Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jacqueline Ricci

April 22, 2022

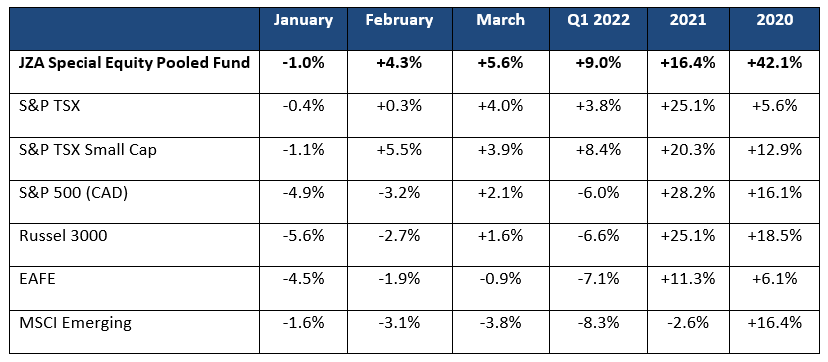

Volatility was the roadmap for the financial markets during the first quarter of 2022. Global stocks on average were weak, but unlike past periods of stock weakness, bonds did not provide an offsetting hedge. Inflation is no longer considered transitory and the prospect of global central banks increasing rates higher/faster, led bonds to suffer one of their worst quarters in the last 25 years. Canadian stocks however bucked the negative trend driven by the strength in the resource sectors. The strength was a result of rising global inflation and heightened concern of supply disruptions from the Ukraine/Russian war. The higher resource sector weighting in the S&P/TSX Small Cap Index led to it enjoying one of the strongest global returns in the first quarter.

The fund outperformed the S&P/TSXSC index by 0.6%, with a quarterly return of 9.0%. The outperformance was in large part due to the overweight in the resource/cyclical sectors. The Canadian Small Cap energy sector was the winner in the quarter with a +36.6% return, followed by the Material sector at +7.3%. Again, the strength in materials was largely from the base metals with golds continuing to lag. The strength in the resource sectors came despite the strength in the DXY which closed out the quarter up +5.4%.

The weakest sectors last quarter were Information Technology (-9.3%), Consumer Discretionary (-7.5%) and Consumer Staples (-6.8%). These sectors have relatively high valuations and tend to be heavily impacted by higher interest rates which drag down their elevated multiples.

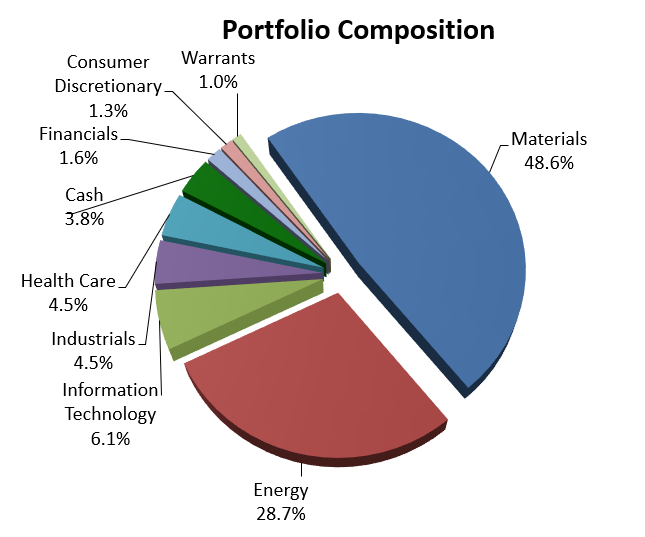

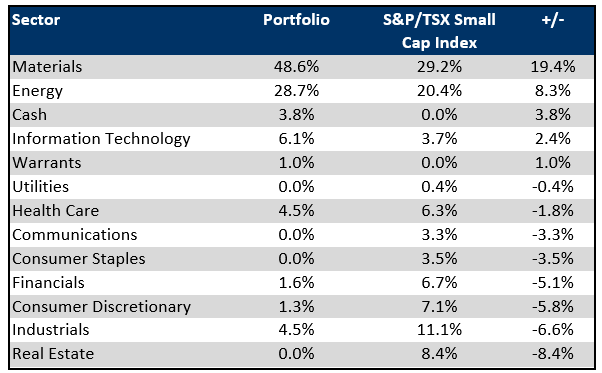

Below are the portfolio and index sector positions as of March 31, 2022:

The three names adding the greatest value to the fund for the quarter were Reunion Gold, Crew Energy and Spartan Delta. Collectively these three names added +3.1.

Reunion Gold is a gold exploration and development company with multiple properties in the Guiana Shield in South America with some of the properties having a strategic alliance with Barrick Gold. The countries of Guyana, Suriname and French Guiana all contain large greenstone belts that are highly prospective. The area already hosts large world class orogenic gold deposits but is still largely underexplored. The management team of Reunion Gold has significant experience is this region with many team members having 25+ years of experience in the area and an excellent track record of discovery. The stocks outperformance in the quarter is largely on the back of the drilling on Oko West which has outlined a high-grade gold mineralization of over 2.5 km strike length and as deep as 350 m. A maiden resource is planned for the third quarter 2022. The fund recently took some profits in the name but continues to hold a core position.

