Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jacqueline Ricci

April 28, 2024

Was that the turning point?

The first quarter of 2024 started slowly but ended well. The market had many ups and downs centered around interest rate expectations. At the start of the year the dot plot was signalling five rate reductions in 2024. An aggressive number given that Fed Chairman Powell still did not see enough signs that inflation was abating, and the targeted 2% inflation rate was not in sight. The market absorbed a few dot plot changes with the current expectation for three rate reductions by year end.

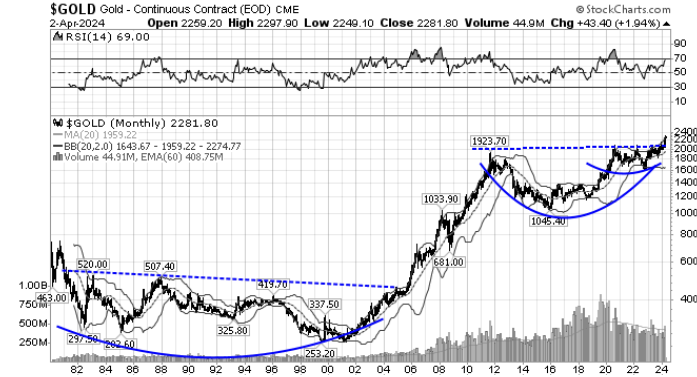

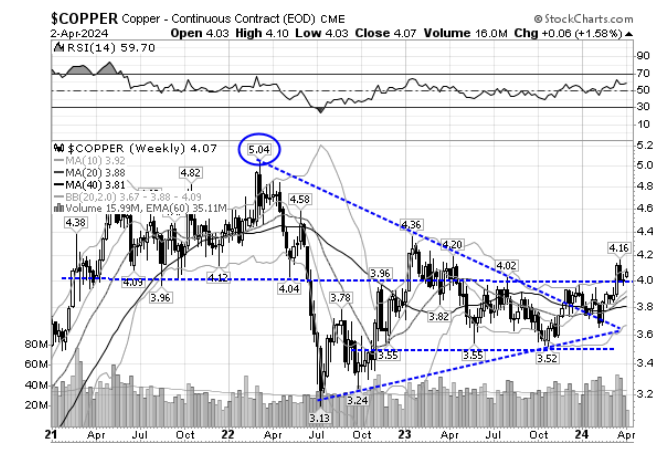

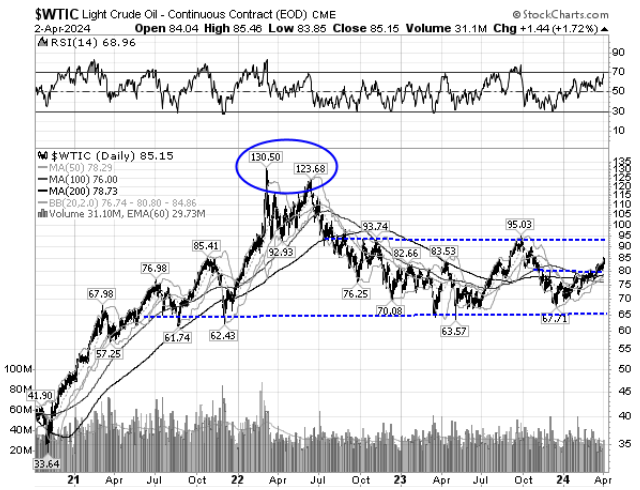

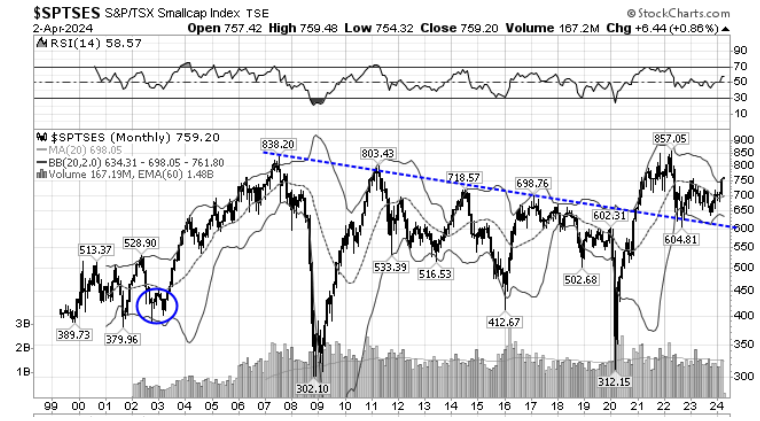

Global equity markets were very strong in the first quarter. At the beginning of the year, leadership was still squarely in the technology space but as the quarter progressed and economic data remained resilient, the rally broadened out into the small cap indices. The strength included the commodity sectors with the CRB Commodity Index rising +11.5% in the first quarter driven by record highs for gold (+8%) as well as strength in oil (+15%). Not to be left out, copper also rallied in March (+3%). The commodity gains came despite continued strength in the U.S. dollar.

