Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

January 24, 2023

After, arguably, the most difficult year for financial markets since the Crisis in 2008, stocks and bonds seemed ready for at least a slight rebound on hopes that things would be better in 2023. Markets did not disappoint as stocks came out of the gate strongly, lead by many of the biggest losers from last year, with the Nasdaq and Russell 2000 indices leading U.S. stocks, with each up 6% month-to-date at this time versus a 3.5% gain for the S&P500 and only minimal gains in the Dow Industrials). In Canada, technology (+10%) and ‘gold-laden’ Basic Materials (up 12%) sectors were leading the 5.5% TSX gain. Bonds also rallied on the view that economic growth is slowing and inflationary pressures are receding. Stocks gave back some of those gains as fourth quarter earnings reports started to flow in later in the month, heightening fears that corporate profits would be coming in lower than expected this year. Companies were less able to pass along prices increases as demand slowed but their costs, particularly materials, labour and interest costs, continued to rise. This put the squeeze on profit margins. Many tech companies, realized that their costs were out of line with their reduced revenue outlooks and decided they needed to cut back employee counts. The bottom line is that we continue to believe that earnings remain the biggest risk for stocks in 2023, much as rising interest rates were the biggest risk last year. The economic data had thus far remained relatively robust, but aggressive rate hikes had yet to show up in the economic numbers, primarily because the economy had a lot of momentum going into the rate hiking period. Business inventories were low and consumers were still relatively flush with cash from all the stimulus offered during the heights of the pandemic. More importantly, though, travel and other services were surging once again as the global economy had finally re-opened fully and there was ‘pent up demand’ for those services. That economic reprieve looks to be ending.

Debt levels had also been built up over the past decade, facilitated by the ‘near zero’ interest rate environment that prevailed. With those policies reversing so unexpectedly and quickly in 2022, there has to be an impact on economic growth at some point. Economics may not be an exact science in terms of forecasting when the impact of higher rates ultimately is felt, but it is not irrational to the degree that these increases would have no impact! Federal Reserve policy famously “acts with long and variable lags”, to paraphrase the ‘father of monetarism’ Milton Friedman. We’re less than 12 months into this hiking cycle. Higher interest rates are taking their toll on housing, auto sales and other interest sensitive sectors. This is spreading to other sectors of the economy as consumers and businesses roll over existing debts at much higher rates. Aside from housing, higher rates are only now hitting the broader economy, with both the Institute for Supply Management (ISM) services and manufacturing indices falling into contraction territory in December. It is not a matter of ‘if the slowdown will occur,’ it’s only a matter of ‘when.’

