitcoin has none of that! While one could argue that you could say the same for gold, there is a ‘jewellery demand’ for gold that is real, ongoing and almost equal to global gold production. Central banks have also been major buyers of gold over the past few years as they diversify their reserves away from fiat currencies. While that may also become a source of demand for Bitcoin, we have not yet seen any major central banks indicate they are looking at that option. The key reason to own Bitcoin is the belief that there will be other new buyers to drive the price higher. That is the definition of what creates an investment bubble! The most recent gains in Bitcoin were fueled by ‘U.S. strategic crypto reserve’ chatter as well as the inclusion of Microstrategy, a proxy for buying Bitcoin, in the Nasdaq100 and to the buying of US$325 billion in funds linked to that index. Again, nothing that indicates a growing penetration or acceptance of cryptocurrencies in fintech or other applications, but only a new set of financial buyers to push the bubble further!

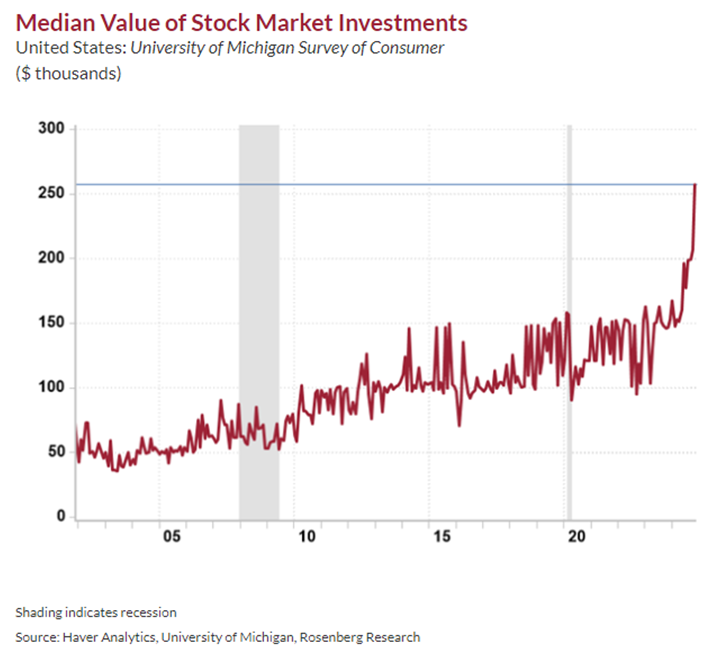

We have often referenced the ‘wealth effect’ and how it has been one of the biggest sources of support for the ongoing strength in consumer spending, especially in the U.S. But what is the ‘wealth effect?’ Here is a visual shot of why American investors have been on a ‘wealth-induced’ spending spree which has helped to sustain economic growth while economies over the rest of the globe stumble. The median value of stock market investments of U.S. households has soared by over 150% since the pandemic lows to over US$250k, more than double the gains seen over the prior 20 years!

Clearly the sharp gains in stock portfolios has buoyed spending even as employment growth slows, interest rates stay higher than expected, overseas economies stumble and geo-political risks increase. The problem with this is that just as economic growth becomes tied to the performance of the stock market on the upside, the same will be true on the inevitable downside when it occurs. Which meams that any stock market correction could quickly turn into an economic risk as well. Another good reason to have a healthy position in long-term bonds as a hedge against stock market risk.

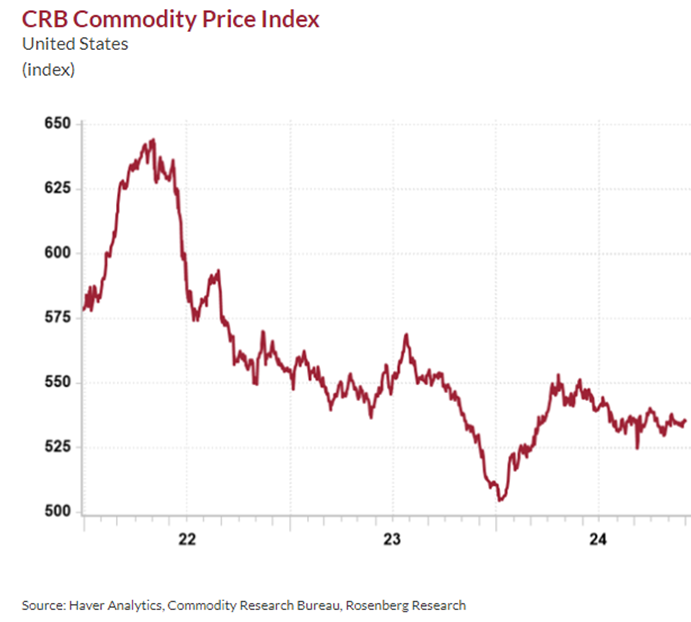

In terms of looking for asset classes that have lagged and may represent a good risk-reward trade-off, one sector that has not kept pace with the boom in risk assets has been in the commodities space. The sputtering European and Canadian economies, lingering weakness in China and other emerging markets and Japan’s mixed macro performance have all combined to undermine the pro-cyclical commodities asset class that has lagged the overall financial markets over the past three years. Geo-political risks still exist for the supply side of most key commodites (particularly energy and agriculturals) such that supply squeezes could occur at any time. Meanwhile, most of the rest of the world economy turned down in 2022 and lagged the ‘mighty U.S.’ since then. Given that those ‘non-U.S.’ economies are also the largest consumers of commodities, the demand side of this equation could improve if those economies start to come out of their prolonged downturns irrespective of what happens in the ‘wealth effect and tech driven’ U.S. economy.

Given that commodity stock valuations are at multi-decade lows, this also means a better risk-reward ratio for investments in those stocks and sectors. We recently added to names in the agricultural sector (Nutiren), copper stocks (Teck Resources and HudBay Minerals) and Canadian energy stocks (Baytex, Cenovus, Freehold Royalties and Veren Inc). These stocks are also a good hedge against any potential weakness in the U.S. dollar if the bullish growth forecasts or higher interest rates fail to meet expectations. The commentary and consensus have all been in the other direction over the past year as investors shifted from bullishness over the rollout of artifical intelligence to bullishness over the potenitally stimulative impact of the economic policies of the new Trump agenda. Commodity markets have already dealt with the severe headwinds of a strong U.S. dollar and would be a major benefiary of any reversal in that recent trend.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.