It should be no surprise that the other two names adding significantly to performance in the quarter were energy names. Crew Energy is a natural gas weighted producer that is focused on sustainable growth within the Montney region in northeast BC. Their liquids-rich gas areas of Septimus, West Septimus and Groundbirch offer significant development potential to grow production, reserves, and cash flow over the long-term. This quarter Leucrotta Exploration was acquired by Vermillion Energy for their Montney Resource. This transaction has focused investors attention to Crew’s significant undervalued land base in the region. The fund continues to hold the position in Crew Energy.

Spartan Delta is a relatively new energy company created by the previous management team of Spartan Energy. The company has grown substantially in the last 2 years through multiple acquisitions. The team is focused on acquiring a diversified portfolio of quality assets which can be restructured, optimized, and rebranded to fully realize their potential. They look for assets with superior investment and cash-flow profiles that provide material upside and sustainable free cashflow under normalized commodity prices. These assets include high quality, multi-zone oil and gas operated production alongside a large land base and strategic infrastructure footprint. We have invested with this management team in previous entities and respect their business acumen. The stock is cheap on all metrics relative to their peers and the fund continues to hold the position in Spartan Delta.

The three names detracting the most from the funds quarterly performance were OpSens, Neo Performance Materials and NanoXplore. Collectively these three names cost the portfolio -1.5% for the quarter.

OpSens is a pioneer of innovative fiber optic sensing technology being applied to multiple sectors. The company has received FDA approval for its Fractional Flow Reserve (FFR) guidewire, resulting in a tool that is accurate, reliable and improves the clinical outcome of patients with coronary artery procedures. The company is currently awaiting FDA approval on their second guidewire tool for transcatheter aortic valve replacement (TAVR) surgery. This second approval will substantially increase the revenue potential for the company by increasing its addressable market and will give the salesforce a second product to sell into cardiologists. On the approval of the first product, the portfolio trimmed the position but continues to hold the remainder as the company seeks approval for the TAVR product, by which time their revenues should start to ramp up. COVID has had a negative effect on the take-up of their products as surgeries have been delayed.

Neo Performance Materials manufactures advanced industrial materials such as magnetic powders, specialty chemicals, rare metals and alloys which are critical in the performance of many everyday products as well as emerging technologies. Some of these advanced materials are used in hybrid and electric vehicles, pollution control systems, and water purification technologies. Last year the company had particularly strong growth in revenue with very high-volume growth and price appreciation. The company is currently looking to expand its Silmet Plant (a rare earth processing facility) in Estonia which they have funded with a recent equity issue. The fund reduced the position recently as the current Ukraine/Russian conflict seems to be weighing on the stock. While we like the company’s management and long-term prospects, we believe the stock needs to digest the large equity capital raises completed over the past two years.

NanoXplore is a manufacturer and supplier of high-volume graphene for use in industrial markets. The company’s Carbon Technology Group specializes in the sale of their signature graphene powder GrapheneBlack. As patented-proprietary clean technology provides customers with a range of graphene-based solutions. It is especially useful for improving the properties of plastics and polymers. In 2020, NanaXplore announced the creation of its own graphene battery initiative by adding GrapheneBlack to current Li-ion anodes to improve energy capacity and charging speeds. Using their low-cost graphene production technology, the company hopes to replace spherical graphite in this battery application. Given its leading-edge product portfolio in a hyper growth area, the stock price tends to be volatile. The fund has held a position in this company for many years. In the fourth quarter of 2021, the fund took some profits in this stock but continues to hold a position given the large opportunity ahead for this company.

OUTLOOK

From the beginning of the year, global equities experienced one of their worst starts in a decade. Worries of central banks raising interest rates to curb inflation put significant pressure on stocks. Adding insult to injury, when Russia invaded Ukraine, NATO countries were put into a conflict with a superpower for the first time since the Second World War. Another factor worrying investors is the resurgence of COVID in China and the governments zero tolerance approach which is slowing down the Chinese economy. Despite these negative developments, commodities rallied on low global inventories and concern that Russian sanctions would lead to further supply issues. As mentioned through much of last year, our forecast is that the resource sectors are setting up for a protracted period of outperformance for other reasons than the above-mentioned short-term issues.

On the energy front, we continue to believe the world is not ready to abandon hydrocarbons. There are not enough cost-effective alternatives in sufficient quantities to replace oil and gas. Although countries are trying to curb demand, the world continues to hit record demand levels for oil and gas. Investors in the sector have also insisted that energy companies run their businesses with more fiscal responsibility than in the past. This in turn is limiting the growth in domestic production despite the healthy price of oil and gas. We are maintaining the portfolio’s overweight position in the energy sector as we do not see the fundamental demand and supply picture changing in the foreseeable future.

