Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

January 4, 2026

The path of interest rates in 2026 is far from clear. Optimism over easier money policies has also been one of the fuels for continued stock market advances in 2025. The Fed eased some worries in December by cutting rates as expected, but the path going forward is not clear. The just-released Minutes of the most recent Federal Reserve meeting highlighted those crosscurrents and the reasons why 3 voters on the board dissented with the decision. “With respect to the extent and timing of additional adjustments to the target range for the federal funds rate, some participants suggested that, under their economic outlooks, it would likely be appropriate to keep the target range unchanged for some time after a lowering of the range at this meeting,” the minutes said.

Officials expressed confidence that the economy would continue to expand around a “moderate” pace, while they saw downside risks to employment and upside risks to inflation. The extent of the two dynamics divided FOMC policymakers, with indications that the vote could have gone either way despite the six-vote victory for the cut. Core inflation remains sticky and elevated at levels well above the 2% targets. We finally got some delayed economic data and the inflation rate in the U.S. did show an unexpected decline to an annual rate of 2.7%, but the data was met with scepticism since there were many omissions of standard metrices. On the other side of the dual mandate, the employment data has clearly been weakening but the numbers are also muddied by delayed releases in the U.S., tighter immigration laws which have limited the growth of labour supply and the impact of artificial intelligence on reducing long-term levels of employment. How the central banks navigate all of this in 2026 will be muddied further by the appointment of a new head of the Federal Reserve before the May meeting. Whoever that person is, they will clearly be a Trump acolyte and be pushing for sharply lower interest rates. The big problem for markets is that excessive monetary ease would end up being a worry for both the stock and bonds, since easier financial conditions will lead to inflation rising again even though it had yet to reach its 2% target. This is the message that the bond market is telling since we have seen long-term interest rates unchanged over the past year even as short-term rates have dropped by 175 basis points! More importantly, if housing is the sector that is most in need of recovery, then this focus on short-term rates is counter-productive since mortgage rates are tied more closely to the level of long-term rates. That is the story we are getting from sectors of the stock market such as the home builders, Home Depot and the price of lumber. Interest rates are no longer falling in other major OECD countries such as Great Britain and Japan as well as the EU and Canada. If the U.S. is the only country continuing to cut interest rates, that will put more downward pressure on the U.S. dollar and probably levitate the gold market even further.

There are more dividend investors than we may have thought. Disappointing dividend announcements have been piling up, just five years after a rash of high-profile Canadian companies slashed their payouts during the early stages of the COVID-19 pandemic. While dividend cuts – or a pause on increases – can be disappointing, especially for those counting on the income, they can bring a sense of relief, too. Some investors may welcome the greater financial flexibility it gives the companies and see more opportunities for growth. Telecom giant, Telus, gained 2.1% after announcing they will cease for now raising their dividend annually and will instead keep it at the same level. The stock had sold off on worries and reports that they may be cutting their dividend so this was more of a ‘relief rally’. Telus investors had noted the extremely negative stock reactions when BCE cut their dividend earlier this year (as expected) as well as the 35% drop in the price of Northland Power when they surprised investors last month with a 40% dividend cut to have more funds available to finance some new growth projects. Allied Properties slashed its monthly distribution by 60% to focus on debt repayment, marking a major reversal for management after telling investors in August they were “very comfortable” with the monthly payout. The stock dropped 20% when rumours started circulating about the risk of a cut and then fell a further 30% when the actual announcement came. The biggest revelation from the stock action following all these dividend announcements, in our view, is that there are far more investors in the market that are very dependent on the flow of dividends from these companies for income than investors who are willing to let management have more cash available to fund future growth or improve their balance sheets. We have seen some companies continue to pay existing dividends even when the amounts needed to fund these dividends exceeded their annual profits (Enbridge a few years ago comes to mind) to placate investors. But paying dividends from the firm’s capital is neither a good nor sustainable strategy so investors need to be wary of what the payout ratios are for most dividend payers and what the risks are to the sustainability of those dividend levels.