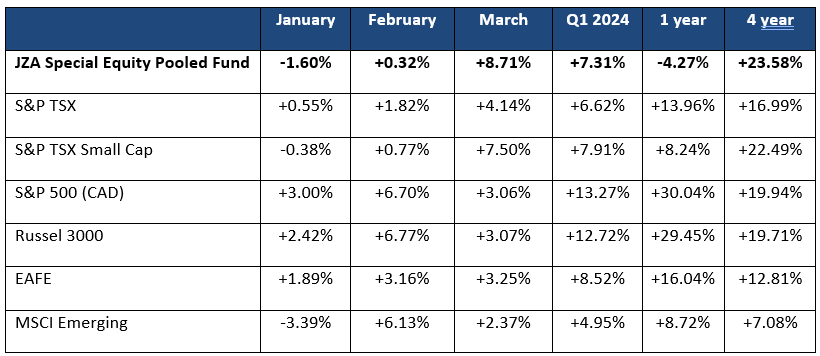

Below is a table showing global index returns including the TSX Small Cap index as well as the returns for the portfolio. The table shows the break down month to month, showing the slow start to the quarter but also the strong finish. The portfolio slightly underperformed the index for the first quarter with a +7.3% return versus +7.9% return for the index.

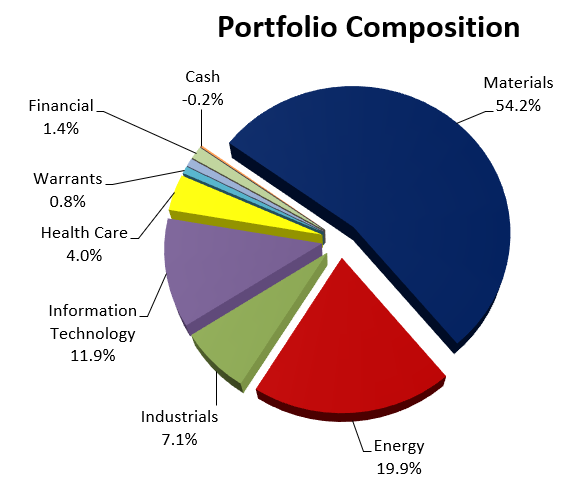

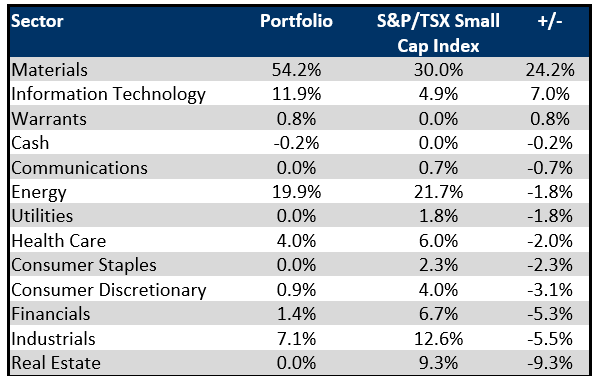

The following table shows the composition of the portfolio with some industry attribution metrics. Attribution of the material sector still showed us lagging as the larger cap names rallied first with catch up to follow from the smaller names as the rally in materials continued into the second quarter. Strong attribution came from Energy, Information Technology, and Industrials.

The three names which were the largest underperformers included Enablence Technologies, Lithium Ionic and Li-ft Power Limited. Collectively these names cost the portfolio -1.4% in performance.

Enablence is a Canadian technology company operating in the integrated optical products business. The company designs, manufactures and sells optical components, primarily in the form of planar lightwave circuits on silicon-based chips. It works with customers that have emerging market uses for its technology, including medical devices, automotive light detection and ranging (LiDAR) and virtual and augmented reality headsets. The company is currently funded and breaking new barriers in the leading-edge field of LiDAR. The portfolio continues to hold the position.

The other two names are both in the Lithium space. Lithium Ionic is a Canadian mining company exploring and developing its lithium properties in Brazil. Both assets are in the northeastern part of Minas Gerais state, a mining friendly jurisdiction that is quickly emerging as a world-class hard-rock lithium producing district. In April the company announced their maiden mineral resource estimate and the initiation of a PEA. Although we like management and the deposit, the significant decrease in lithium carbonate prices make the industry challenging. Electric Vehicle adoption appears to be slower than expected and there are other technologies being developed (DLE- Direct Lithium Extraction) that may bring on more supply at lower costs. The portfolio sold the position in Lithium Ionic to redeploy capital in other areas (specifically gold and copper companies).

Li-FT is a Canadian mineral exploration company engaged in exploration and development of lithium pegmatite projects with its flagship project, Yellowknife Lithium project located in the Northwest Territories. Although management is excellent and the opportunity is significant, the dramatic decline in the lithium price led us to reduce the position for other opportunities.

The three names that provided the portfolio with the best returns for the quarter included, Atex Resources, Source Energy Services and Celestica Inc. These three names contributed +3.0% to the portfolio in the first quarter of 2024.