On the base metal and associated industrial metal front, we continue to see a significant supply issue. After more than a decade of chronic underinvestment in the sector it should be no surprise that there is a dearth of large scalable projects to meet the increasing demand. Projects that are in the pipeline are in areas of higher geopolitical risk and projects are taking longer to get through the rigorous permitting process. As we move into an EV world, the pressure to find and develop more basic material assets only increases. We like the outlook for this sector and are well positioned to take advantage of the inevitable commodity price increases.

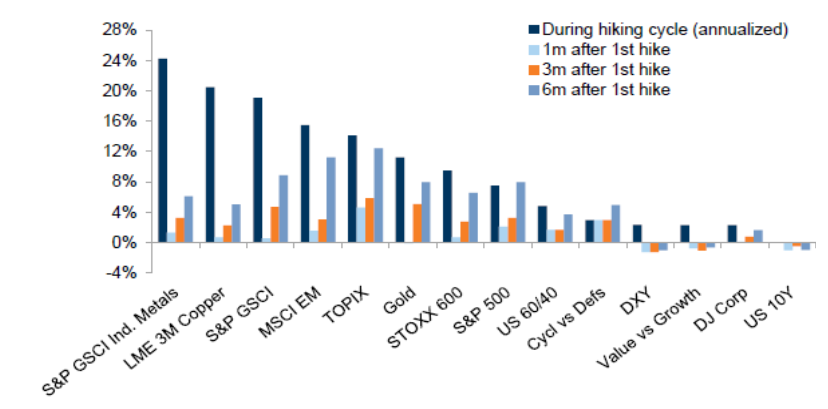

As the global central banks begin raising rates, we anticipate volatility will continue for the remainder of the year. Below is a chart showing the best performing sectors during Fed rate hiking cycles. In past cycles, industrial metals, copper, commodities (S&P GSCI), emerging markets (MSCI EM), and gold stocks typically are the best performers. The one area of concern we are monitoring is the possibility that overly aggressive rate hikes could push global economies into a recession. While we do not currently expect a recession in this year, we will be carefully watching for any signs of weakening.

Another area of current concern is how inflation pressures will impact corporate costs. Companies with large capital projects are especially vulnerable to these pressures. There have been many recent examples of cost pressures on mining projects as seen in their recent feasibility studies. We continue to look through our names for this risk.

In the past number of months, growth stocks have sold off sharply (particularly in the technology sector). We anticipate this trend to continue but will look to purchase some of these growth names at lower valuations.

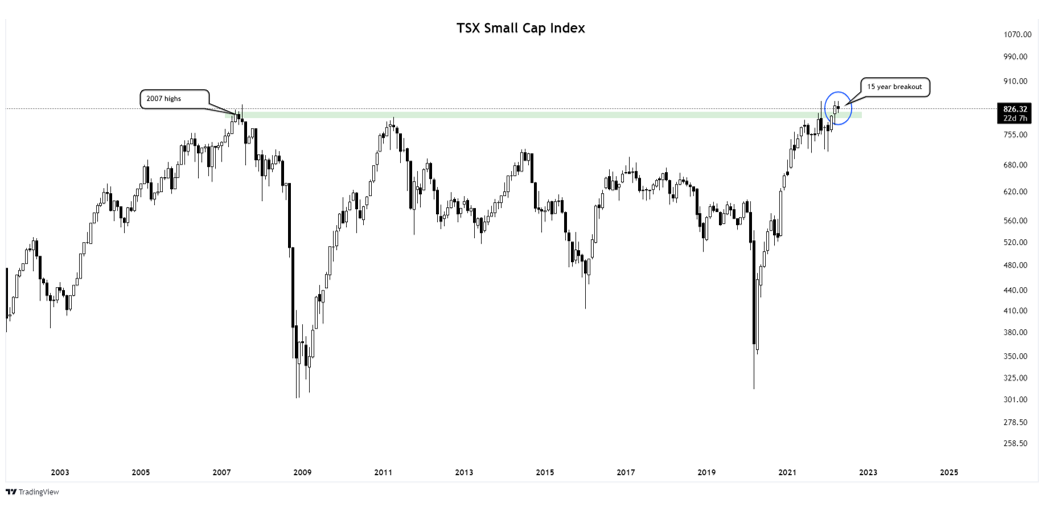

In closing, we have included a long-term chart of the S&P/TSX Small Cap Index. This is a monthly chart that shows the 15-year breakout of the index from the old 2007 highs. From a technical perspective, holding above these highs confirms that Canadian small caps are finally breaking out and are in a primary bull market (with some analysts forecasting an additional +60% to +70% of gains).

Despite this year’s volatility, the fund’s performance has been strong and makes for a compelling argument for investing in Canadian small cap stocks.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.