Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

April 5, 2019

But much of the recovery in stock prices in the first quarter has been ‘technically driven’ money flows. After getting to extreme lows in investor confidence and equity holdings last December, money had to flow back to stocks just to return to normal levels. Pension fund re-balancing alone was responsible for about $80 billion in first quarter buying while ETF flows from the public also accelerated as stock prices rose, with March flows totalling over US$40 billion. But as we entered the last week of the month, most of the corporate buybacks went into a ‘blackout period’ in front of first quarter earnings which prevented them from engaging in buybacks, which had been responsible for a record US$808 billion in buying during 2018. ETF flows also went negative last week for the first time since last October. That might explain some of the market weakness late in the month.

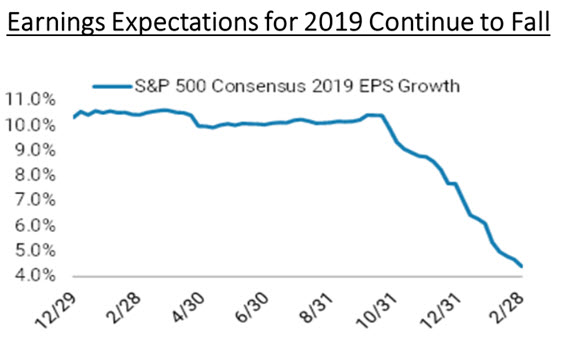

Slowing global growth is also leading to downward earnings revisions, with first quarter earnings now expected to show negative year-over-year growth for the first time since 2015. Tech companies are bracing investors for what could be the worst quarter from a revenue perspective in more than six years. With first-quarter earnings season just a few weeks away, information technology firms have been revising their forward guidance considerably lower. So far, 31 companies have issued negative revenue guidance, which is well above the five-year average of 20 and the highest level since the 36 that did so in the fourth quarter of 2012, according to FactSet. The revised expectations come against a generally dismal backdrop for corporate profits. S&P500 companies collectively are now expected to show a 3.7% decline in earnings per share. Investors haven’t been too concerned about the declining outlook though so it will be interesting to see how markets react as these earnings are released.

While a more dovish U.S. Fed has supported stocks on the belief that it would lead to a recovery in the back half of this year, we have been surprised by the sharp reversal towards optimism. We have been on many conference calls in the past quarter where a weak first quarter outlook was ignored as the companies indicated they would still hit year-end targets, but it would be “back-end loaded!” stocks such as Micron, Intel, Texas Instrument and Samsung have rallied despite sombre outlooks. No doubt investors are seeing the stock market glass as ‘half full’ as opposed to the alternative.

Chipmakers are enjoying their best ever start to a year despite lingering concerns about slowing economic growth. The VanEck Vectors Semiconductor ETF (SMH) has gained over 20% so far this year, the best first-quarter performance since its inception in 2000. That surge outpaces the broader S&P 500′s 12% rally. But this rally is coming despite a clear slowdown in growth in this sector. Earnings announcements from industry heavyweights Micron, Samsung, Intel and Texas Instruments all pointed out sector weakness in 2019, but also held out the olive branch of a recovery in the back half of the year. Investors are clearly buying into this second half optimism. But, as shown below, the data are not supporting the bullish view. While manufacturing growth (blue line) has slowed down, the downshift in shipments (orange line) has been much more pronounced, suggesting that actual results in the sector will fall short of stock market expectations. Buyer beware!

Tough month for Canada’s outlook. Canada continues to face a wide variety of concerns that have caused our stocks to lag other global markets, our currency to come under pressure and our bond yields to fall more than those in the U.S. Fourth quarter GDP was substantially below expectations: in at just +1.6% annualised rate, well below the Bank of Canada’s projection. The breakdown paints a rather subdued picture of the economy with consumer spending slowing to 1.1%, the slowest pace in almost four years and investment falling by nearly 10%, with residential investment and business investment both contracting. The Bank of Canada will have little choice but to wait and hope for a projected growth rebound in the second quarter. Headlines picked up no this theme and were full of sour views on Canada’s prospects. To highlight just a few of the veritable “Sell Canada” stories:

• A strategist at one of the world’s largest asset managers predicted that the Canadian dollar will return to all-time lows of around 62 cents (last seen in early 2002), citing the lack of a growth driver with an over-extended consumer.

• Fitch Ratings chimed in that even Canada’s fiscal position may no longer be worthy of its gold-plated reputation (which includes a triple-A rating for the federal government), given overall public sector debt levels.

• A hedge fund investor who called the top in the U.S. housing sector in 2007 and made famous by the movie The Big Short, took a similar line of reasoning on Canada, saying that housing had seen its best days and predicting that the domestic banking sector could be challenged as well.

Bottom line, don’t expect any interest rate hikes in Canada this year.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.