Atex Resources is a mining company exploring its flagship property, Valeriano copper gold project within the Link Belt in north central Chile. The company is focused on delineating and growing the copper-gold porphyry resource underlying a surface oxide gold deposit. Drill results to date confirm the presence of a major system that is open in all directions. The company is well sponsored and funded and we are excited at the opportunity this investment presents. We continue to hold the position as we continue to be bullish on the outlook of copper and gold and see a scarcity of good development projects.

Source Energy Services is the largest supplier of quality proppant in the Western Canadian Sedimentary Basin. The company produces and distributes northern white and domestic frac-sand from their Wisconsin and Alberta facilities. The company has multiple catalysts in 2024, including refinancing the high yield debt to conventional debt, strong LNG tailwinds and an upcoming partnership announcement to drive further growth. We continue to hold our position of Source in the portfolio.

Celestica is a contract manufacturer that designs and manufactures electronic components for OEM’s. The company has strategically repositioned itself to focus on higher value and higher growth markets with longer lifecycles and better margins. The company is emerging as a core hardware provider to artificial intelligence (AI) infrastructure buildouts. The stock has been a tremendous performer; up over 56% last quarter and 249% over the last year. We have trimmed the position as the weight had increased but expect the company’s strong demand backdrop and favorable competitive positioning to drive peer leading revenue growth and improving margins. We continue to hold a position.

Looking Forward…

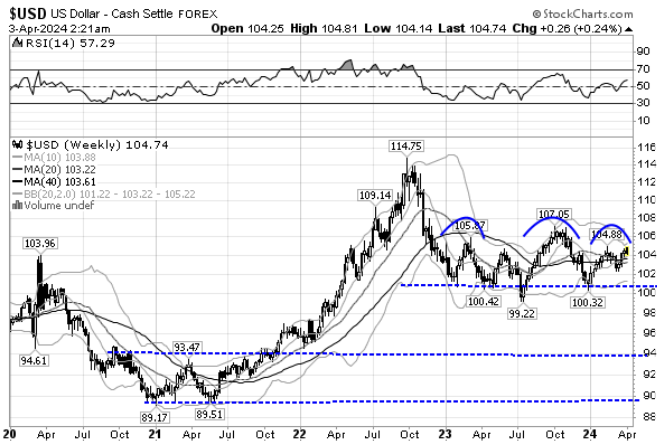

In the latter half of 2023, we expected the Fed would pivot and that would drive commodity markets on the back of a declining US dollar, decrease in real rates and higher future economic growth. While US rate cuts are being pushed out, the market is seeing some signs that we are closer to this happening and the mantra has changed from “rates need to be higher for longer” to “rate cuts are coming”.

Although the US dollar remains elevated it clearly is beginning to make lower highs and shows signs of exhaustion which would continue to favor our positioning in the commodity square.

With this expectation of a shift in macro policy, we have started to see the CRB Index begin to move providing a good underpinning for the gold, base metal and energy sectors with the underlying commodities breaking out.

We have held firm over the last number of months that this broadening of the market would take place and we are finally seeing the TSX Small Cap Index begin to break out of a consolidation.

On a fundamental basis our thesis for base metal and gold prices still holds. The underinvestment over the last 15 years will create very tight supply situations earlier in the economic cycle; in fact, we are already seeing the tightness of supply and we are only at the end of the tightening cycle. Copper specifically, despite the electric vehicle adoption taking longer to materialize, is benefitting from the artificial intelligence connectivity roll out and the tightness will only be exacerbated when demand from China and rest of world begins to increase. Our names in the copper space include a good mix of producers and developers; Capstone, Hudbay, Taseko, Atex, Filo, NGex and Arizona Sonora.

Although it appears that the uranium price is pausing, we still are bullish for the outlook of the sector. Markets remain very tight and contract prices continue to work their way higher to meet spot prices. We continue to hold NexGen, Dennison, Encore and F3.

Energy is a sector we are closer to market weight. We see great value in the space with companies operating well with very strong cash flows. The hesitancy is that, with higher WTI prices, companies can push drilling and increase supply to meet demand. The current price of WTI is ideal for the industry to continue to return capital to shareholders. The portfolio has a heavy oil bias as we see differentials coming in. Names exposed to the heavy of trade include IPCO and Athabasca.

As we move toward summer, we are looking for opportunities in the natural gas space. Currently natural gas storage is very bloated and summer gas pricing will be challenging. As companies work their way through these difficult prices, the back half of 2024 looks more promising as Canada’s first LNG facility turns on and will take 2 bcf (billion cubic feet) of gas out of North America. This coincides with a US facility turning back on and removing another 2 bcf of gas.

The technology sector has provided good returns over the last few quarters. Some of this is related to the strong growth in revenues but some of the significant returns are related to the decrease in rate expectations pushing multiples paid for these stocks up. We see further growth in our technology names but are cautious that stocks are no longer cheap. Our favorite names include Docebo, Celestica, Copperleaf and Tecsys.

Looking for Q2 to show more follow through of what began in earnest in March as we move closer to eventual interest rate reductions.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.