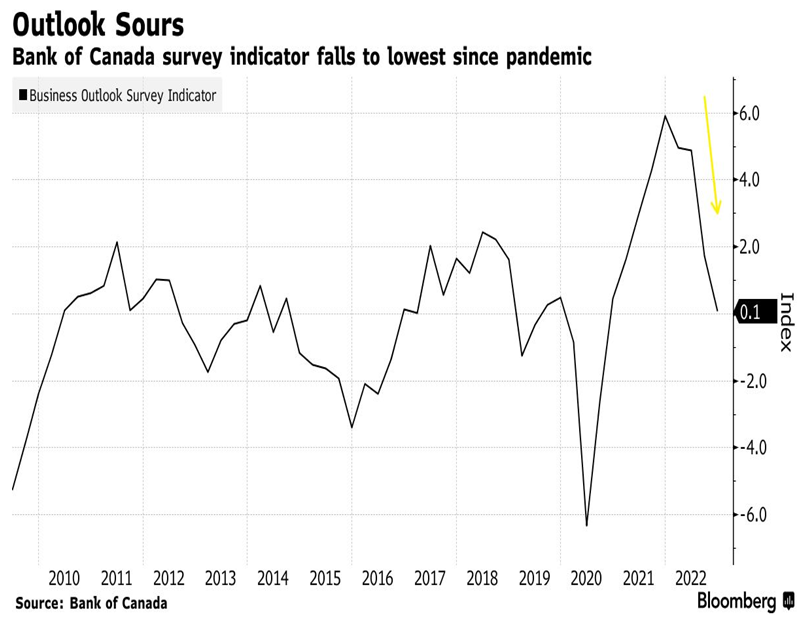

Sentiment among Canadian firms is at its lowest since the Covid-19 pandemic and inflation expectations remain elevated, Bank of Canada surveys show. The central bank’s business outlook indicator fell in the fourth quarter as about 70% of businesses see the economy heading into a recession, and more firms than usual expect their sales to decline. Higher interest rates and inflation have also limited the ability of consumers to spend, the Bank said in a separate survey. The data suggest the Bank of Canada won’t need to increase interest rates much further in order to bring demand and supply back into balance, and that last year’s aggressive hikes are already working to slow growth. That view has helped the stock market get off to a better start in 2023, as we find ourselves in that old conundrum where “bad (economic) news is good (stock) news!” The chart below shows how sharply the BOC Business Outlook Survey has rolled over since the rate hikes started in early 2022.

Sentiment is just as poor among individuals as it is with business. Canadians are increasingly worried about their levels of debt amid rising interest rates and high inflation. The MNP Consumer Debt Index, a quarterly snapshot of consumer sentiment in Canada, fell to a new low for the index that speaks to Canadians’ mounting concerns about their personal finances. MNP also said that fewer people were confident in their ability to pay for living expenses this year without going further into debt and said they were already feeling the effects of interest rate hikes after last year’s tightening cycle from the Bank of Canada.

Just as investors are celebrating the prospect of peak inflation and potential for a soft landing, this earnings season is likely to show there’s still plenty that should keep them up at night. With costs still on the rise, interest rates starting to bite and consumer spending declining, results are expected to reveal the start of a U.S. earnings recession, which will last until the second half of 2023, according to Bloomberg Intelligence strategists. While analysts have been busy slashing their forecasts over the past few weeks, the consensus for corporate profits in 2023 remains too high with or without an economic recession. Slowing demand will be in focus this reporting season as a harbinger of recession. US economic data showed consumers lost momentum in November amid higher interest rates and elevated inflation. Americans are tapping into savings and leaning more on credit cards, raising the question of whether they’ll be able to continue driving economic growth through 2023.

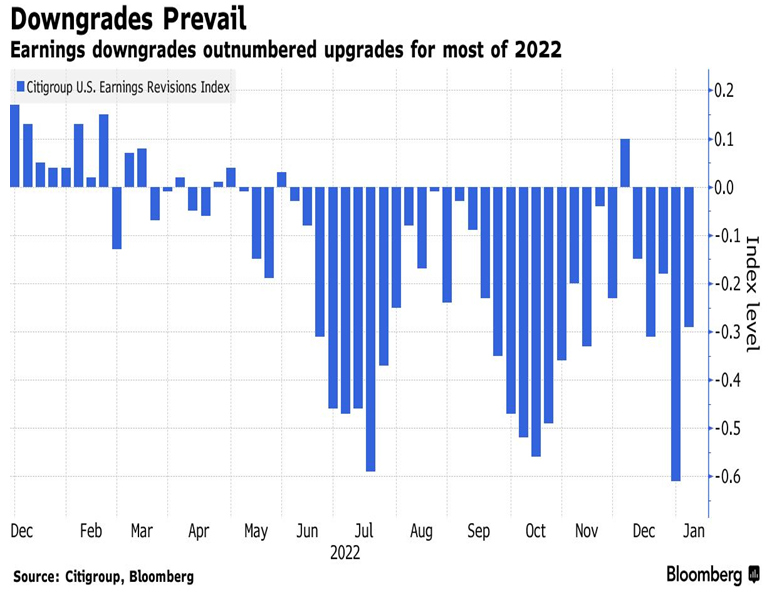

Earnings confession periods in March, June, September, and December 2022 led to an average 5% decline in S&P500 monthly performances. However, after analysts lowered the earnings bar, relief rallies ensued through the reporting season with earnings coming in better than feared. The sharp rebound in stock prices in January is consistent with this playbook. We do not believe this is the beginning of a new bull market since a recession has not even begun yet, but this rally could have more legs in the short-term as negative speculative positions are unwound. From a technical standpoint, the S&P500 is back above its 200-day moving average while price momentum indicators and other overbought conditions are slowly building, with a high level of stocks trading above their 50-day moving averages. Against this backdrop, we maintain our ‘sell-on strength’ strategy and reduced stock weights very recently. More importantly, as shown below, earnings estimates continue to be downgraded, as they have for most of the past six months, suggesting that analyst expectations are still too high and investors need to adjust to those new, lower levels.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.