Canadian fourth quarter bank earnings were exceptional, low-drama quarter, providing investors with a full slate of earnings beats and guidance that was better than expectations. While management teams remained somewhat cautious around the geopolitical environment heading into 2026, the current set-up positions the banks to generate growth, primarily supported by continued momentum in Capital Markets and Wealth. In combination with modest net interest margin improvements and prudent cost containment, strength in these sectors should help offset flattish loan losses and muted loan activity. While the banks are certainly expensive versus historical levels, a constructive view is supported by earnings growth and considerable capital positions. Beats across the board in the 4th quarter were driven mostly by strength in capital markets activities and wealth management, which should come as no surprise given, we have been in a bull market. Loan loss provisions were kept relatively flat, which was somewhat of a surprise given some of the weak segments of the economy we have seen due to the ongoing trade frictions. Capital levels remain exceptionally strong, and buybacks will stay in place for all the banks. RBC was a particularly strong beat as they also improved their cost structure, raised their dividend and laid out a stronger long-term ROE forecast. The bar was set very high for the banks though and valuations are close to record levels, which is why we are seeing only a muted response on the stocks RBC and National still have upside from their recent acquisitions of HSBC Canada and CWB, respectively. National also added assets from Laurentian Bank buyout. But outside of that, growth opportunities are limited. Most recent forays into the US (which included TD Bank failing to buy Horizon, Bank of Montreal buying Bank of the West and Royal buying Citi National) have all caused more headaches than gains initially and we don’t necessarily see more opportunities there. There are no more smaller players to absorb in Canada and competition is starting to come from more online players in the business. We expect that this will become the avenue of growth for the banks going forward, but it remains to be seen whether they will try to do it organically or acquire the leading firms (i.e. Wealth Simple). Given record valuations and limited growth opportunities we remain underweight the bank sector.

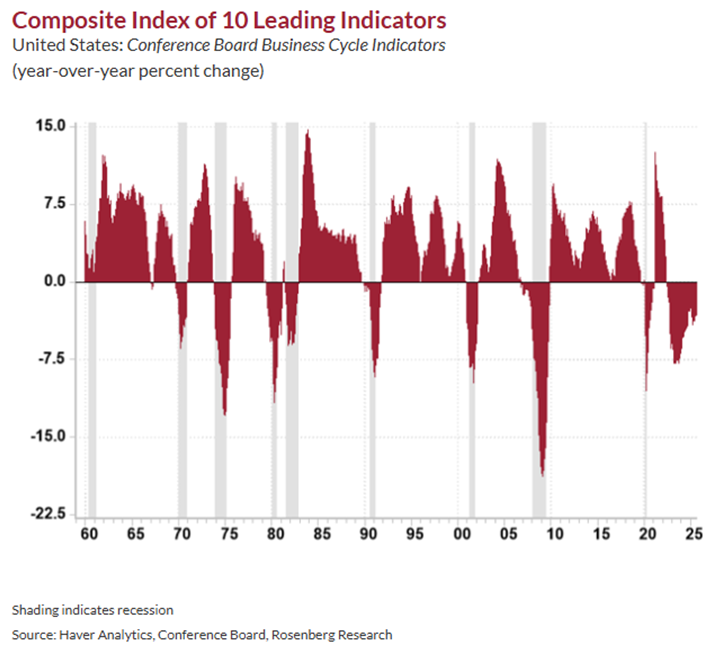

Has the Index of Leading Economic Indicators lost its predictive value? There was a time when the Conference Board’s index of leading economic indicators was a closely watched metric but having made the recession call in 2022, nobody pays much attention to it anymore. The year-over-year trend has been ensconced in negative territory every month since July 2022 (-3.3% presently), and that duration has never occurred outside of an outright recession. The diffusion index was 45% after coming in at 40% in August, so this is the second month running where over half the components were subtracting from growth. The index is made up of indicators such as average weekly hours in manufacturing, average weekly initial claims for unemployment insurance, manufacturers’ new orders, nondefense capital goods excluding aircraft orders, building permits and stock prices, all of which reflects investors’ expectations for the future health of the economy. These components are combined to provide an aggregated signal intended to predict turning points in the U.S. business cycle, typically spanning six to nine months into the future.

