Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

March 27, 2023

After keeping interest rates at record low levels for over a decade, global central banks did a complete 180 degree turn in the past year with the most aggressive period of rate increases in over 40 years. Given the sharp and unexpected reversals in policy and the addiction to low interest rates in the markets and the economy, we expected a sharp pullback in growth. Yet we watched in amazement as this ‘highly levered’ global economy continued to surge ahead, ignoring all of the well-established rules of monetary policy and pushing out the ‘long and variable lags’ that accompany the implementation of these policies. That apparent ‘economic immunity’ to these rate increases seemed to come to an abrupt end in the past month as something finally ‘broke’. But it wasn’t the economic data, it was the banking system!

Not unlike the Global Financial Crisis in 2008, which saw its birth in the collapse of a few loosely followed mortgage funds, this banking implosion was also quietly conceived in the bowels of California tech community. The collapse of Silicon Valley Bank (SVB) was a direct result of the easy money policies of the past decade, which were magnified exponentially in the early days of the Covid pandemic. With interest rates effectively at zero, many regional banks which did not have well-sourced deposit bases were able to access cheap wholesale funding from many of the upstart technology companies that were their clients as well. What wasn’t loaned out was put into U.S. Treasury securities, which still earned those banks a positive spread on their money and gave them capital to extend loans to non-profitable upstart companies whose stocks were being elevated by the speculative bubble growing in that high growth tech space. But once the Federal Reserve and all other central banks started raising rates so aggressively, these banks lost their cheap sources of funding while also watching the value of their holdings of Treasury securities plummet in value. When SVB decided they needed to raise some additional capital to maintain their balance sheets, investors fled from the bank, doing massive withdrawals of their funds, almost all of which were substantial amounts well in excess of the $250,000 limit for insuring those deposits. That fear spread to other regional banks, with Signature and First Republic Banks also seeing their stocks plummet over 60% in a matter of days. The contagion also went beyond the U.S. borders as the venerable Credit Suisse, with almost 200 years of history as a major Swiss bank, saw its shares plummet in value and Swiss regulators stepped in to broker a takeover by its larger rival UBS as confidence deteriorated.

Canadian banks also got caught up in the selling, with Bank of Montreal and TD taking the biggest relative hits due to their recent major acquisitions of U.S. regional bank (BMO bought California’s Bank of the West earlier this year while TD’s purchase of Tennessee-based First Horizon is still pending). Canada’s Big Six banks have nearly $30-billion in what are called “unrealized” losses in their securities portfolios. But the key for Canadian banks’ health is that the losses are offset elsewhere on their balance sheets by financial hedging instruments that have produced profits, even as their bond portfolios have declined. That overall picture of Canadian banks’ balance sheets reveals once again how the country’s distinct banking culture has largely insulated its big financial institutions from the problems facing the United States.

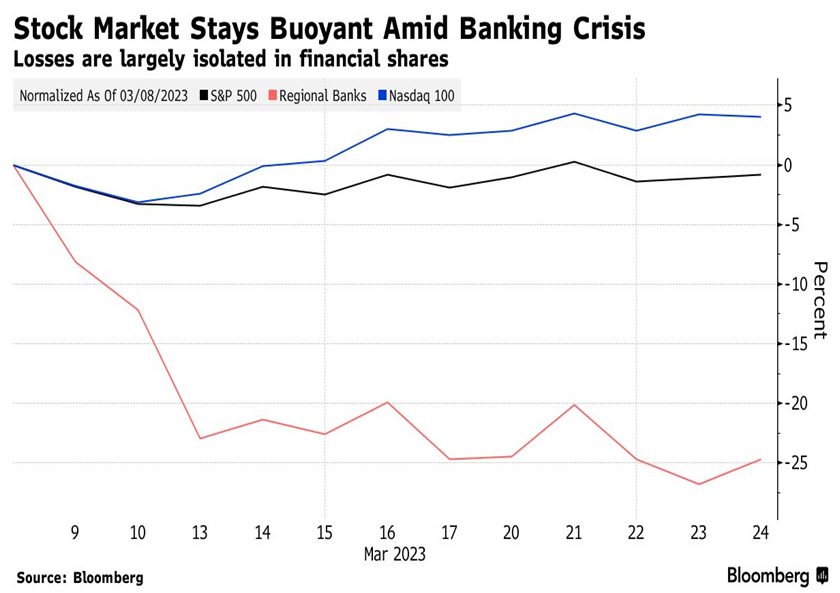

Even the biggest U.S. money center banks got caught up in the initial round of selling, despite the fact that they were beneficiaries of the carnage to some degree as they saw massive inflows of deposits from clients of regional banks, that helped to solidify further their diversified deposit bases. Bank of America claimed an initials uptake of over $15 billion in new deposits, but still saw its stock plummet over 20% in the week following the SVB collapse. The problem now, however, isn’t the possibility of more bank failures. It’s that banks are likely to curtail lending and thereby tighten credit conditions and accelerate the path to an economic downturn. Even before the failure of SVB, the percentage of banks tightening lending standards had risen to 44.8%, the highest reading since July 2020, at the peak of the Covid lockdowns. Given the problems at regional banks, that percentage is likely to go even higher and accelerate the growth slowdown. The result is that banks and energy stocks have been the downside leaders in the market over the past month, the latter due to heightened fears that we are closer to a recession that will reduce oil demand and the former due to the perceived higher risks to the banking sector. However, despite all of this carnage in the banking sector, the increased economic risks and the continued ‘hawkish’ views espoused by central bankers, the stock market has proven surprisingly resilient. As shown in the chart below, from the day of the SVB collapse, the S&P500 is basically unchanged as we write while the ‘technology heavy’ Nasdaq Index has been the leader, rising almost 5%. At the same time, the Regional Bank Index in the U.S. has lost over 25%.

Investors clearly have focused more on the idea that these banking problems could help to reverse the aggressive interest rate calls from central bankers. Forward interest rates curves are now forecasting 150 basis points of ‘easing’ in interest rates over the next 18 months, despite the ongoing rhetoric from Fed Chairman Jerome Powell and ECB Chair Christine Lagarde that interest rates are going to stay ‘higher for longer’ until the ‘back of inflation’ is clearly broken. Investors don’t seem to believe the Fed’s commitment to its inflation target goals and believe that they will have to act to provide ample liquidity to the banking sector to prevent a repeat of 2008. For now, stock market bulls are enjoying the equity resilience, emboldened by hopes that the Federal Reserve will soon pause its aggressive inflation-fighting campaign and regulators including Treasury Secretary Janet Yellen can contain any financial fallout. Bears are quick to note: the same thing happened in 2008, when the Lehman Brothers collapse incited extreme turbulence. At present, stocks remain closer to their lows than highs of last year and a lot of pain is already priced in.

We still come down somewhat in the middle of this argument. We believe that central banks will remain vigilant about inflation than consensus investor sentiment. Prior periods where they have reversed policy before inflation was totally tamed ended up seeing a very fast return of inflationary pressures and the need for even more aggressive rate hikes down the road. This is something the central banks want to avoid repeating. However, we don’t believe that inflationary expectations have been built into consumer behaviour, particularly wages, anywhere close to what they were in the 1970s. Moreover, the supply shortages are starting to ease and the ‘re-opening’ of the economy seems complete. That supports the argument that inflation will recede relatively quickly back down close enough to the 2% target range that central banks will be able to take their ‘collective feet off the brakes’ in terms of interest rates.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.