Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

February 2, 2017

Some analysts estimate it needs to retain a minimum of $2.6 trillion to $2.8 trillion under the International Monetary Fund’s (IMF’s) adequacy measures. If pressure on the yuan persists, analysts suspect China will continue to tighten the screws on outflows via administrative and regulatory means. But if it continues to burn through reserves at a rapid rate, some strategists believe China’s leaders may have little choice but to sanction another big “one-off” devaluation like that in 2015, which would likely roil global financial markets and stoke tensions with the Trump administration. The yuan depreciated 6.6 percent against the surging dollar in 2016, its biggest one-year loss since 1994, and is expected to weaken further this year if the dollar’s rally has legs. Adding to the pressure, Trump has vowed to label China a ‘currency manipulator’ and has threatened to slap huge tariffs on imports of Chinese goods.

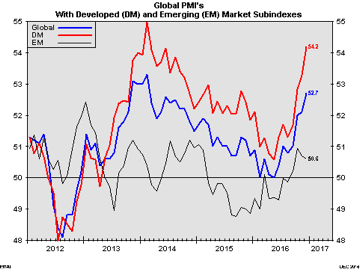

So why do stock prices continue to head higher, particularly in the U.S? Stock market optimism has been supported to some degree by the recent improvement in global growth trends. Growth exceeded expectations in many regions outside of the U.S. in the 2nd half of 2016, with the Citi Global Economic Surprise Index showing its sharpest rebound since 2013. Global manufacturing indices (PMI’s) have also turned higher, as shown in the chart below. While these are still ‘survey based indicators’ and therefore subject to ‘sentiment bias’, they have clearly shown their strongest rebound in about four years. While this could be a positive data point for corporate earnings going forward, we are still somewhat skeptical since the emerging trade conflicts and currency volatility could quickly take the momentum out of these indicators. Retail sales data in the U.S. was weak in December and fourth quarter growth was well below expectations. The new administration in the U.S. has gotten a brief ‘honeymoon period, where most investors are giving them the benefit of the doubt on their plans to grow the economy. But more incidents like the recent ‘immigration ban’ or the clashes over the border tax and the wall with Mexico are all going to push back against this optimism.

After many false promises, it is becoming evident that 2017 will be the year the Federal Reserve finally begins down the road towards ‘interest rate normalization’. Assuming that we don’t have some ‘growth accident’, short-term bond yields should rise this year. In addition, this stronger economic growth, higher inflation, soaring debt and deficits, along with the lack of central bank bond-buying, should send long-term rates much higher as well. Our continued concern, though, is that Wall Street soothsayers, who viewed every Fed rate cut as a buying opportunity for stocks, are now assuring investors that the potential dramatic and protracted move higher in bond yields will be bullish for stocks as well. We take issue with that view, given that the low (and even negative) interest rate scenario had been the prime reason for the rise in stocks over the past few years. Have we so quickly forgotten the TINA (‘There is no Alternative’) rationale for the out-performance of stocks?

Another interesting point is that the bulk of the gains in stock prices over the past five years have accrued to investors in U.S. stocks. The chart below shows the performance of the S&P500 Index versus the MSCI All-World Index from the bottom in 2009. The strength of the U.S. dollar, the better economic performance and the viewed ‘safety’ of U.S. assets all contributed to the better relative performance. However it has also lead to a distortion in valuations. European, Asian and Emerging Economy stock indices are all trading at significant discounts to the valuation of U.S. stocks. As growth starts to pick up outside of the U.S. (driven to some degree by the weakness in those foreign currencies) we should see a moderation in central bank support as well as a relative improvement in stock market performance.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.