Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

September 24, 2022

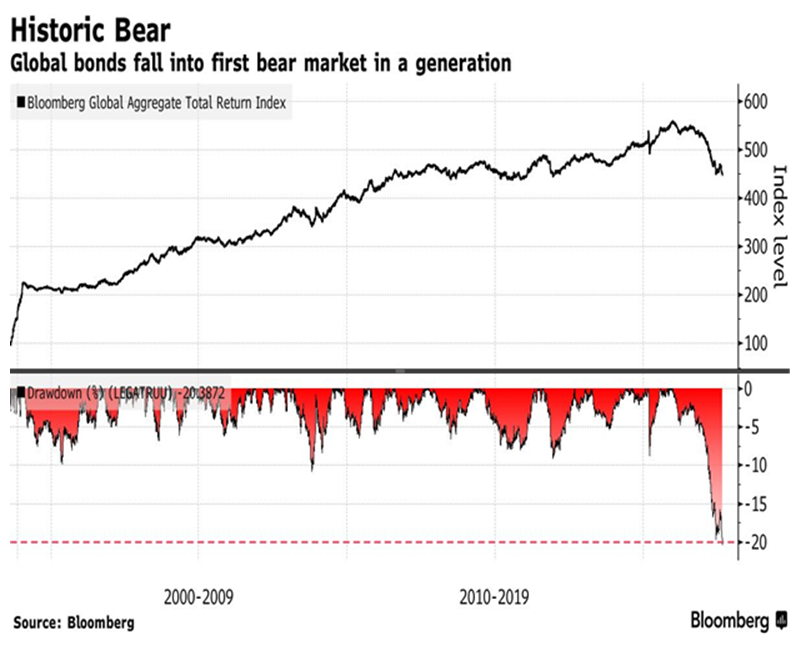

Under pressure from central bankers determined to quash inflation even at the cost of a recession, global bonds slumped into their first bear market in a generation. The Bloomberg Global Aggregate Total Return Index of government and investment-grade corporate bonds has fallen more than 20% from its 2021 peak on an unhedged basis, the biggest drawdown since its inception in 1990. Officials from the U.S. to Europe have hammered home the importance of tighter monetary policy. With inflation most likely having seen its peak for the cycle and economic growth in the process of slowing, bonds are suddenly looking like a good alternative to stocks, for the first time in over a decade! While we have suggested we might be getting closer to a low in the stock market, the more attractive, lower risk investment is in bonds right now. We have shifted most of our excess cash reserves in client portfolios into bonds recently, while maintaining a slight underweight position in stocks.

Dusting off the old growth stock research reports. While almost all the current stock research is taking on a much more cautious approach and somewhat dour and bearish, we find it worthwhile to go back and look at the reports from those same analysts a year or two ago, when the stocks were anywhere 100-300% higher than they are today. Was the basis behind positive reports back then just wrong or was it simply that valuations got too extended? It’s easy now to say that Peleton was never worth over $150, Zoom over $500 or Shopify over $2000. We find it instructive to look at both the current dire research as well as the bull market stories to evaluate whether a stock was just over-valued or whether the story about their growth was actually wrong. In that vein we are finding buying opportunities in many growth stocks, but certainly not in all the names. While we haven’t bought Netflix due to its struggles with new subscribers and constant need for new content, we have added Disney recently as it should benefit more from the re-opening of the economy and its massive library of content that it is now putting onto its various streaming services. In the semi-conductors, we are still not buyers of Nvidia due to its high valuation and relative dependence on gaming and crypto, we have bought into Advanced Micro Devices, which continues to pick up desktop market share from Intel as well as growing its dominant position in data-centres. In cloud software we are still not looking at Shopify due to their high cost structure, slowing growth and continued excessive valuation, we have bought into Lightspeed Commerce, whose valuation has dropped to about four times revenue, is nearing cash flow breakeven and still has strong organic growth. In all of those cases, the common elements are the same. The stocks are down hugely from their highs but their growth stories are still intact and valuations are more reasonable.

Growing profits in a no-growth business. While investors are always looking for ‘growth’ in earnings of the companies they buy stocks in, there have been lots of success stories from companies that were in ‘no growth’ businesses. In all those cases, they had excess free cash flows and were able to re-invest those cash flows in accretive acquisitions which allowed the company to continue to expand their earnings despite no growth in their core businesses. Philip Morris did that in the tobacco industry in the 1980s. In Canada, Alimentation Couche Tard has done that in convenience stores while, in technology, Open Text and CGI have run similar acquisition models. The most successful has been Constellation Software, which has continued adding multiple acquisitions annually using their massive free cash flows, which has resulted in investors giving the company a premium valuation of over 20 times operating cash flow. Accidents can come with these strategies though, as demonstrated by Valeant Pharmaceuticals, with their huge buying spree that took the company to the highest weight on the TSX in 2015. However, those purchases were all done with debt as opposed to free cash flows, and those debt loads are what crushed the company when the acquisitions could not meet the markets appetite for further growth. Fast forward to today and we look at how BioNtech and Moderna failed to use all the excess cash flows from their covid vaccine windfalls to make acquisitions to supplant this growth once the inevitable slowdown in vaccine sales finally came. Pfizer, on the other hand, has used all the excess cash from their mRNA vaccine windfall to make substantial accretive buys, which have helped the stock do substantially better than Moderna or BioNTech.

Using these same analogies of growth, we are looking at the energy sector and wonder whether they should learn from those histories and use the excess cash flows from the current windfall of record energy prices to invest in ‘non-renewable’ energy, which will sustain their growth after fossil fuels start to deteriorate, as they inevitably will. Shareholders have rightly been asking for more pay-outs in terms of buybacks/dividends after years of suffering poor returns and we understand this. However, they should look out further and start to move some funds into more sustainable areas of growth. If Elon Musk is right about the growth and penetration for electric vehicles, the demand for gasoline is going to be substantially lower a decade from now. In that scenario, we see very little chance that oil with still be trading up in the current US$80 per barrel range and those energy companies that acted will be glad they diversified into some renewable energy projects.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.