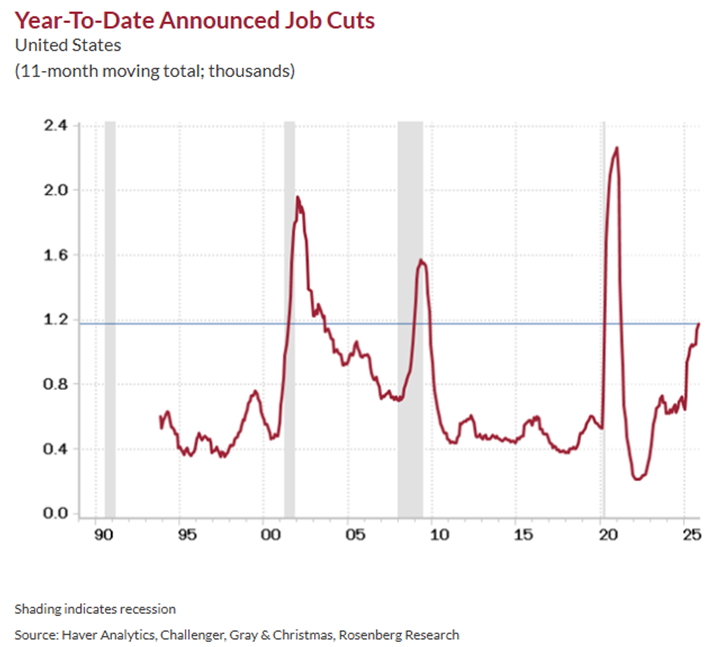

Third quarter GDP numbers in the U.S. were quite strong, extending the resilience of growth beyond what many would have expected even earlier this year. But looking deeper into the numbers, it seems like only the headline is the good news as growth came from a very narrow base. Three-quarters of the U.S. economy experienced no growth in the third quarter. The only reasons for the +4.3% headline were due to lower imports, government expansion, the ongoing AI buildout, and continued spending from high-end consumers, which were running down their savings rate dramatically while feeling empowered by the ‘wealth effect’ from rising stock markets Through the first eleven months of 2025, there have been 1.2 million job cut announcements, more than double the near 500k in hiring plans. This is a similar number we had on our hands over the same time frame in April 2020, December 2008, and July 2001, which were all pre-recession periods. But the impact from the explosion of AI on jobs should not be underestimated. Challenger hiring data showed that in the six months to November, there have been 54,694 layoff notices due to AI implementation. Another 66,866 were from “cost-cutting,” which is indirectly related to the same thing. We believe it will ultimately be a deflationary force as it improves productivity and corporate profits but slows down or even reduces employment levels. The increase in job cuts in 2025 was initially believed to be due solely to the apprehension over the fallout from the aggressive tariff increases. But as those impacts seem to have moderated, job cuts have continued.

How to mould all of these economic crosscurrents into a cohesive investment strategy for 2026 is not straight-forward. Given all the elevated risks we described throughout this commentary, we have made few changes to our overall strategy or defensive portfolio positioning but have maintained stock exposure around the 50% level with ongoing strong weights in the technology, telecom, energy infrastructure and U.S. health care sectors. In tech world, we note that some prior laggards are starting to look like better bets to us on both a valuation and growth basis as well as being contrarian views. After a disappointing year for software stocks, Salesforce (CRM-US), snapped back after releasing earnings ahead of expectations and making some positive comments about the outlook for growth at their Investors’ Day. Another software laggard, Adobe, report better-than-expected financial results as demand for its artificial-intelligence products grows. The stock rallied a bit post that release and comments from the CEO that “Adobe’s record FY2025 results reflect our growing importance in the global AI ecosystem and the rapid adoption of our AI-driven tools”. The stock is now trading at only about 16 times current earnings, a significant discount to the overall market for a company still growing revenues at over a 10% annual rate. Perrenial software winner in Canada, Constellation Software, also stumbled mightily in 2025 but is now looking like pretty good value for the ongoing acquisiton-oriented company. Maybe the rumours of the death of enterprise software were premature. We have added to all three names in our tech holdings as well as a few giants that are trading at earnings multiples below the entire market, namely Amazon, Meta and Alphabet.

A few other names we have added to recently include Sprott Physical Uranium Trust. If the nuclear expansion and energy shortage stories around AI are true then uranium prices are going to need to go a lot higher than the current level of around US$80 per pound. This trust holds physical uranium and is the only ‘pure play’ on the commodity. Almost everything else around this trade have surged in the past year (i.e. Cameco, Constellation Energy, the engineering and electric utilities building this capacity) but the actual price of uranium is actually flat on the year. We also added to Torex Gold while slightly reducing overall exposure to that sector given the strong gains of the past year. But we note that Torex trades at a significant discount to the rest of the sector due the winding down of production at their largest mine, the El Limon open pit on the Morales property in Mexico, which we view as a relatively safe geo-political risk region. However, in the past year they have also almost seamlessly migrated that production to the Media Luna deposit at the south end of the same property. Meanwhile they have expanded the reserves at El Limon by going underground at that mine with a higher grade that will also yield about 30% copper output. Overall mine life has expanded to the mid 2030s and the company is once again on the verge of generating free cash flow and yet continues to trade at a discount to the group on both a net asset and cash flow basis.

We also still like bonds, particularly in the U.S., as a hedge against any weakness in the stock market or overall economic risks. U.S. rates are still expected to fall in 2026 and long-term yields are above 4.8% so we can see good income and well as potential capital appreciation. This investment is not without risks of course and we have outlined some of the risks around U.S. monetary policy and the expected change in the head of the Federal Reserve to someone who will most likely be a ‘Trump acolyte’ and an advocate for extremely sharp interest rate cuts. This could lead to higher long-term rates but the new chief still has only one vote and would need to get the rest of the committee on board for cuts that would raise inflation risks. In a world where cash is not generating returns in excess of inflation, where stocks have both economic and valuation risks and private market investments are illiquid and richly valued, there is still a good argument for keeping a more balanced portfolio with a 35-40% weight in the bond market.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.