Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

January 24, 2023

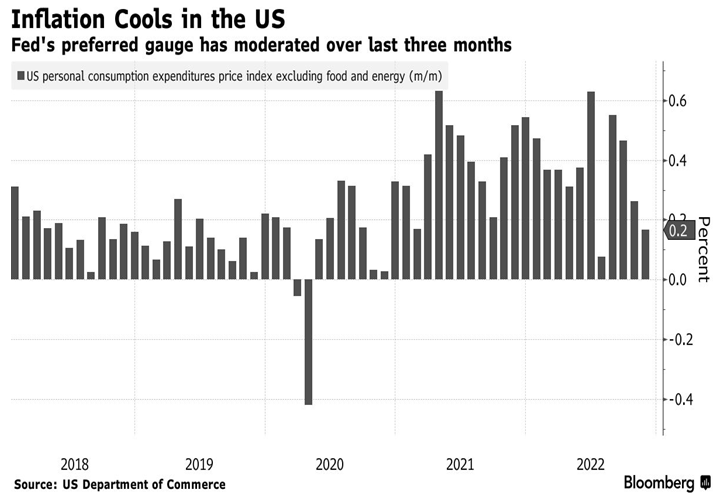

The U.S. Federal Reserve Board entered 2023 with plenty of resolve to make sure it wins the war on inflation, which in 2022 rose to the highest levels in four decades and then started to decline in the final months of the year. The central bank began raising its benchmark interest rate from almost zero in March, which most outsiders criticized as too late a start to the tightening cycle. Sensing that they might have been a bit ‘behind the curve’ in this regard, they then picked up the pace with super-sized rate hikes for much of the rest of the year, bringing the federal funds rate to the 4.25-4.50% range, the highest since 2007. This aggressive policy is starting to yield results as we see inflation rates begin to recede (below) in both the U.S. and Canada. The year-over-year numbers are still up in the 6% range, but the ‘annualized 3-month’ inflation numbers are closer to zero, with almost all categories receding. That has given investors more confidence to believe that central banks will start to retract some of their more ‘hawkish’ commentary and has most likely been responsible for most of the rally in stocks we have seen in January. While investors look ahead to a potential ‘pivot’ in Fed policy back to an ‘easing mode’ later this year, the Fed continues to re-iterate its hawkish policies and commitment to keep interest rates ‘higher for longer.’

The contrary messages from the bond vs the stock market. Based on Fed funds futures, financial markets are now pricing in nearly 200 basis points in rate cuts between June 2023 and December 2025. Historically, cuts of this magnitude have almost always been associated with a recession. During the “soft landings” that is anticipated by bullish stock investors, the easing from the Fed is closer to 50 to 75 basis points, meaning the bond market is clearly predicting an economic downturn. In contrast, consensus S&P500 earnings are expected to grow by +9% in 2023, which implies a recession will be avoided (profits typically decline by about 20% during “hard landings”). Both the bond market and stock market can’t be right. We think the bond outlook has it right, which means the stock market is likely to see further selling pressure as its current optimistic assessment is revised downward.

So how do we factor also these differing outlooks into a cohesive, low-risk strategy for investing in 2023? Our simplest call is to increase exposure in bonds to at least a market weight (i.e. 40% for most balanced portfolios). The nominal return on bonds has risen (even though real returns are still negative based on current inflation) but we see no way we can avoid slower economic growth for the balance of 2023, a condition which would provide a continued tailwind for bond prices. We also expect inflation rates to continue to recede throughout the year, thereby improving the real return on bonds. Cash returns have also risen and we prefer holding cash over preferred shares at this time since we still see some credit risk from the preferred share sector as economic growth slows.

In terms of stocks, it is more of a conundrum. Markets rarely suffer two negative years in succession, so last year’s poor returns may already incorporate much of the bad economic news we see ahead. Stock market multiples have checked back to long-term averages and investor sentiment has plunged to bear market levels. Those facts alone seem to mitigate some of the downside risk to stocks. But valuations generally tend to ‘overshoot in both directions’ so there is no guarantee we won’t decrease to even lower levels. Tech stocks have already done that with many of the major players seeing stocks drop over 40% without any consequent decline in earnings estimates. After January’s rally we have moved back to an underweight position in stocks (around 45% in balanced funds, nearer to the low end of our traditional 40-60% range). We reduced technology stock exposure as we want to see how the economic slowdown will impact some of their key growth areas of the past few years, particularly cloud services, phone sales and mobile advertising. We have maintained a strong weight in semi-conductors, though, as they have already adjusted to lower estimates and still need to rebuild productive capacity given the ongoing chip shortage in key sectors.

We also reduced energy exposure but are still overweight oil stocks, as we see ongoing supply constraints and exceptionally low historical valuations. We reduced exposure to economically sensitive sectors such as consumers (autos, retails and housing), industrial production (steel, base metals and rails) and remain underweight financials. Gold stocks continue to look like a good contrarian play this year as we expect more U.S. dollar weakness, decades-low valuations and a reversal of the tight interest rate environment later this year. For income-oriented accounts, we continue to like the pipeline and telecom companies for their high dividend yields, stable earnings and moderate valuations. Top names in those sectors remain Rogers, BCE, Telus, AT&T, Enbridge, TC Energy and Pembina Pipeline. We don’t see 2023 as a year in which a ‘risk on’ strategy throughout the year will work since markets will continue to be volatile, but we also see limited downside risk in many sectors and don’t want to be significantly underweight stocks. This is particularly key after such dismal overall stock market returns in 2022 and the extremely negative sentiment that is typically more indicative a something closer to a market bottom than a top!

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.