Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

August 4, 2020

This division between the haves and have nots we referred to earlier is not limited to stock market sectors. It’s also very evident in the rest of the economy where we have seen some improvements in economic conditions in the technology sector and online services but when we look at the overall job picture, it continues to be horrific.

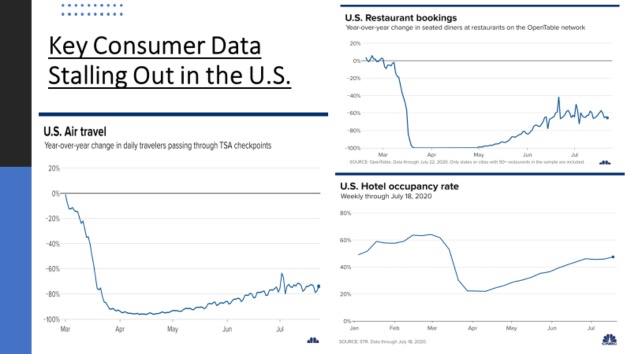

It’s becoming clear now that what policy makers hoped would be a V-shaped recovery has transitioned into a fitful period of starts and stops. Tentative steps toward reopening the North American and European economies have run up against regionalized outbreaks of COVID-19, leading governments in some European countries and U.S. states to impose renewed lockdown measures. Where businesses have reopened, continuing fear of the coronavirus has kept many customers away from restaurants and shops, while major swaths of the economy continue to operate far below pre-pandemic capacity levels. After an uptick in June, U.S. hotel and airline reservations are falling again, plunging the travel and hospitality sector into an even deeper crisis. The charts below show how the recovery in key sectors has stumbled and how deceptive this data can be made to appear. While many pundits cheered in early June that a recovery was gaining momentum with restaurant bookings and air travel each up over 100% from the March-April levels, but the reality is that those data points still remain 60% and 80%, respectively, below year-ago levels. Adding to the woes, they have also appeared to stall out as these low levels. We are still a very long way away from anything resembling a ‘robust recovery!’

The story in Canada is pretty much the same economically in the U.S. despite our much better record in battling the virus. The Canada-U.S. border has been closed to non-essential travel for four months. Real monthly GDP rose 4.5% in May, offsetting 20% of the decline in March and April combined, as provinces began to reopen. In level terms, real monthly GDP remains extraordinarily depressed, 15% down from the peak and close to the levels seen in early 2012. While we expect another strong rise in June, we will likely see much slower. but positive, growth rates after that as later phases of the re-openings kick in. Financial markets here will also need to see some signal from Ottawa that it has a plan for reducing the federal debt, which is set to hit $1-trillion this year, or nearly 50% of gross domestic product. Combined with rising provincial debt levels, it would not be surprising to see Canada’s total net debt-to-GDP ratio surpass 100%, within the next couple of years, something not seen in the past eighty years. While we see lots of economic and financial market risks ahead and have tried to point many of them out, we also recognize that central banks will remains supportive of financial markets and that we have probably already passed the worse part of the economic damage from this crisis. Those facts alone give us some comfort in maintaining an exposure to stocks, preferred shares and corporate bonds. But we also do not see this as a time to be taking extraordinary risks on the growth outlook or stock market valuations and have positioned our managed funds accordingly.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.