Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

January 4, 2026

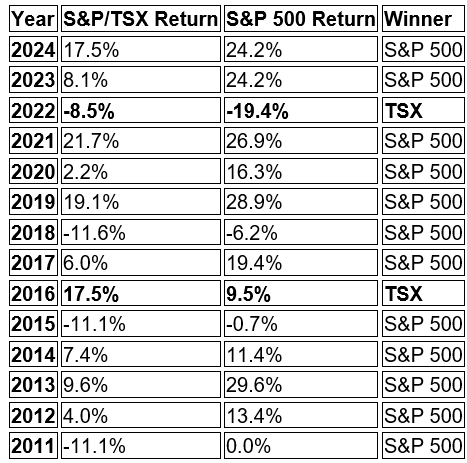

For only the third time in the past 15 years we saw Canada’s TSX Index generate a higher annual return than the U.S. S&P500 Index in 2025. Going into the last trading day of the year, the TSX is sporting a gain of over 28% while the S&P500 is ahead by about 18%. Headlining the Canadian market’s outperformance in the past year was a rise of over 90% in the Basic Materials sector, which is mostly the gold stocks. In fact, the gold stocks alone accounted for over 1/3 of the overall market gain in the past year despite having just a 12% weight in the index. Although the AI (artificial intelligence) craze continued in the U.S. and most global markets, the price gains for most of the big names were much more muted in 2025 as excessive valuations and some growing trepidation about both the sustainability and constitution of that sector’s growth was brought into question. Despite the market weakness and economic angst early in the year about the impact of the Trump tariffs, the reality has proved less dire (thus far) as many threatened reciprocal tariffs were rescinded, some of the Liberation Day tariff levels were reduced and companies have initially absorbed the cost increases. But the full economic impacts have yet to fully flow through and there were some offsets as the continued massive spending on AI infrastructure as well as increased government fiscal spending blunted the negative influences. U.S. markets have so far remained astonishingly dominant. Since the 2008-09 global financial crisis, U.S. equities have outperformed the rest of the world’s markets by 7% annually, compounded. They have also dominated the largest companies with about two-thirds of global listed equity market capitalization residing in the U.S. The past year shows that trend might be on the verge of changing. European, Asian and emerging markets all had higher returns than the U.S. in 2025.

Year-by-Year Comparison (Price Return)

There have been two key reasons for U.S. market dominance since the Financial Crisis in 2008. The first is technology, where the U.S. has become synonymous with the most transformative technologies of our time. That includes not only AI, but also cloud computing, semiconductors, and platform businesses that scale globally. The second is quieter but equally powerful. The U.S. has a history of predictable, enforceable, and fairly administered rules and regulations. That is manifest in the openness of U.S. capital markets, the depth of its exchanges, and the strength of its legal system. But the volatile policies of the second Trump administration have raised the question of what happens when those rules, regulations, and the institutions underlying them start to wobble? This past year offered a preview. Following ‘Liberation Day’ tariff announcements from the Trump administration in early April, U.S. markets experienced a “triple red” moment: simultaneous major drawdowns in equities, bonds, and the dollar. The last time these three indicators all flashed red for a prolonged period was in the 1970s, when U.S. institutions were dealing with economic instability, political turmoil, and oil shocks. The other threat to U.S. dominance is the drift toward fiscal dominance, in which the government copes with too much debt by bending monetary policy to serve fiscal needs. The U.S. debt burden is real. The federal government’s interest payments on its debt now exceed its defence spending for the first time. Ferguson’s Law, named for historian Niall Ferguson, said that any great power that spends more on servicing debt than on defence risks ceasing to be a great power. U.S. debt is expected to be a smidgen below 100%, with a deficit on course to be one of the biggest in the developed world at more than 7%. What has saved American finance thus far is the dollar’s status as the must-have global asset and trading currency. But there are four overlapping threats to the dollar: supply, China, reserve safety and the pushing away of allies. Supply is the big one, as the U.S. runs near-record peacetime deficits on top of a bulging current-account deficit. America must attract a constant flow of foreign capital to finance government and imports, which puts it in a less stable position. Both roles face challenges, though, and the more the U.S. exploits foreigners, the higher the risk they look elsewhere. Gold has been the prime beneficiary of this diversification and there is no reason it will end anytime soon despite the sharp rise in the price over the past year.

If Nvidia is this cycle’s coalmine, is Oracle the canary in it? Tech stocks in the U.S. have had a tremendous three year run from their November 2022 lows, driven in large part by excitement over the large language models powering the AI revolution. But this trade has stumbled a bit, particularly in the past few months. The capex binge is now being financed increasingly in the debt market, and concerns are mounting over the systemic risk involved in all the tied selling and entangled relationships. The stakes are larger than they have ever been! Nvidia, Amazon, Google, Meta, Microsoft and Apple alone are collectively valued at more than $25 trillion, or 150% of the entire market cap for the S&P500 at the bubble peak in early 2000. We are starting to see some cracks. While the big software companies such as Salesforce, Workday, Adobe and Service Now have been laggards all year, the mega cap tech stocks such as Amazon, Microsoft and Meta have also pulled back from their highs and trail the overall index. Worries about the ‘circular financing’ and negative free cash flow for these major players has become a key issue. A once-obscure footnote disclosure called “remaining performance obligations,” or RPOs, has become one of the most closely watched numbers for investors in AI-themed stocks, especially Oracle. It is also a lot squishier than investors may realize, helping to explain the sharp fall in Oracle’s stock. RPOs represent contracted sales that have yet to be recognized as revenue. In other words, management believes the sales are probable, not definite. Oracle’s stock soared in early September, at one point jumping 36% in a single day, after a bombshell earnings report in which it said its RPOs had more than tripled since the previous quarter to $455 billion. Since then, Oracle’s RPOs have jumped to $523 billion, or about nine times Oracle’s revenue for the past four quarters. Yet the stock has cratered, down over 40% from its all-time high on Sept. 10. Investors have grown uneasy about the circular nature of many of the AI sector’s dealings and are looking askance at huge gains in RPOs, particularly OpenAI’s ability to meet gargantuan future commitments. It is widely known that about $300 billion of the increase in RPOs at Oracle was due to a five-year contract with OpenAI to supply computing capacity. We expect the AI trade to receive more scrutiny in 2026, much like the free cash flow worries over the past few months. Monetization of AI will have to be visible at some point. Up to now we have not seen it. Anecdotal data indicate over 800 million users of Open AI’s ChatGPT but only 10 million users are paying for that service! That sounds a lot like the ‘eyeballs’ data metric that preceded the bursting of the 2000 ‘tech bubble!’

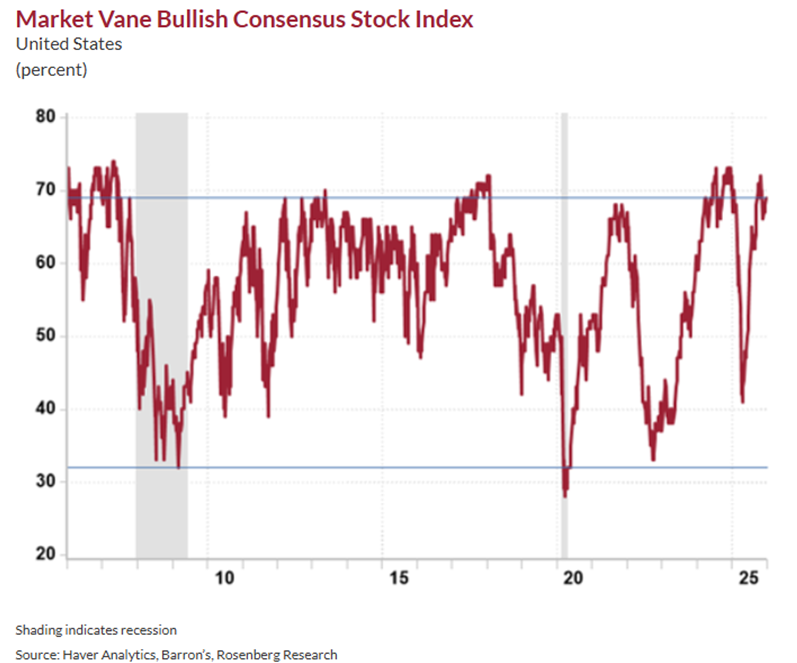

Risk assets are generally having some shakier moments, with the breakdown in Bitcoin over the past few months being the clearest indicator that investors are getting a little less risk tolerant. Bitcoin had sailed to an all-time high of about $126,000 in early October, fuelled by a more favourable regulatory environment. But then a series of record liquidations of highly leveraged crypto positions rocked investors’ confidence in the risk-on asset. As traders rotated out of more volatile assets amid economic uncertainty, the cryptocurrency’s gains for the year were wiped out. Luckily for investors, other sectors have begun to take the mantle and lead the gains to keep stock indices still close to record highs. Financial stocks have certainly been exceptionally strong during the fourth quarter, and we have also seen a recovery in the industrial sector, base metals, retailers and transportation stocks. Bullish investors highlight this increased breadth of gains as a very good sign for sustaining the overall bull market, but we are more cautious, noting that economic weakness and the ongoing impact of tariffs could undermine earnings growth in these other groups and put those recent gains at risk. Tariffs seem to have been dismissed as a major economic risk after the rollbacks by the Trump administration, but investors should recognize that the effective U.S. tariff rate on imports at the end of last year was only around 2.5% and is now nearly 17%, the highest since 1935. But investor sentiment is ‘all in’ for a bullish 2026. Money managers are set to ring in the new year with resounding confidence about everything from economic growth to equities and commodities, according to a monthly poll by Bank of America. Investor sentiment as measured by cash levels, stock allocation and global growth expectations rose to 7.9 in December on a scale capped at 10, the most bullish survey outcome in four-and-a-half years. Combined exposure to equities and commodities — assets that typically perform well when the economy is expanding — hit the highest since February 2022, just before a Covid-driven inflation shock led to a sharp rise in global interest rates. Meanwhile, Market Vane bullish sentiment, pressing against 70%, is near the very high end of the historical band. It seems that almost everybody is ‘all in’ as we move into 2026, except for stalwarts Warren Buffett, who is sitting on cash, and JPMorgan CEO Jamie Dimon, who is buying bonds.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.